Key Market Outlook(s) and Pick(s)

On Monday, I joined Stuart Varney on Fox Business’ Varney & Co. to discuss markets, the economy, earnings, the consumer, Advance Auto Parts ($AAP), VF Corp ($VFC), and more. Thanks to Stuart and Maggie Edwards for having me on:

On Tuesday, I joined my friend Lou Basanese on his podcast TheBigSkinny to discuss markets, the economy, earnings, the consumer, 3 picks and a lot more. Thanks to Lou and his great team for having me on:

Intel Update

For newer readers, here’s a brief overview of the key drivers behind our Intel thesis, a once left for dead semiconductor giant with a legacy CPU and server franchise back in vogue, alongside a growing foundry business at the center of the U.S. push to rebuild advanced chip manufacturing:

A year ago, the conversation around Intel was whether it could survive. Today, it’s about how fast it can add capacity to meet enormous demand.

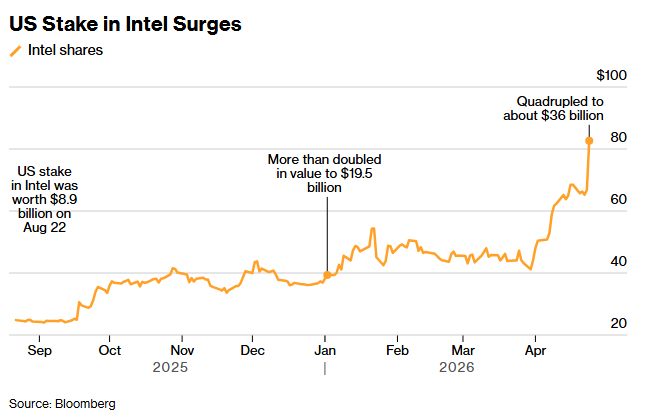

That single shift, captured by Lip-Bu Tan on this quarter’s earnings call, sums up the entire arc of our INTC investment better than anything we could write. The same TSMC that watched Intel’s manufacturing arm struggle for the better part of a decade is now publicly calling INTC a “formidable competitor.” The same analysts who downgraded the stock in the hole at $19 are now tripping over themselves to hike price targets. And the same Treasury that picked up its $8.9B stake at $20.47/share is now sitting on over $36B today, a ~4-bagger for Uncle Sam that will go down as one of the greatest trades in taxpayer history.

Admittedly, we were a bit nervous heading into this print, with the stock trading at ~118x earnings after a ~236% rally over the past year to levels not seen since 2000. There was clearly a lot of optimism baked in, whether from the long-awaited prospect of external foundry customers, packaging deals, or growing excitement around the CPU revival. Those factors set a high bar for Intel to clear.

The good news is that INTC didn’t just clear it. It blew it out of the water.

