- Cigna tops estimates for third quarter and raises EPS guidance (marketwatch)

- Warren Buffett’s Wisdom Can Cut Through the Fog of Inflation (Barron’s)

- High Anxiety. The Energy Report 11/04/2021 (Phil Flynn)

- Wall Street’s smartest hedge funds are now getting smacked by inflation (New York Post)

- Small-Cap Stocks Are Making a Comeback (Barron’s)

- IBM Spinoff Kyndryl Starts Trading. Now It Needs to Figure Out How to Grow. (Barron’s)

- Booking’s Earnings Show Travel Is Back (Barron’s)

- Merck Covid Pill Gets First Authorization From the U.K. The Stock Is Rising. (Barron’s)

- Three generations haven’t traded through an inflationary cycle. Here are the stocks for it, one seasoned fund manager says. (marketwatch)

- S. jobless claims drop to pandemic low of 269,000 as firms avoid layoffs during labor shortage (marketwatch)

- Some puzzles left behind after Fed Chair Powell’s press conference (marketwatch)

- After Tame Taper, Powell Shifts Focus Back to Jobs Market (Barron’s)

- House Releases Draft of Social Spending Bill. Paid Leave and SALT Added Back In. (Barron’s)

- Activision has worst day in 13 years, technician says it could be a buy (CNBC)

- Inflation Debate Can Wait as Fed Tapers (Wall Street Journal)

- The longest-standing tech analyst on Wall Street shares the 4 criteria he uses to identify the biggest winners in the market, and 2 stocks he thinks could be among the next FAANGs (businessinsider)

- Aston Martin Nears Rollout of $3 Million Valkyrie Hypercar (Bloomberg)

- In a Deal Desert, Warren Buffett’s Berkshire Hathaway Keeps Buying Itself (Wall Street Journal)

- How to Block Your Phone from Interrupting You (New York Times)

Tag: StockMarket

“Shoot First, Ask Questions Later” Stock Market (and Sentiment Results)…

On September 22, Chairman Powell said that while we had met “substantial further progress” on one half of the dual mandate (inflation), we had not yet hit “substantial further progress” as it related to the second half of the mandate (full employment). He specifically said he would need to see a “decent” jobs report prior to moving ahead with taper. That may happen on Friday, but it had not happened at the time of his announcing taper (yesterday).

He bowed to the pressure and blinked before meeting his objective. Whether this will result in his deepest fear of long-term structural unemployment (as we saw in the 8 years following the Great Financial Crisis of 2008-2009) remains to be seen. In the mean time, several factors that led to the high inflation prints of late are rolling over into this new tightening of policy:

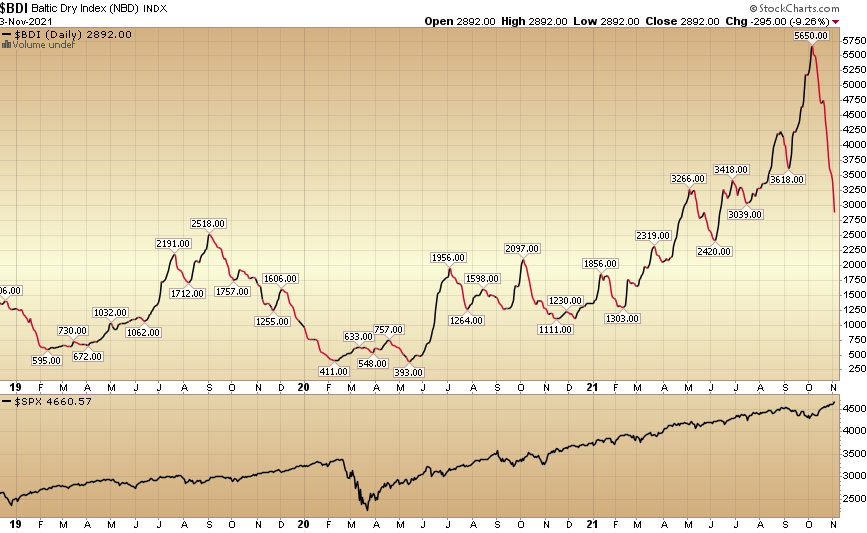

The Baltic Dry Index – which measures the average prices paid for the transport of dry bulk materials across more than 20 routes – has collapsed 48.81% since October 7.