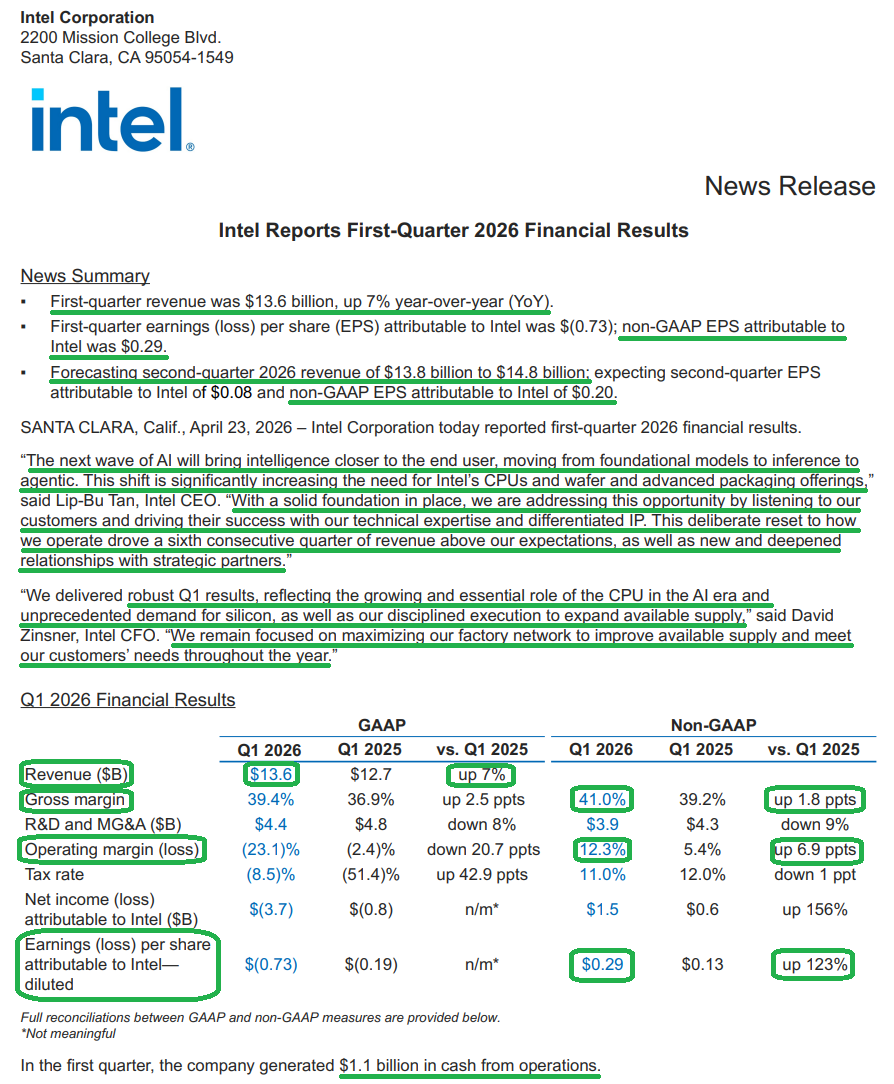

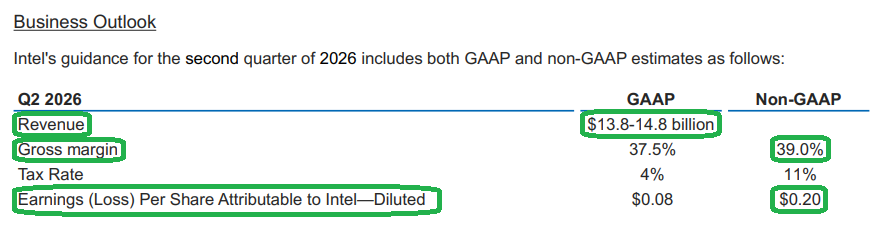

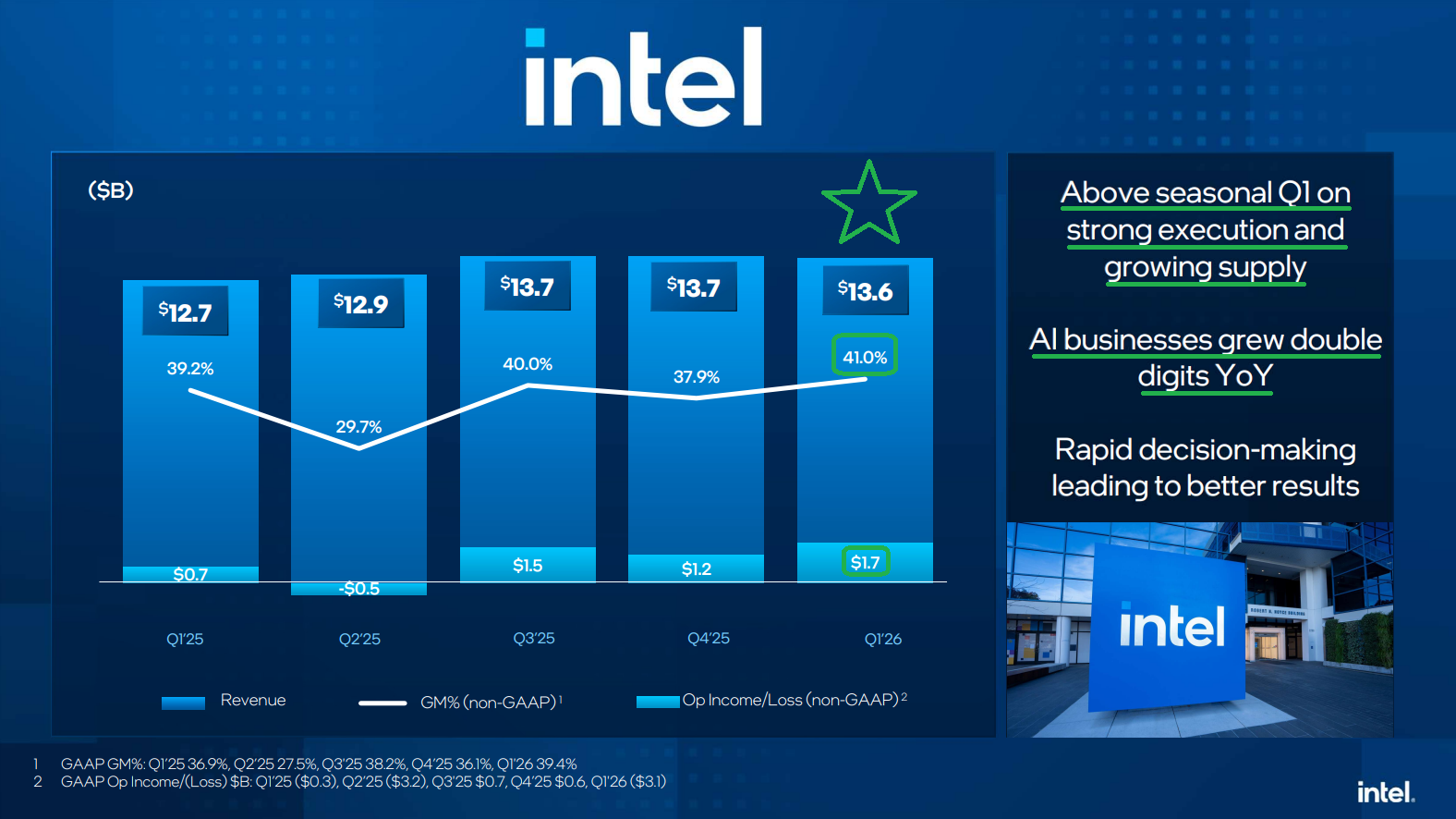

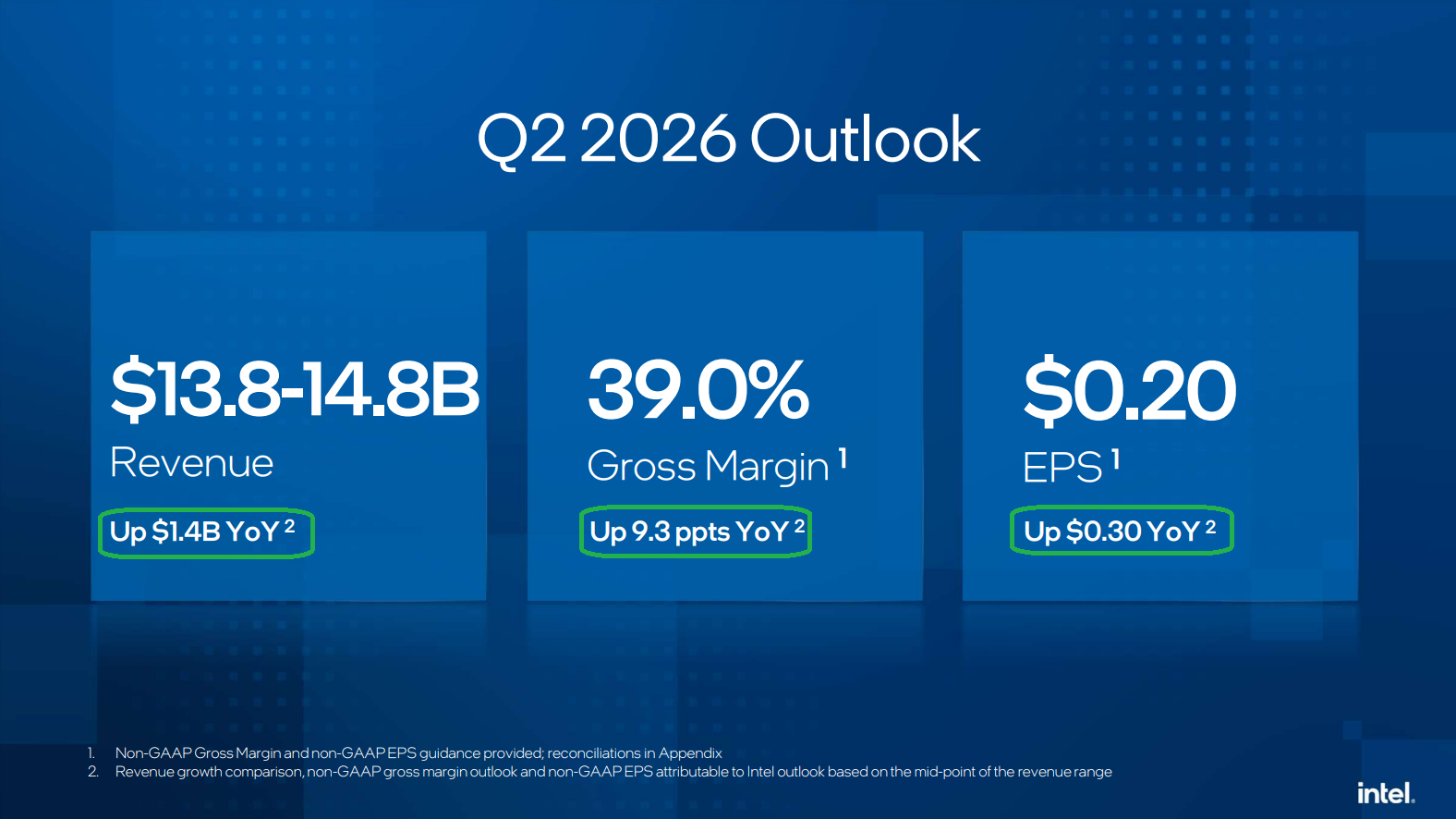

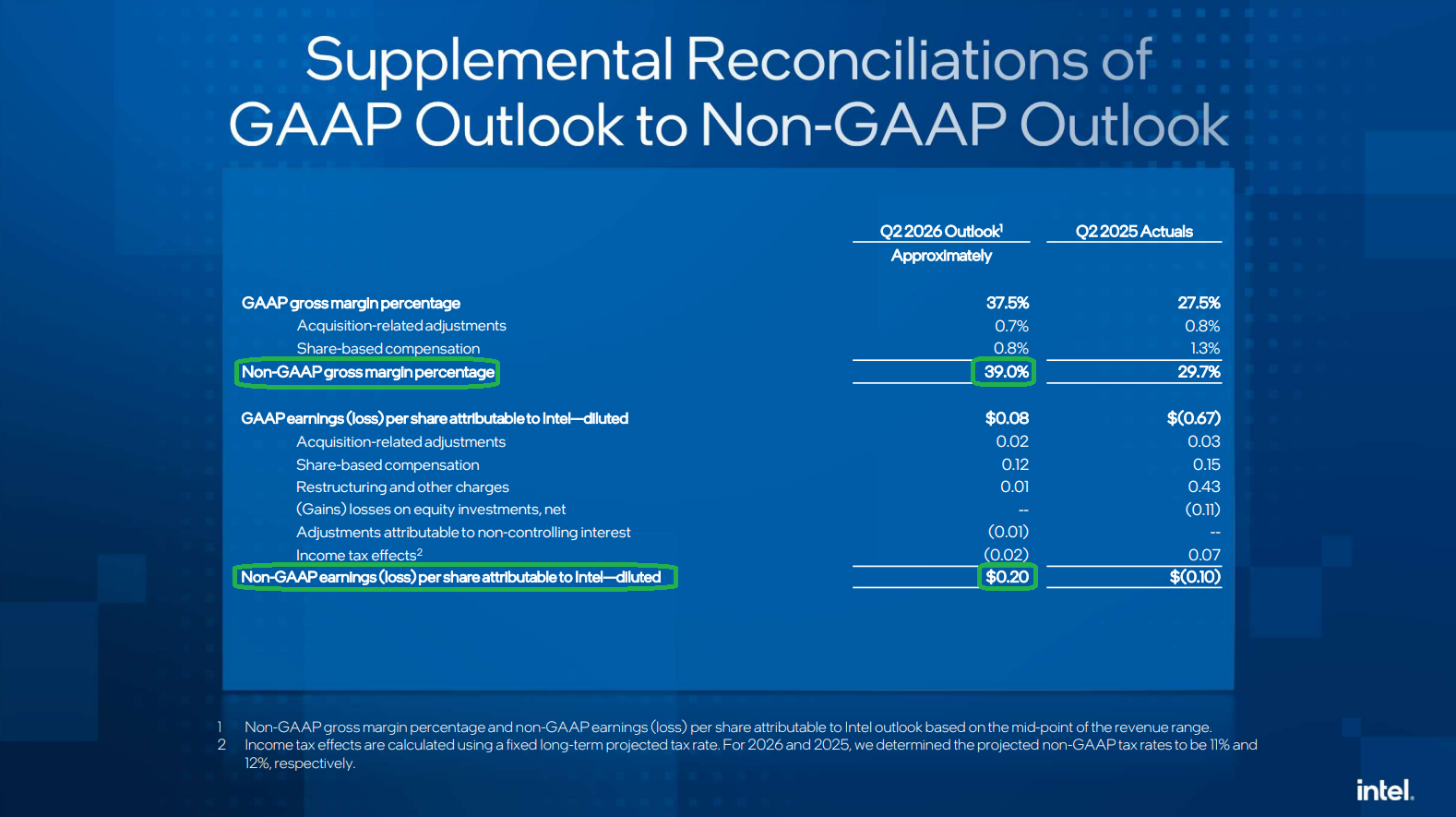

Revenue of $13.58B (+7.2% Y/Y) came in $1.4B above the prior guidance midpoint and ahead of Street consensus of $12.42B. Adjusted EPS of $0.29 crushed breakeven consensus, while adjusted gross margins of 41% beat guidance by 650 bps and marked the highest level in five quarters. Most importantly, no let-up is in sight, with Q2 guidance calling for revenue of $14.3B (+11% Y/Y) and EPS of $0.20 (+$0.30 Y/Y), both well above Street estimates.

The print and guide were enough to remove any remaining question marks and prove the turnaround is taking hold, sending the stock up 24% and setting fresh all-time highs.

Results were driven by demand that now stretches as far as the eye can see and is so thoroughly outstripping supply that INTC is selling chips it had previously written off as scrap. While management declined to quantify the unmet demand opportunity, they made clear it’s meaningful and that “it starts with a B.”