The Baltic Dry Index – which measures the average prices paid for the transport of dry bulk materials across more than 20 routes – has collapsed 48.81% since October 7.

The average sale price of a 40-foot container in China plunged by 22.5% in the first two weeks of October alone.

Malcolm Wilson, CEO of GXO Logistics Inc. – the world’s largest pure-play contract logistics provider – said Tuesday that global supply chain bottlenecks should ease by the end of the second quarter of 2022, and that massive spikes in demand hitting GXO’s U.S. facilities are already starting to level off. He told analysts that the issues that we’re seeing right now he believes are very much temporary.

“We’re anticipating to continue to see them probably into Q1, maybe even into Q2, but definitely it’s a temporary issue, [and] it will abate.”

But Chair Powell couldn’t take the heat, so he got the hell out of the kitchen.

Wages (year on year percent increase below) – which are sticky and have moved up – should start to rise more modestly as more and more people re-enter the workforce due to extended unemployment benefits expiring in September, and vaccination rates (childcare/school resumption) improving:

The labor force participation rate recovery will dampen the wage increases over time (it is modestly trending up – with the exclusion of September – due to Delta):

Whether he went in November (bowing to external pressure), or January (as I had anticipated), does not make much of a difference – as it was well telegraphed to the market. At the end of the day, people don’t like paying $12 for a gallon of milk – whether it’s due to short term supply chain issues or not. Couple that with the Fed trading fiasco and they blinked a couple of months earlier than anticipated – but it was inevitable nonetheless.

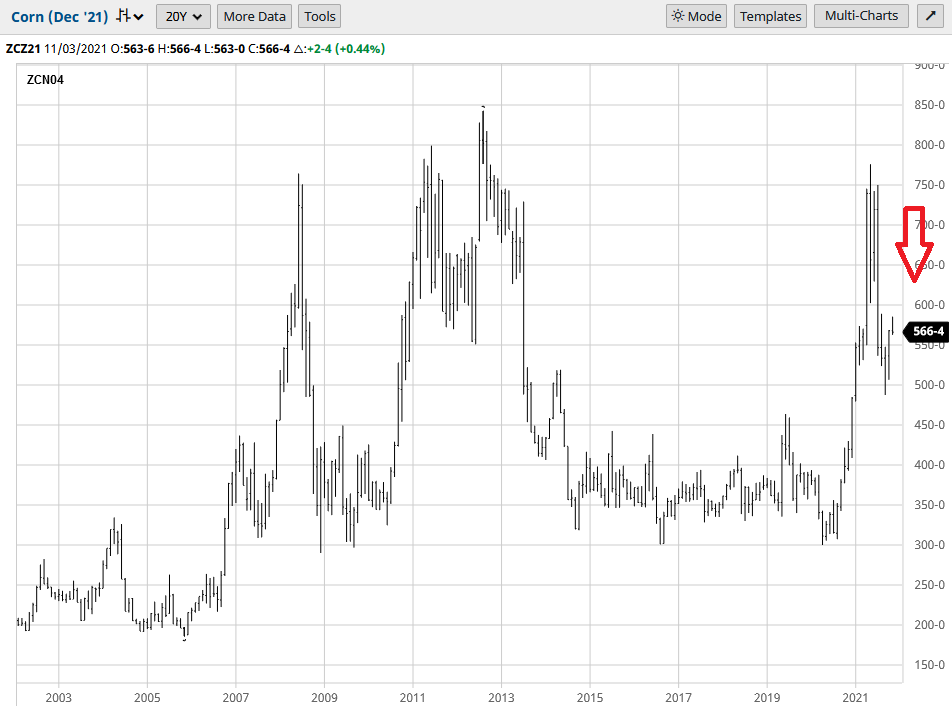

They had more runway than they thought to get the 2M extra unemployed folks back to work, but they are opting to put out a grease fire with water – despite the fact that the sand is just a little further away (and more effective). Here’s what I mean when I suggest that the rollover in some prices are already well underway and will show up on a lagged basis in coming months (irrespective of taper):

(Charts by BarChart, Annotation by Tom Hayes)

Everyone’s complaining about milk prices TODAY but the collapsing prices WILL SHOW UP IN THE SUPERMARKET ON A LAGGED BASIS:

Everyone’s complaining about milk prices TODAY but the collapsing prices WILL SHOW UP IN THE SUPERMARKET ON A LAGGED BASIS:

So could they have waited a few extra months to ensure those 2 million more people unemployed (than pre-pandemic) got back into the labor force? Yes.