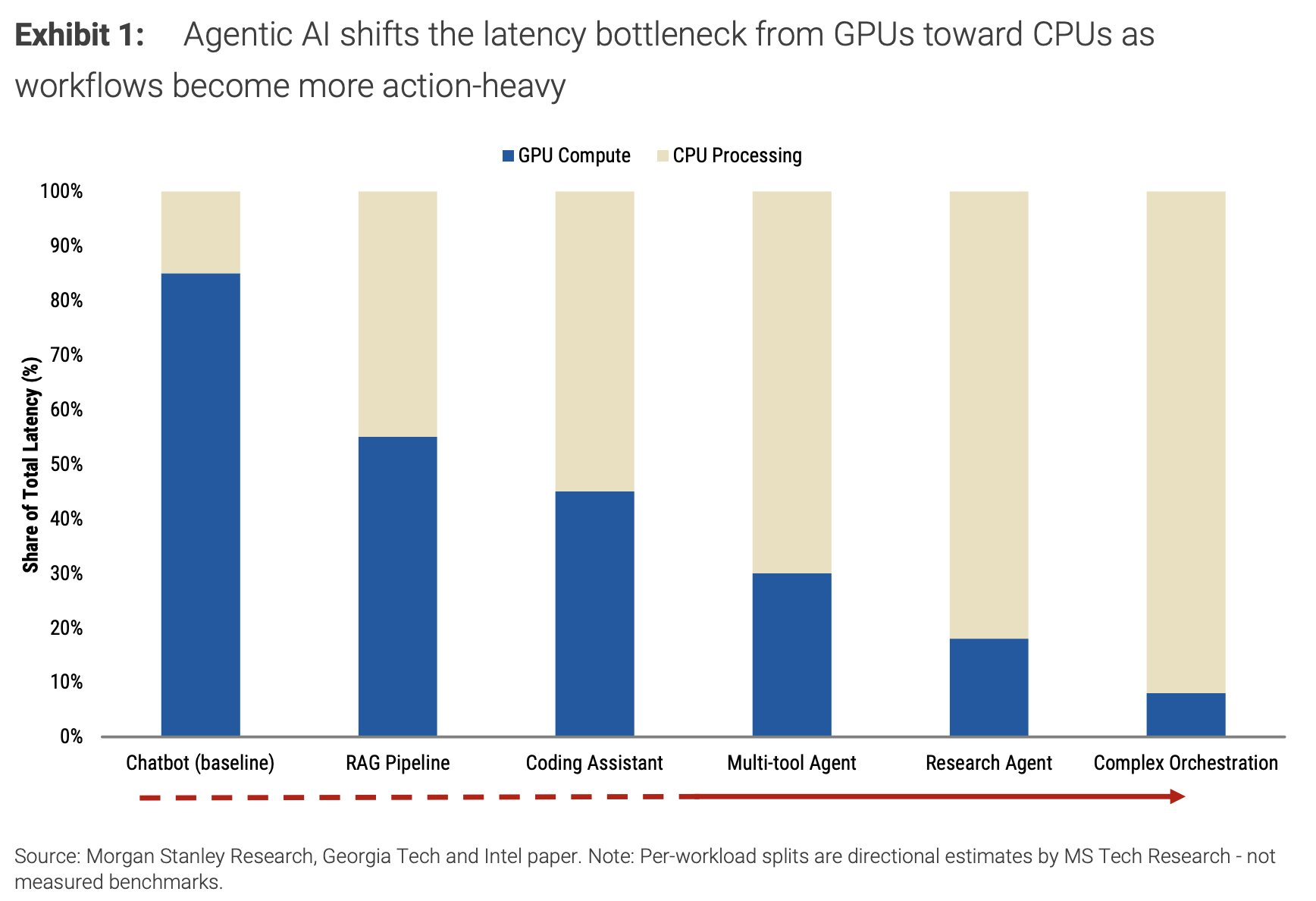

The bigger story is what’s driving the demand. For the past several years, the AI story has been dominated by GPUs and accelerators, with INTC and the “boring” CPU business cast as the casualty. That story is now reversing in spades. As compute shifts from training to inference, and from chatbots to agents, the historical CPU-to-GPU ratio of 1:8 has compressed to 1:4, with management seeing a path to 1:1 or even a tilt toward CPUs.

As the humble CPU reinserts itself as a foundation of the AI era, Intel, the most dominant CPU franchise on the planet, stands to be a massive beneficiary.

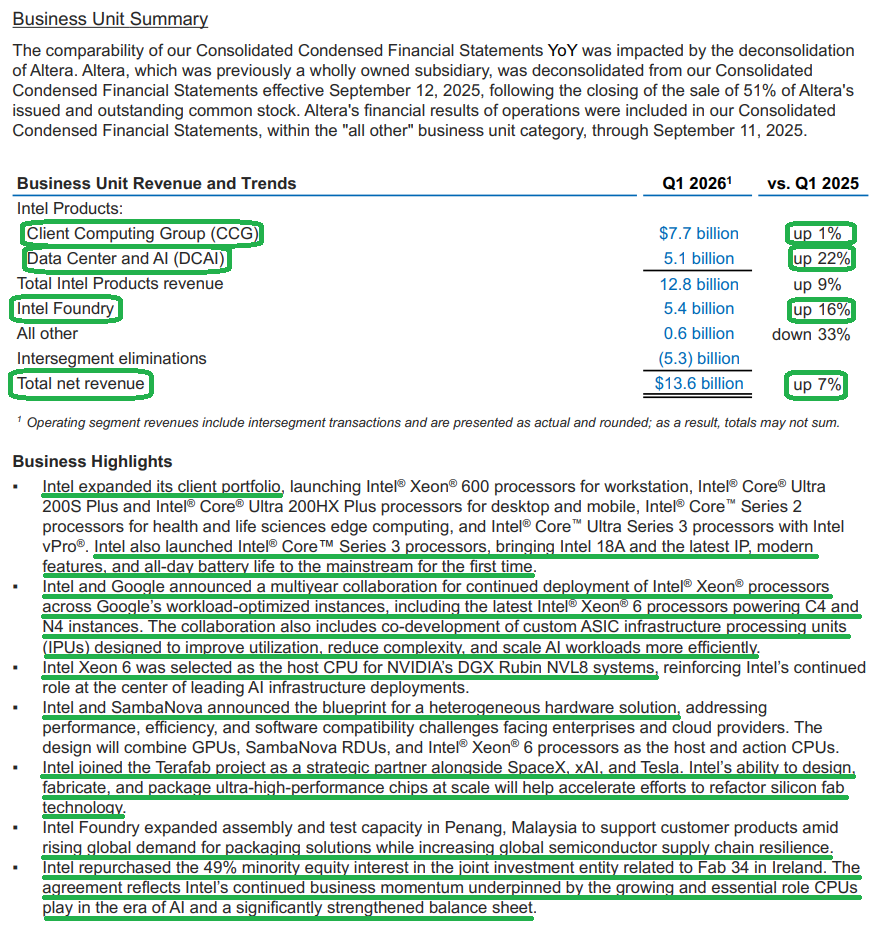

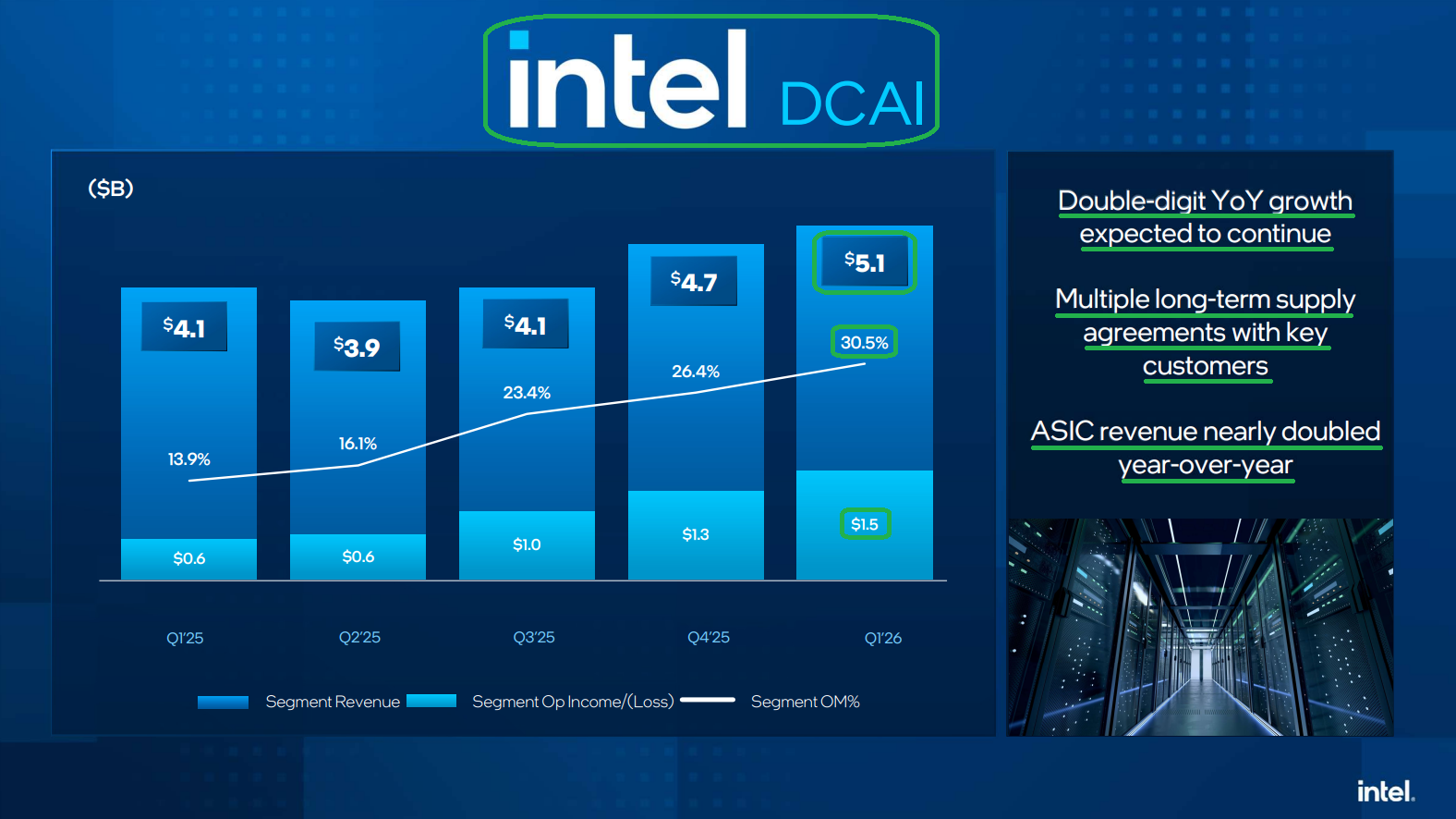

That’s why DCAI revenue grew 22% Y/Y this quarter to $5.1B, with operating profit more than doubling Y/Y to $1.5B. It’s why Google signed a multiyear agreement for Xeon deployment, with management hinting that other LTAs of similar scope have been signed but not announced. It’s why Xeon 6 was selected as the host CPU for NVIDIA’s DGX Rubin NVL8 systems. It’s why the ASIC business is already running at a $1B+ run rate, up more than 30% Q/Q and nearly doubling Y/Y. And it’s why management now sees double-digit unit growth not just in the quarters ahead but in the years ahead.