Does it matter that they are tightening into falling prices (will show up on lagged basis) and slowing rates of growth?

Yes, but it’s tough to get re-appointed when milk is $12 a gallon and the general public is upset with public officials (legally) trading while in possession of non-public information.

So they bent – despite not having the confirmatory employment data in hand at time of announcement. The net effect is probably 500k unemployed people will be left out in the cold when all is said and done. Rather than having 5.7M unemployed as we did in Feb 2020, we’ll likely wind up with ~6.2M unemployed when we hit “full employment” this time. Enough time will pass that they will stop being counted because we took the foot off the gas a hair too early. Hard to see now, but it will become clear ~18 months from now.

Overbought?

Alan Shaw, the legendary former head of technical analysis at Smith Barney, once said, “The most bullish thing a market can do is get overbought and stay that way.”

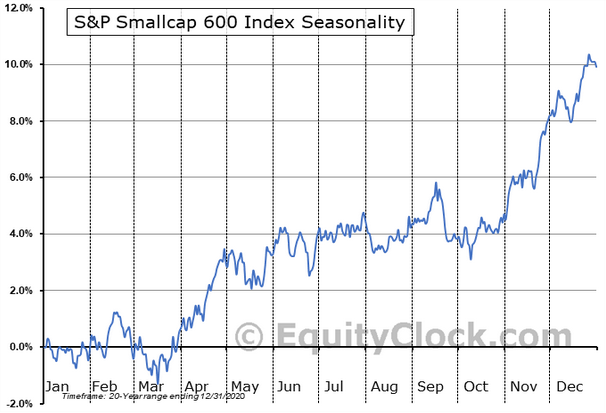

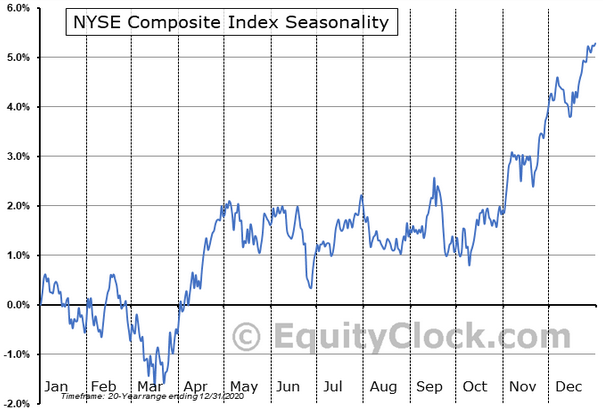

On the one hand, the S&P Small Cap index (similar to Russell 2000) finally broke out to new highs – after consolidating sideways for ~9 months. This is constructive (and consistent with a rising rate environment). We also saw regional banks up nicely after the Fed announcement. ‘Tis the season…

The ValueLine Geometric Index (the original “equal weight” index) also broke out to new highs on the Fed announcement:

Did I mention the Dow Transportation Index also broke out?

![]()

![]() So while there are many indicators pointing to the market being “overbought”, sometimes the most bullish thing it does is stay that way for some time. In other words, these warning signals may not come into play in a material way before year-end (but we will keep a close eye on them):

So while there are many indicators pointing to the market being “overbought”, sometimes the most bullish thing it does is stay that way for some time. In other words, these warning signals may not come into play in a material way before year-end (but we will keep a close eye on them):

Now onto the shorter term view for the General Market:

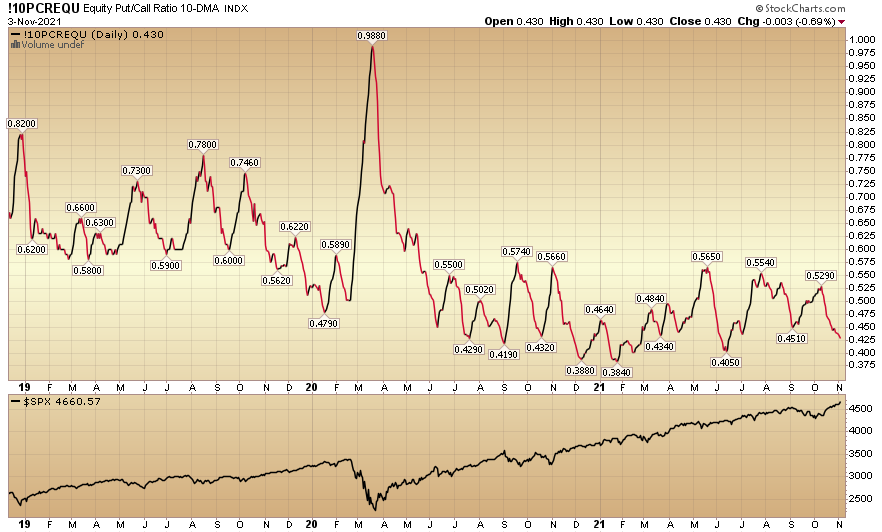

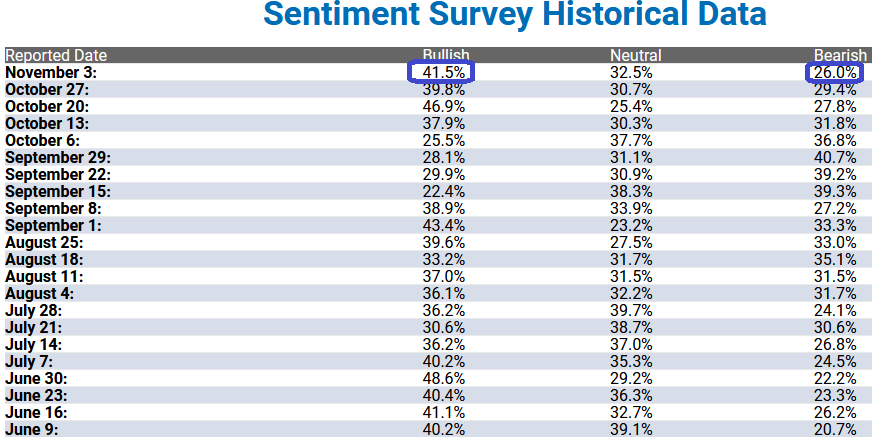

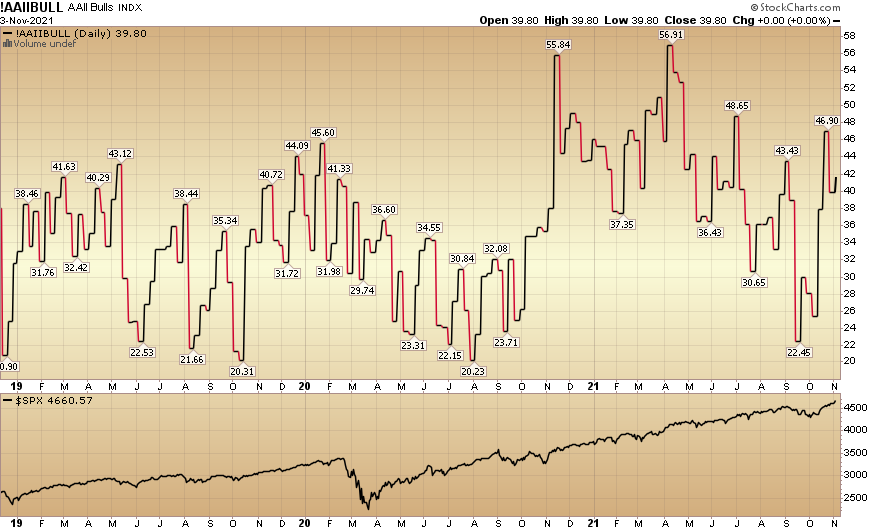

In this week’s AAII Sentiment Survey result, Bullish Percent (Video Explanation) bumped up to 41.5% this week from 39.8% last week. Bearish Percent ticked down to 26% from 29.4% last week.

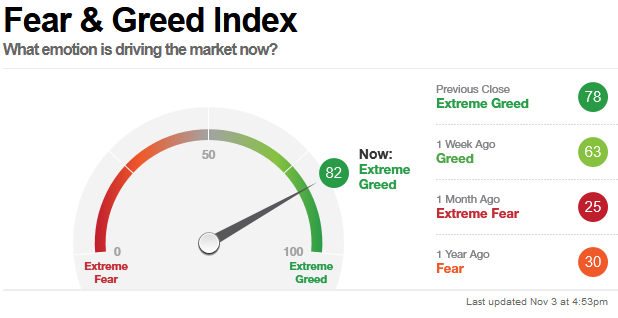

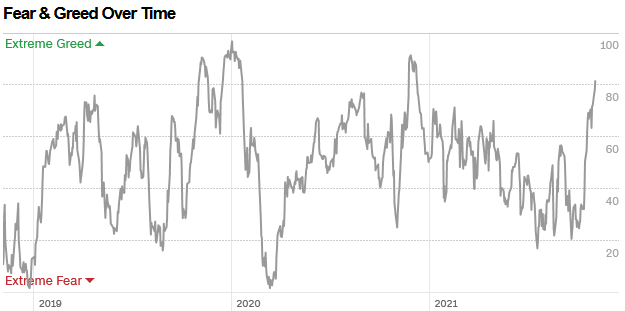

The CNN “Fear and Greed” Index ticked jumped up from 63 last week to 82 this week. Greed is back. You can learn how this indicator is calculated and how it works here: (Video Explanation)

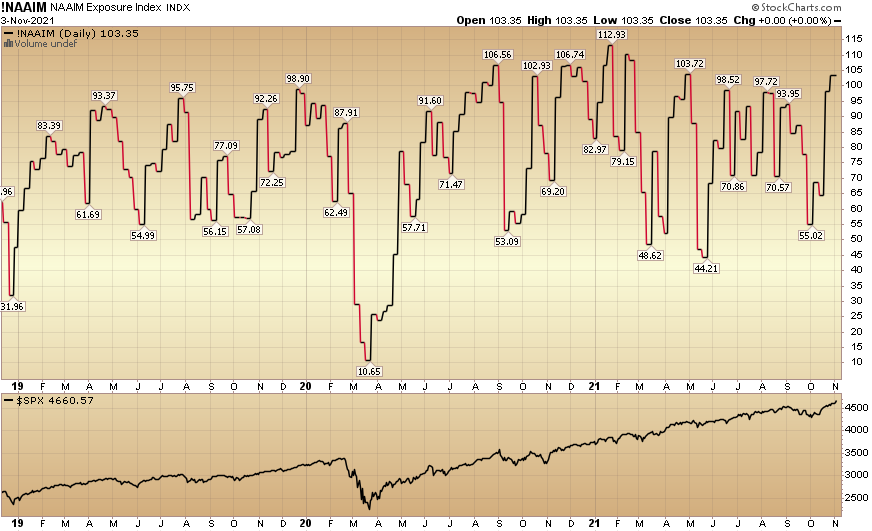

And finally, this week the NAAIM (National Association of Active Investment Managers Index) (Video Explanation) rose to 103.35% this week from 98.02% equity exposure last week. Managers are chasing into year end – as they were underweight with the market pressing higher through earnings season.

There are times to heed warnings and times to ignore them. The Fed will still add another $660B of liquidity to the market over then next 7 months taper period (through bond purchases and reinvestment). We think that although there are numerous indicators flashing yellow (and will come home to roost in 2022), getting too defensive in front of a year-end performance chase – when many managers came into Q3 earnings season short or defensive and now have to play catch-up to match or exceed their benchmarks – is probably not a good idea…

Where is money flowing today?

Data Source: Finviz

Be in the know. 25 key reads for Wednesday…

- Earnings Estimates Are Rising Again. That’s Good for Stocks. (Barron’s)

- VMware’s Solo Act Should Sing (Wall Street Journal)

- No Responsibility. The Energy Report 11/03/2021 (Phil Flynn)

- The RBA’s Defeat Down Under Should Worry Central Bankers (Wall Street Journal)

- The Fed’s Two-Day Meeting Is About to End. What to Expect. (Barron’s)

- Powell Will Have a Tough Time Reeling in the Market’s Rate-Hike Expectations (Barron’s)

- Bed Bath & Beyond Stock Soars 59% on Likely Short Squeeze (Barron’s)

- CVS Boosts Forecast and Earnings Beat Expectations. The Stock Edges Higher. (Barron’s)

- Five Stocks With Safe and Growing Dividends (Barron’s)

- Buy DuPont Stock, Analysts Say. Its Strategic Shift Is ‘Transformative.’ (Barron’s)

- Activision Blizzard Stock Is Falling. Key Game Delays Trump an Earnings Beat. (Barron’s)