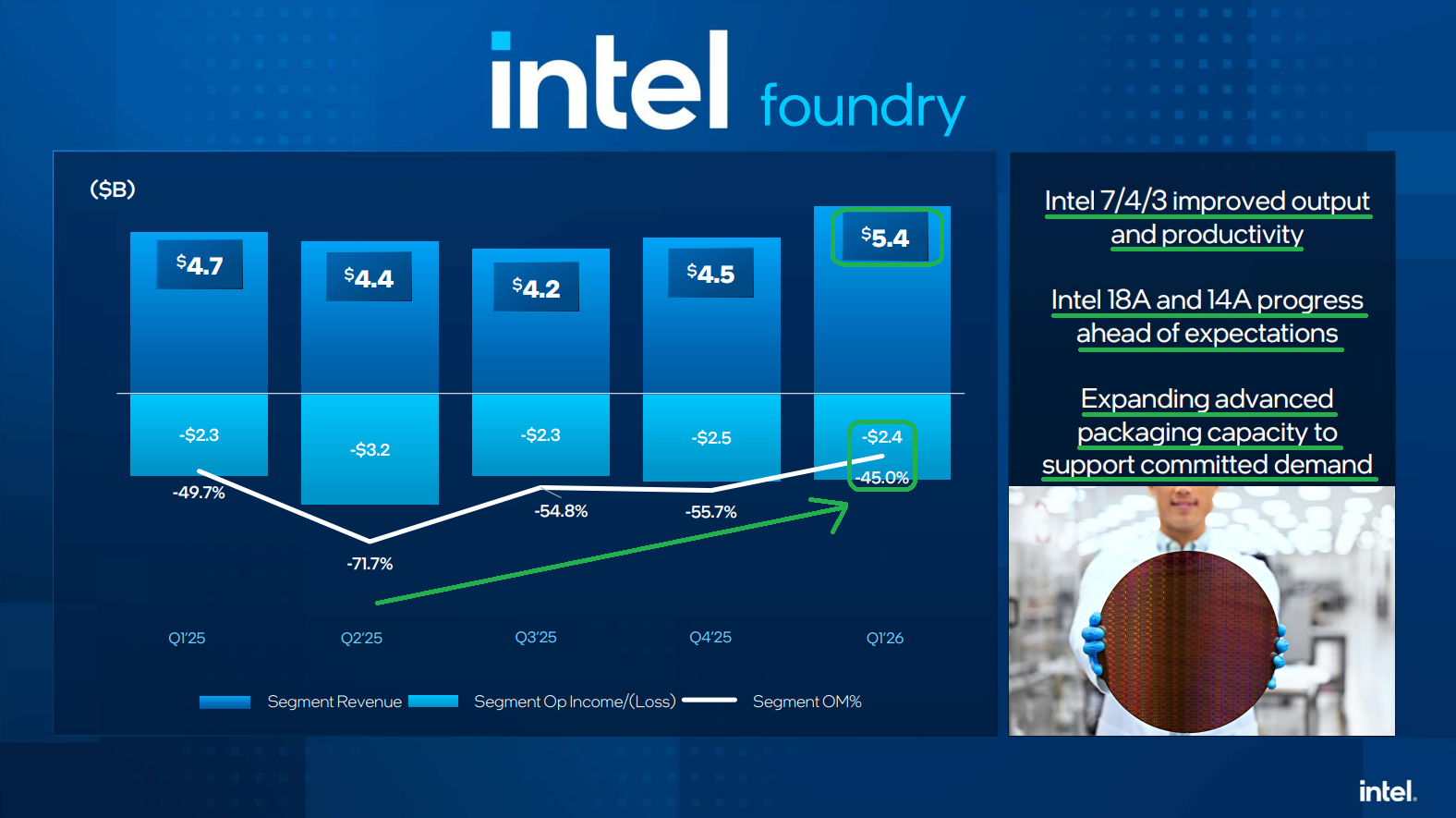

Then there’s the foundry business, which has gone from a cash-incinerating existential question mark to a legitimate strategic asset almost overnight. Prior to earnings, we got the long-awaited news of Intel’s first major external 14A customer commitment, with Elon confirming on Tesla’s call that he plans to use Intel’s “state of the art” 14A process for Tesla, SpaceX, and xAI on the Terafab project. This was always the whipped cream and cherries portion of our original underwriting, a thesis that’s now being validated almost daily.

Which brings us to how we’re positioned today.

When we sold half the position into the move heading into Q4 earnings at ~$55, we walked through the logic in detail on the podcast and in the weekly article. The stock had run from below liquidation value of ~$22/share to $55+ in less than a year, fully pricing in a recovered legacy CPU and server business. Any further upside was effectively the market betting on a near-term external foundry customer announcement. Hope should never be an investment thesis, and we were more than happy to book a 2.5x gain in eighteen months and let the rest ride as a free flyer.

Following this quarter’s results, we trimmed again, booking what has now become a 4-bagger in a matter of ~2 years.

The same logic applies as last quarter. At $82/share, you’re now paying for a fully recovered legacy business (originally assigned $45 to $50 in value) that’s riding the AI CPU wave, plus a foundry business that has finally started landing external customers, though still years out from converting to meaningful revenue. That’s a lot of good news and forward expectations already embedded in the price.

That doesn’t mean we don’t believe in Intel.

In terms of what INTC has already delivered to this point, the stock is without question overvalued. But in terms of what we think it WILL deliver over the next several years, with margins inflecting from trough levels, external foundry revenue beginning to convert, and a structural change in the demand backdrop for CPUs, the stock is still likely inexpensive. Both statements can be true at once. The only difference is that we’re now effectively playing with house money, with our remaining stake a free flyer on the upside scenario that costs us nothing relative to the gains already booked.

And if there’s one person we want at the wheel for what comes next, it’s Lip-Bu Tan. We’ve covered his Cadence track record before, and the math hasn’t changed. Betting against him has never been a profitable trade.

At the end of the day, markets overshoot in both directions. That’s human behavior. In the case of Intel, sentiment has moved from despondency to euphoria in a very short period of time. Our job is to take advantage of those dislocations, not get swept up in them.

Q1 Earnings Breakdown

10 Key Points

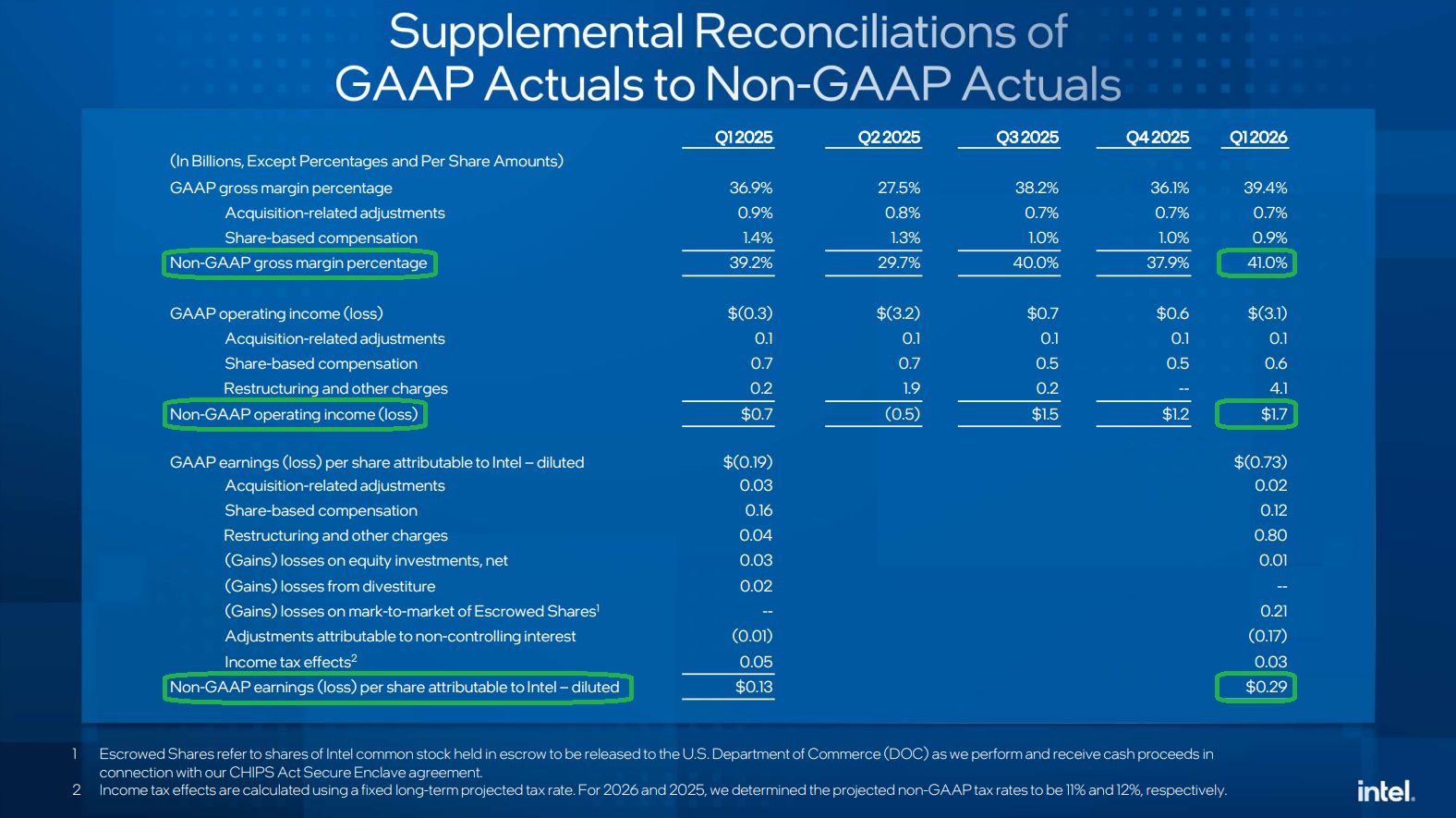

1) Intel topped expectations across the board for the sixth straight quarter, with results coming in well above the high end of prior guidance on revenue and EPS. Revenue of $13.58B (+7.2% Y/Y and roughly flat Q/Q) was $1.4B above the prior guidance midpoint of $12.2B and ahead of Street consensus of $12.42B. Adjusted EPS of $0.29 (+123% Y/Y) crushed prior breakeven guidance and Street estimates of $0.01.

2) Adjusted gross margins of 41% (+180 bps Y/Y) came in well above prior guidance of 34.5%, while adjusted operating margins of 12.3% expanded 690 bps Y/Y. Management made it clear that further margin expansion remains a top priority from trough levels of just over 36% seen in both FY24 and FY25, eyeing a path back toward 40%+ in the near term, with plenty of room to move higher over time compared to Intel’s heyday of consistent 60%+ gross margins.

3) Data Center and AI Group (DCAI) revenue of $5.1B (+22% Y/Y and +7% Q/Q) beat consensus of $4.4B. Segment operating profit of $1.5B (~31% operating margins) more than doubled Y/Y from $0.6B and rose $292M Q/Q on improved product margins, better cycle times, and stronger yields on Intel 3. Server CPU supply is effectively sold out through 2026, with factories running above 100% capacity and management noting that the unmet demand revenue opportunity “starts with a B.” Management now expects double-digit segment growth to continue through 2026 and into 2027. Intel also signed multiple long-term agreements during the quarter, including a multiyear collaboration with Google for continued deployment of Xeon processors, while Xeon 6 was selected as the host CPU for NVIDIA’s DGX Rubin NVL8 systems.

4) Client Computing Group (CCG) revenue of $7.7B (+1% Y/Y and -6% Q/Q) beat consensus of $7.1B, helped by Core Ultra Series 3 representing the strongest CCG product launch in five years and AI PC revenue growing 8% Q/Q to ~60% of the client CPU mix. That said, management is prudently planning for PC demand to weaken in the second half as memory shortages and rising component prices weigh on pricing, with full-year PC unit TAM now expected to decline by the low double digits despite near-term orders remaining robust. As a result, client revenue is expected to be roughly flat from Q2 onward.

5) Intel Foundry posted revenue of $5.4B (+16% Y/Y and +20% Q/Q), with external foundry revenue reaching $174M. Segment operating loss improved by $72M Q/Q to $2.4B on better yields across Intel 4, 3, and 18A, partially offset by an intentional step-up in 14A investment to support external customer evaluations. The advanced packaging backlog continues to grow, with management now confident these opportunities will be worth billions per customer rather than the hundreds of millions previously expected. Intel also announced a multiyear expansion of back-end facilities in Malaysia to support rising global demand for packaging solutions, which is expected to begin converting to revenue in 2027.

6) Tesla, SpaceX, and xAI committed to using Intel’s 14A process for the Terafab project, confirmed by Elon Musk on Tesla’s Q1 call, where he called it “state of the art.” This is the first major external 14A customer announcement and arrives ahead of management’s prior timeline, which had pointed to firm customer decisions beginning in H2 2026 and extending into H1 2027. Beyond Terafab, management noted that 14A yield and performance are outpacing 18A at the same point in maturity, with multiple additional customers actively evaluating the technology and PDK development progressing faster than 18A did. Management continues to point to firm customer decisions beginning in H2 2026, with Investor Day in H2 a potential platform, and extending into H1 2027.

7) Intel 18A is still early in its ramp but is tracking ahead of internal expectations, with management noting that the original year-end yield target will likely be achieved by mid-year, a meaningful pull-forward driven by a deliberate push on yields and cycle times. 18A is now powering Core Ultra Series 3 in full-volume production ramp, which, alongside Intel 3-based Xeon 6, represents the fastest new product ramp at Intel in five years. That said, 18A remains a near-term gross margin headwind given the early-ramp cost structure, with management still expecting a multi-quarter path before foundry margins on 18A reach the segment average.

8) The big driver behind the explosive growth in DCAI is a structural shift in AI workload mix that is finally tilting toward Intel’s CPU franchise. Management noted that the shift in compute from training to inference and agentic applications has already narrowed the historical CPU-to-GPU ratio from 1:8 to 1:4, with a path toward 1:1 or even a tilt toward CPUs amid the continuing migration toward inference and agentic workloads. Management is confident this structural shift in demand for the CPU franchise will be a meaningful growth engine in the years ahead, not just quarters, with strong visibility into double-digit unit growth for both the industry and Intel.

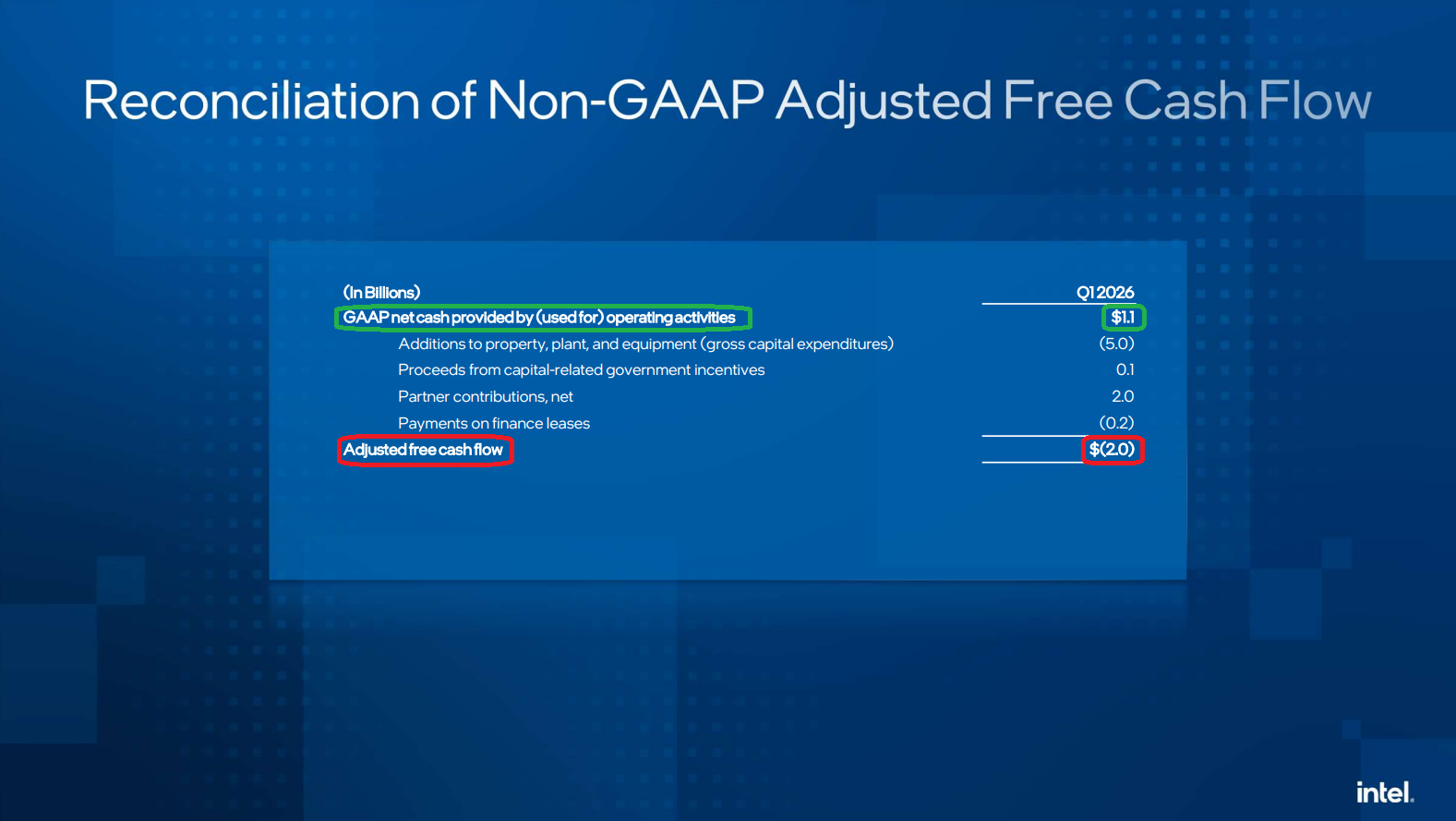

9) Capex will now be roughly flat Y/Y (vs. FY25 capex of $17.7B), compared to prior plans for reduced spending, with tool spending now expected to rise ~25% Y/Y as Intel leans into demand while pulling back materially on new space. Q1 operating cash flow was $1.1B against gross capex of $5B, producing adjusted FCF of -$2B, though management still expects positive adjusted FCF for the full year, excluding the Fab 34 joint investment buyout. The Fab 34 buyout, which closed during the quarter, repurchased the 49% JV equity interest in the Ireland facility for $7.7B in cash and $6.5B in new debt, a highly accretive deal that allows shareholders to capture the full economic benefits from a fab now hitting its stride.