- Lyft Stock Gets a Lift from Better-Than-Expected Earnings (Barron’s)

- Jerome Powell’s Dashboard Casts Doubt on Inflation Easing Quickly (Wall Street Journal)

- BP, Buoyed by Resurgent Oil Price, to Boost Investor Returns (Wall Street Journal)

- China Binges on U.S. Gas to Manage Energy Shortage, Carbon Footprint (Wall Street Journal)

- Opioid Makers Win Major Victory in California Trial (New York Times)

- Hong Kong in Talks With China to Open Border, Report Says (Bloomberg)

- Short Sellers Crushed as Bed Bath & Beyond Adds to Avis Blow (Bloomberg)

- China’s PBOC Says Digital Yuan Users Have Surged to 140 Million (Bloomberg)

- Fed to Taper Bonds, Show Patience on Rates: Decision-Day Guide (Bloomberg)

- Companies add 571,000 jobs in October thanks to a big boost in hospitality hires, ADP says (CNBC)

- China Junk Bond Yields Hit All Time High As Property Default Contagion Spreads, Home Sales Plunge 32% (zerohedge)

- Goldman Sachs Upgrades Phillips 66 (PSX) to Conviction Buy (streetinsider)

- Fed prepares to start tapering as US inflation concerns persist (Financial Times)

- ‘It’s really a toy’: Zillow closes home-flipping business. What does that say about the reliability of its Zestimate home-valuation tool? (marketwatch)

Where is money flowing today?

Data Source: Finviz

Be in the know. 24 key reads for Tuesday…

- The Fed Is Boxed In. What It Means for Investors. (Barron’s)

- Soaring Oil and Gas Prices Boost BP Profit in the Shadow of COP26 (Barron’s)

- Intel Chairman Omar Ishrak and Other Insiders Bought $2 Million in Stock (Barron’s)

- 100 million Barrels and Counting. The Energy Report 11/02/2021 (Phil Flynn)

- Mortgage Bond Sales Surged in October (Wall Street Journal)

- The U.S. and EU Shake Up Global Trade (Wall Street Journal)

- Amazon to Launch First Two Internet Satellites in 2022 (New York Times)

- S&P 500 performance in 2022 will be bullish if history is a guide (asiamarkets)

- Wall Street Warns Bond Market Rout Will Catch Up With Stocks (Bloomberg)

- J&J, Teva Beat $50 Billion Opioid Case in First Industry Win (Bloomberg)

- One Trader Calls All the Shots in the Treasury Bond Market (Bloomberg)

- Bond Whiplash Raises Risk of a Financial Market Accident (Bloomberg)

- Small caps kick off November with a rally — why that’s good news for the S&P 500 (CNBC)

- Beijing’s flights are cancelled as China’s capital city tightens Covid restrictions (CNBC)

- China’s coal shortage eases after Beijing steps in, report says (CNBC)

- Bank of America names 13 stocks that are primed to rebound by January after underperforming this year due to tax-loss harvesting (businessinsider)

- Stocks are in ‘melt-up’ mode and have further to run before hitting a top as strong participation drives latest rally, Leuthold CIO says (businessinsider)

- Value investing legend John Rogers told us 4 stocks he’s been buying for the market’s next phase — and why the meme stock and bitcoin rallies remind him of a mistake he made in his earliest days (businessinsider)

- Signs of a new capex cycle’ emerge as S&P 500 companies report earnings, says BofA (marketwatch)

- Opinion: Higher interest rates probably won’t cause this bull market in stocks to end, according to research dating to 1871 (marketwatch)

- Clorox (CLX) Stock Gains 5% Following Q1 EPS Beat, Reaffirmed 2022 Outlook (streetinsider)

- Evercore ISI Reiterates Uber (UBER) as No.1 Mega Cap Pick Ahead of Earnings (streetinsider)

- Pfizer raises 2021 sales forecast for Covid vaccine to $36bn (Financial Times)

- US bond tumult risks triggering stock market volatility, analysts warns (Financial Times)

Tom Hayes – Quoted in Reuters article – 11/1/2021

Thanks to Devik Jain and Bansari Mayur Kamdar for including me in their article on Thomson Reuters today. You can find it here:

Click Here to View The Full Article on Reuters

Where is money flowing today?