10) Q2 guidance came in well above consensus expectations, with revenue of $13.8B to $14.8B (+2% to +9% Q/Q) versus Street estimates of $13.07B, and adjusted EPS of $0.20 versus consensus of $0.09. At the midpoint of $14.3B, that implies revenue of +$1.4B Y/Y, gross margins of 39% (+930 bps Y/Y), and EPS up $0.30 Y/Y. Management did flag that 2026 opex is now likely to come in above the prior $16B target due to inflationary pressures, variable comp, and targeted investments to capture the opportunities ahead.

Earnings Call Highlights

Morningstar Analyst Note

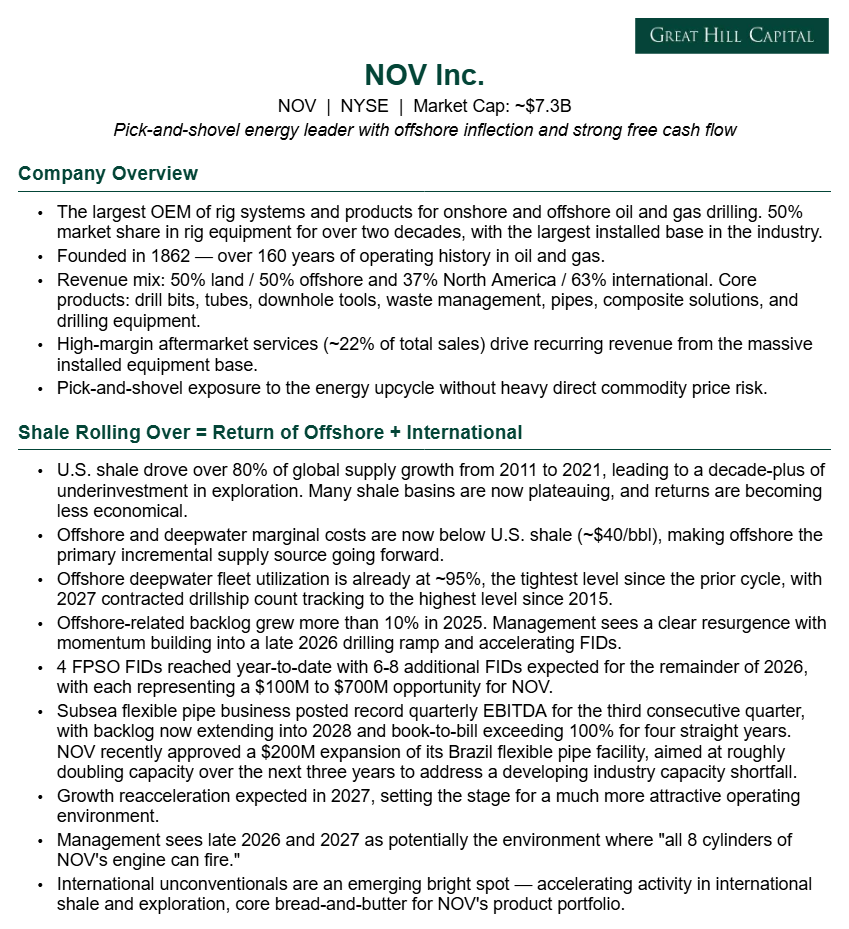

National Oilwell Varco

For newer readers, here’s a brief overview of our NOV thesis, a pick-and-shovel oilfield equipment leader positioned for an accelerating energy upcycle as offshore and international reassert themselves after a decade-plus of underinvestment:

Q1 Earnings Breakdown

10 Key Points

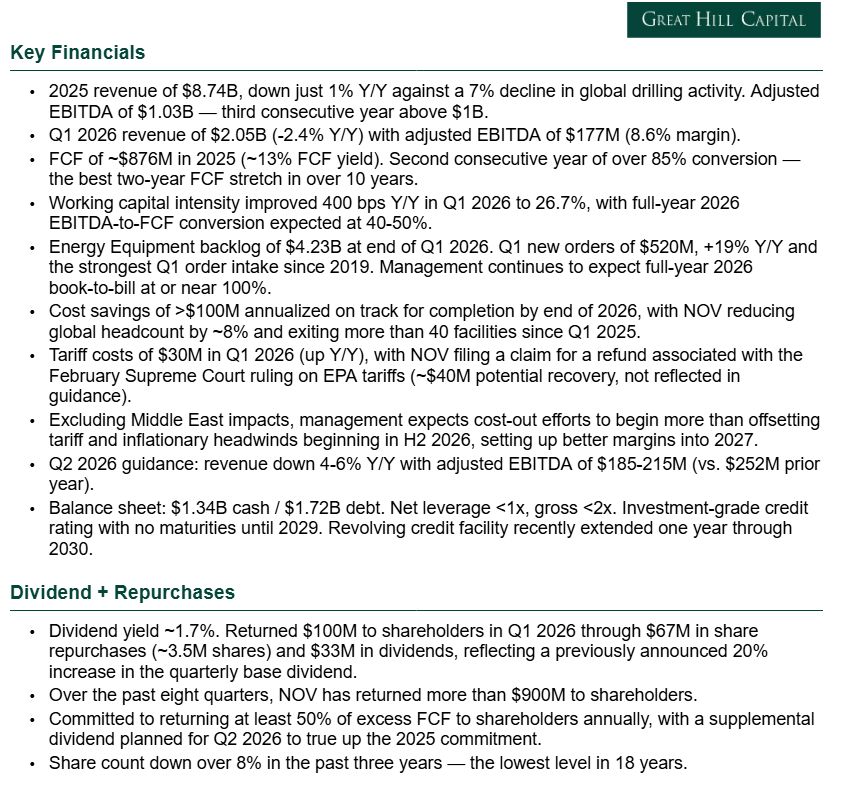

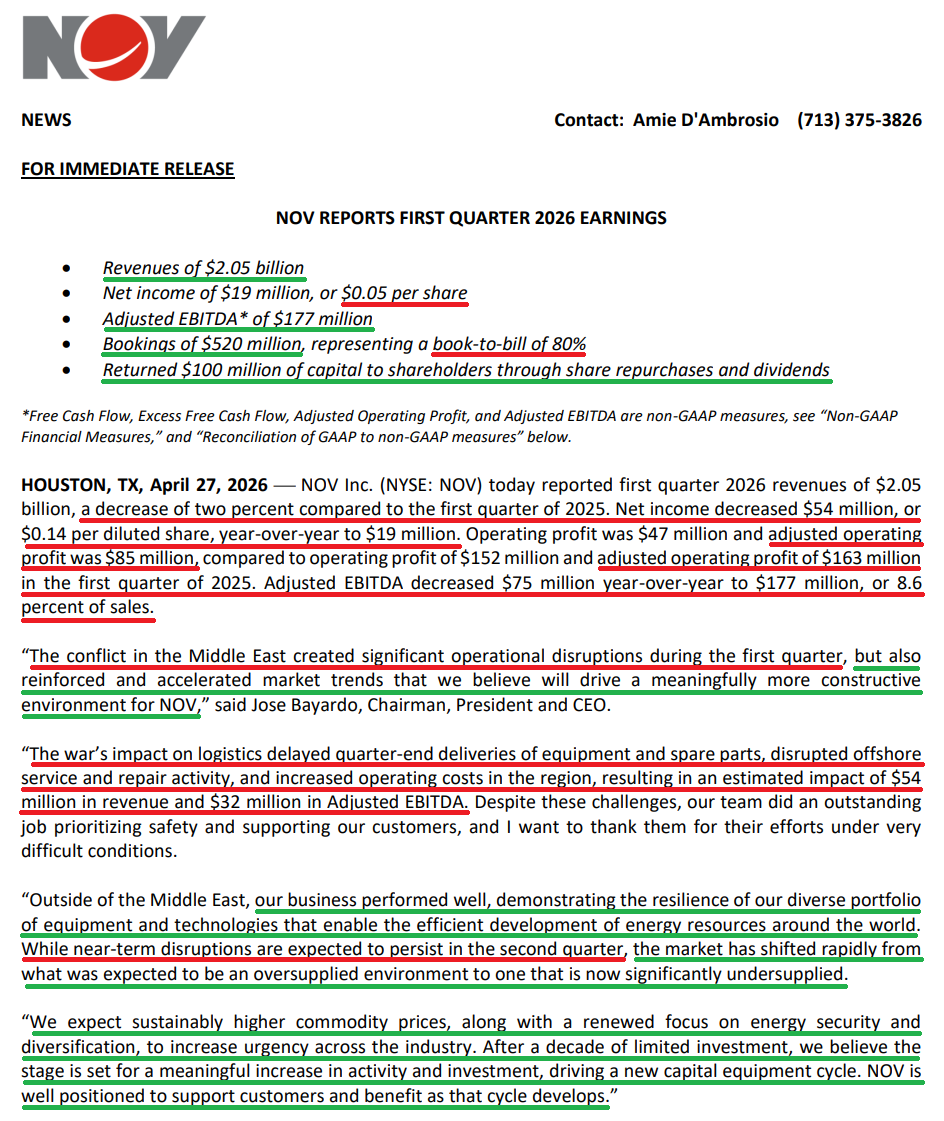

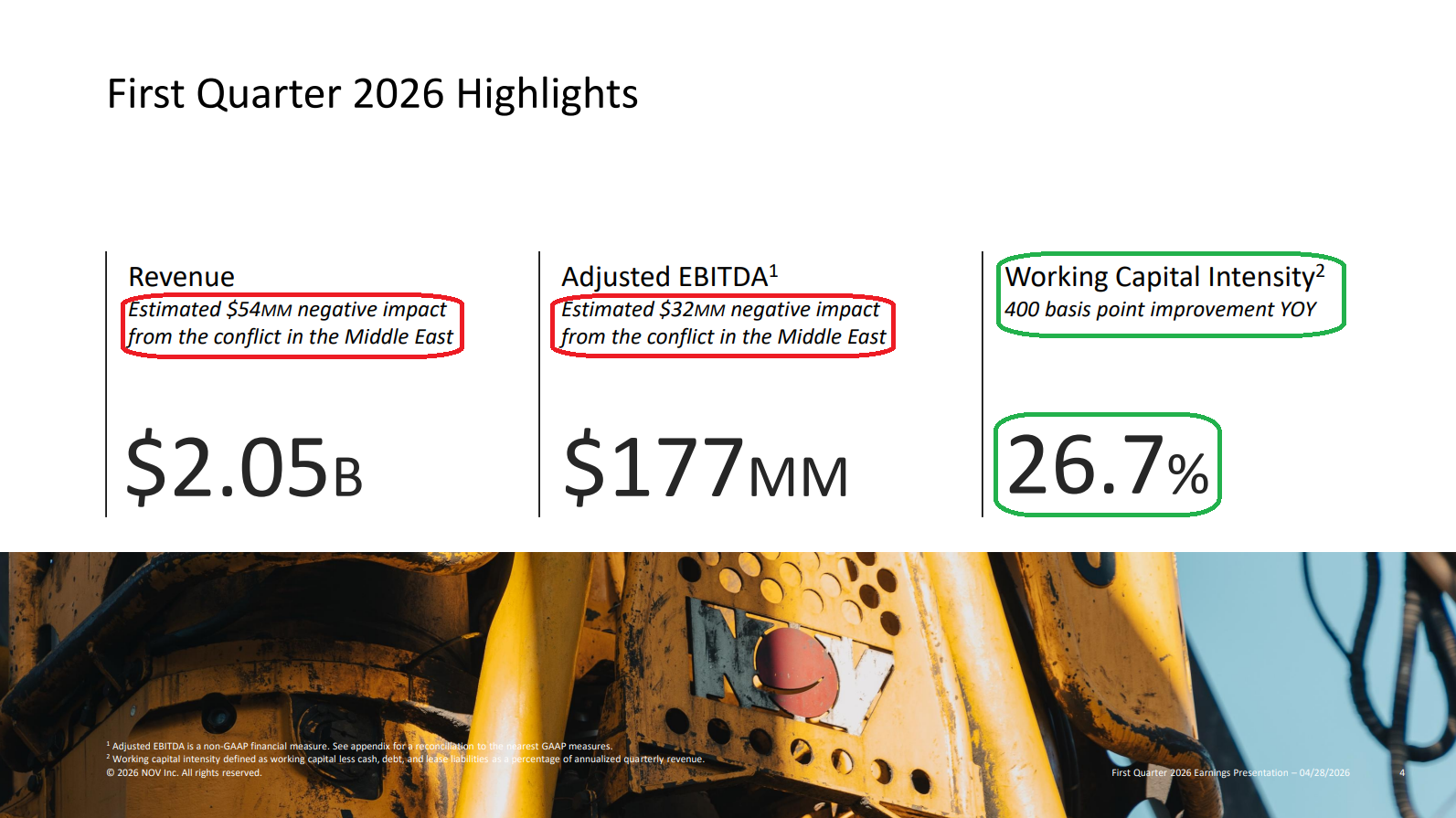

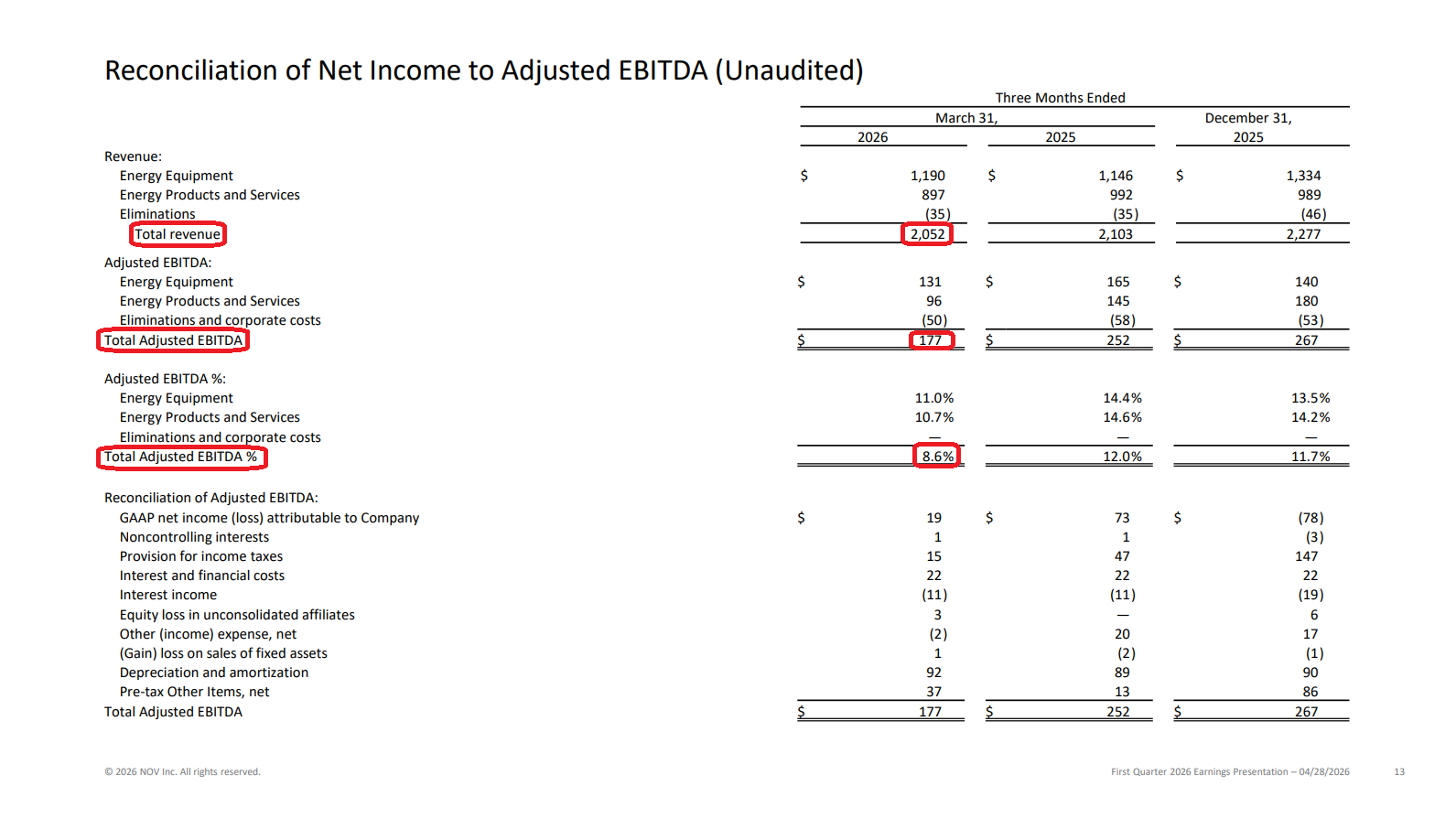

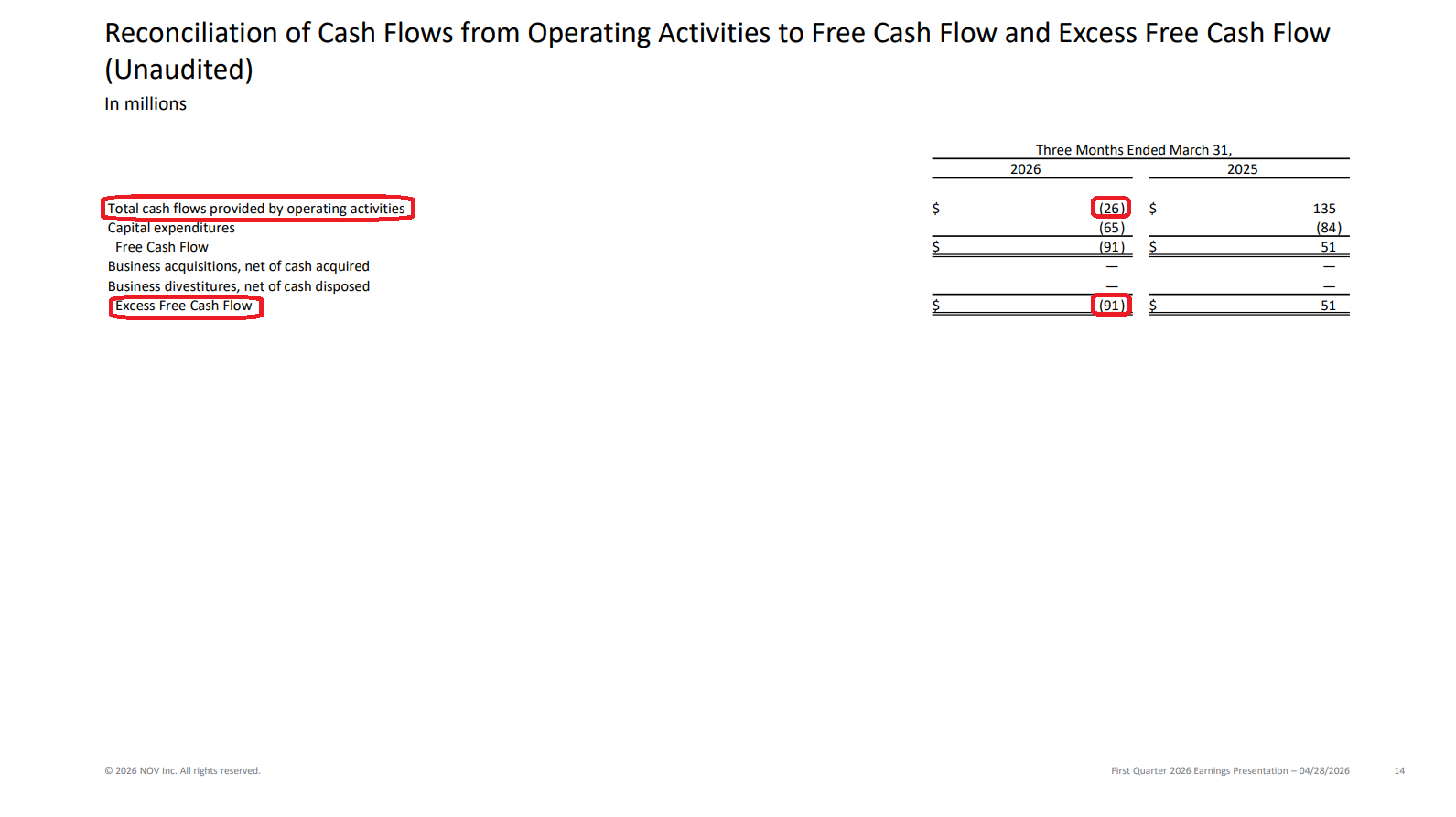

1) NOV reported Q1 revenue of $2.05B (-2.4% Y/Y and -10% Q/Q), in line with consensus and pre-announced results. Management estimated a ~$54M headwind to Q1 revenue from the conflict in the Middle East, noting that, adjusted for this impact, Y/Y revenue would have been roughly flat. Adjusted EPS of $0.11 missed consensus by $0.04.

2) Adjusted EBITDA came in at $177M, in line with pre-announced results, down $75M Y/Y to 8.6% of sales versus 12.0% in the prior