Data Source: Finviz

Be in the know. 20 key reads for Monday…

- Here Come the Best 3 Months on the Calendar for Stocks (Barron’s)

- Even if Fed Tightens, Easy Money Will Be Available. That’s Good News for Stocks. (Barron’s)

- Tax Maneuvering Could Create Opportunity in These 7 Beaten-Down Stocks (Barron’s)

- Exxon Mobil as COP26 play? Here’s why Morgan Stanley says some of the dirtiest companies will benefit from decarbonization. (marketwatch)

- XPeng’s stock rallies after October deliveries update, Li Auto’s slip (marketwatch)

- One Upside to Economic Woes May Be China-U.S. Thaw (Wall Street Journal)

- Delta Surge of Covid-19 Recedes (Wall Street Journal)

- Global Climate Talks Face Hurdles After G-20 Nations Struggle to Find Common Ground (Wall Street Journal)

- Wages and Prices Are Up, but It Isn’t a Spiral—Yet (Wall Street Journal)

- A contraction in China’s factory activity worsened for a second straight month in October, adding evidence that growth momentum has weakened. (Wall Street Journal)

- Uber and Lyft Thought Prices Would Normalize by Now. Here’s Why They Are Still High. (Wall Street Journal)

- Investment in Brazilian Startups Is Booming (Wall Street Journal)

- China’s Popular Electric Vehicles Have Put Europe’s Automakers on Notice (New York Times)

- Bank of America to Apply to Set Up Brokerage Unit in China (Bloomberg)

- Tesla’s Hidden Billionaire: How a Retail Trader Made $7 Billion (Bloomberg)

- Erdogan Says He Expects Biden to Help With F-16 Approvals: AHBR (Bloomberg)

- OPEC+ Balks At Biden’s Demands For More Oil Production (ZeroHedge)

- 5 Big Dividend Biotech and Pharmaceutical Stocks Have Strong Upside Potential (247wallst)

- Will the ailing Turkish economy bring Erdogan down? (Financial Times)

- Yellen says U.S economy is not overheating (Reuters)

Be in the know. 26 key reads for Sunday…

- Danbury’s Glover Teixeira wins UFC title, tells city residents ‘Never give up on your dreams’ (newstimes)

- “10 To 20 Asset Managers Are Being Liquidated” – Rate Vol Exploding Just As Funds Pile Into Repo Trade That Blew Up Market (ZeroHedge)

- For Harry Houdini, Séances and Spiritualism Were Just an Illusion (smithsonianmag)

- November’s First Trading Day: DJIA Up Over 1% Three Years in a Row (Almanac Trader)

- America’s Favorite Race Car Ain’t No Miata (roadandtrack)

- Morgan Plus Four CX-T Review: Ready For Your Next Adventure (Forbes)

- The Disrespect (thereformedbroker)

- PagSeguro: The ‘Square of Brazil’ Is a Value Buy (gurufocus)

- ECRI Weekly Leading Index Update (advisorperspectives)

- A LONGER TERM LOOK AT OIL — ENERGY STOCKS TESTING MAJOR TRENDLINE (stockcharts)

- Xi Hasn’t Left China in 21 Months. Covid May Be Only Part of the Reason. (dnyuz)

- Riding high off vaccine wins, Pfizer CEO Albert Bourla delves into his strategy for the year ahead (Fortune)

- Inside the reopening of one of the most luxurious hotels in St. Barths (fortune)

- SpaceX Is Expected to Become Even More Valuable Than Tesla, According to Morgan Stanley (RobbReport)

- From Alabama to Wyoming: The Most Expensive Home for Sale in Every State (robbreport)

- The 2023 Corvette Z06 Has Just Been Unveiled—and It Doesn’t Disappoint (architecturaldigest)

- Best Halloween Candy, Ranked (gawker)

- ICON to build largest 3D printed community of 100 homes co-designed by BIG (designboom)

- What I Discovered at My First F1 Race (thedrive)

- The Real Roots of Midlife Crisis (getpocket)

- Learn Anything Faster By Using The Feynman Technique (cantorsparadise)

- The Bonfire of the Currencies? (project-syndicate)

- Internal vs. External Benchmarks (collaborativefund)

- Craig Fuller on the Huge Challenge of Getting the Ports To Operate 24/7 (bloomberg)

- Dan Alpert on the Big Difference Between Now and the 1970s (bloomberg)

- Keanu Reeves Surprised His John Wick Stuntmen with Rolex Submariners (gq)