year. Adjusted EBITDA was pressured by an estimated $32M Middle East impact, driven by higher operating costs from increased freight expenses and lower absorption at manufacturing facilities. Management continues to execute against its ongoing $100M cost-out program, having reduced global headcount by ~8% and exited more than 40 facilities since Q1 2025. These initiatives have been largely offset by tariff costs, IT investments, and inflationary pressures to date, but excluding Middle East impacts, management expects them to more than offset tariffs and inflation beginning in H2 2026, setting up improved margins into 2027.

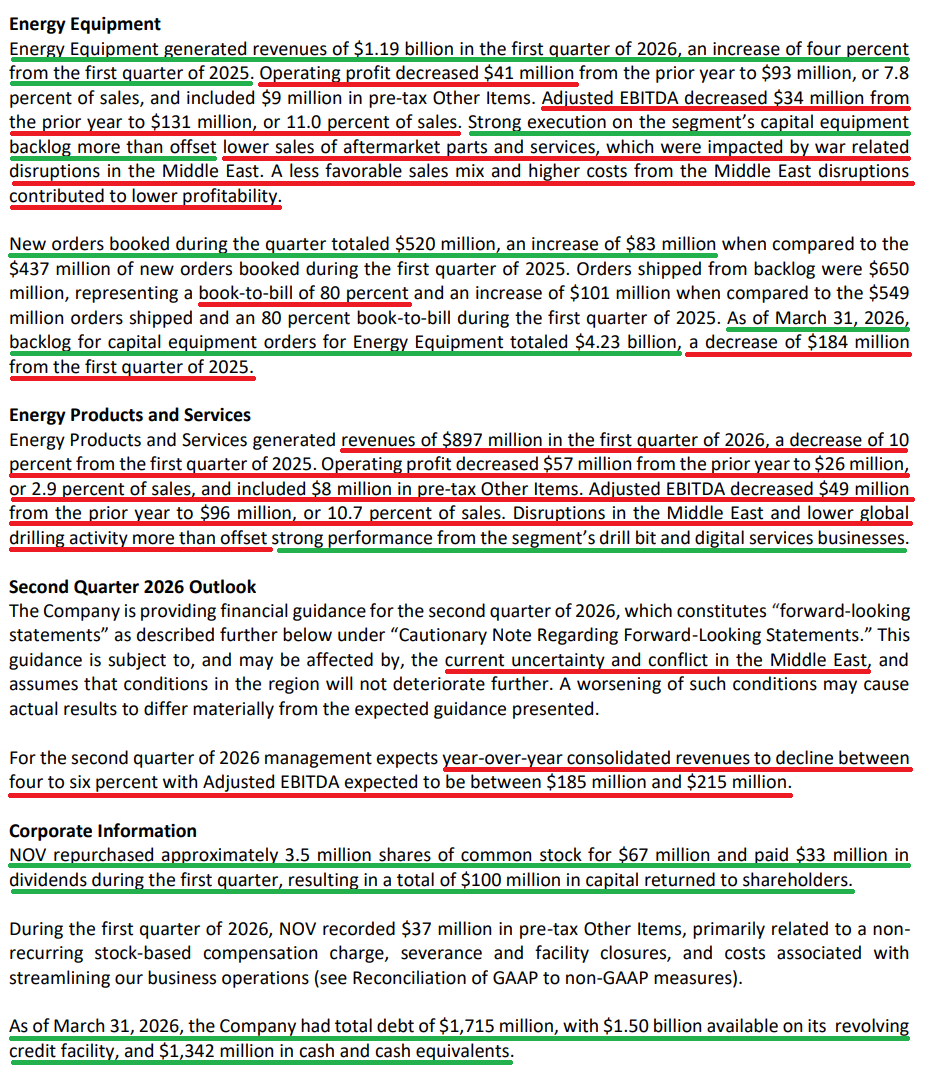

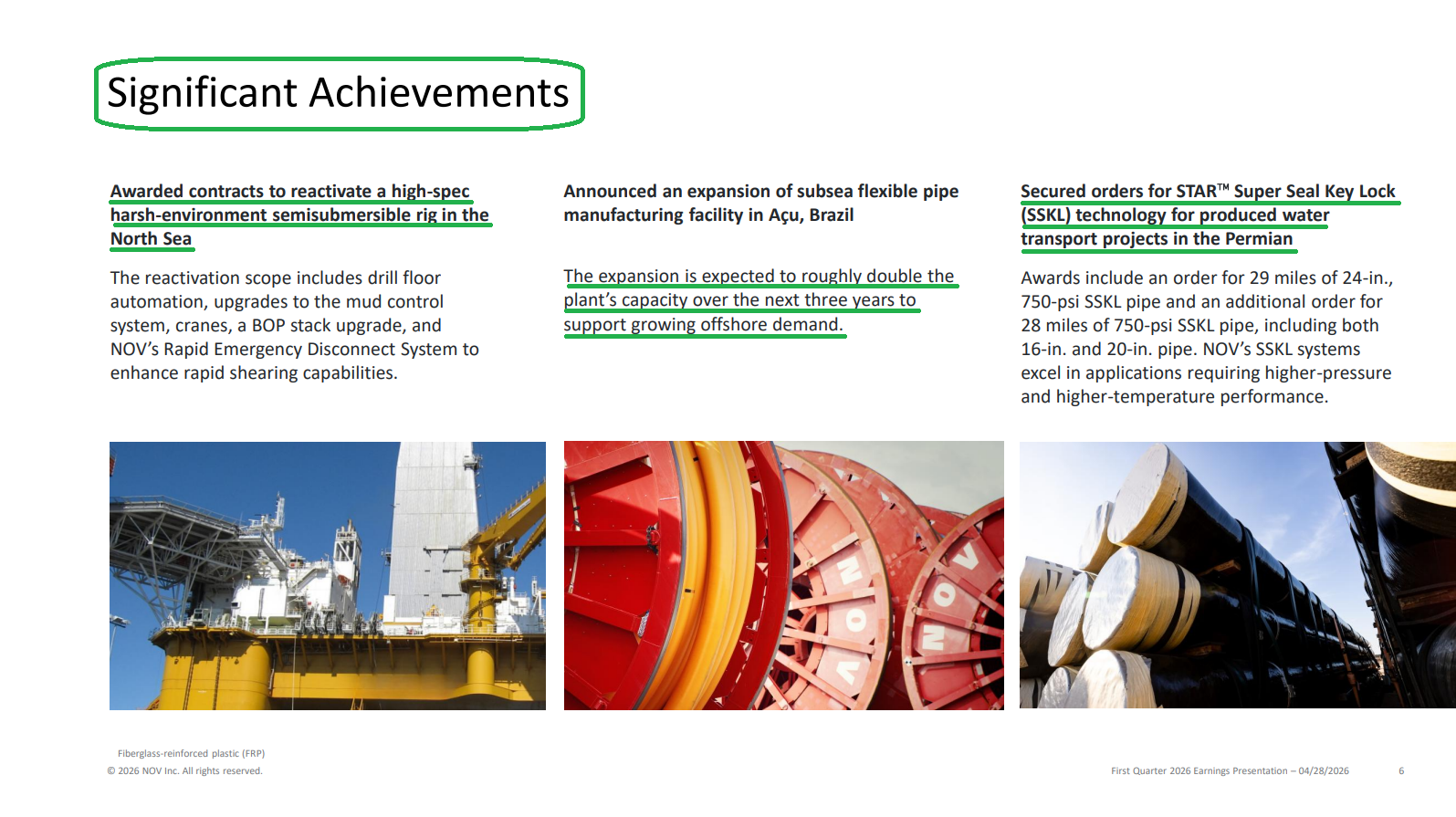

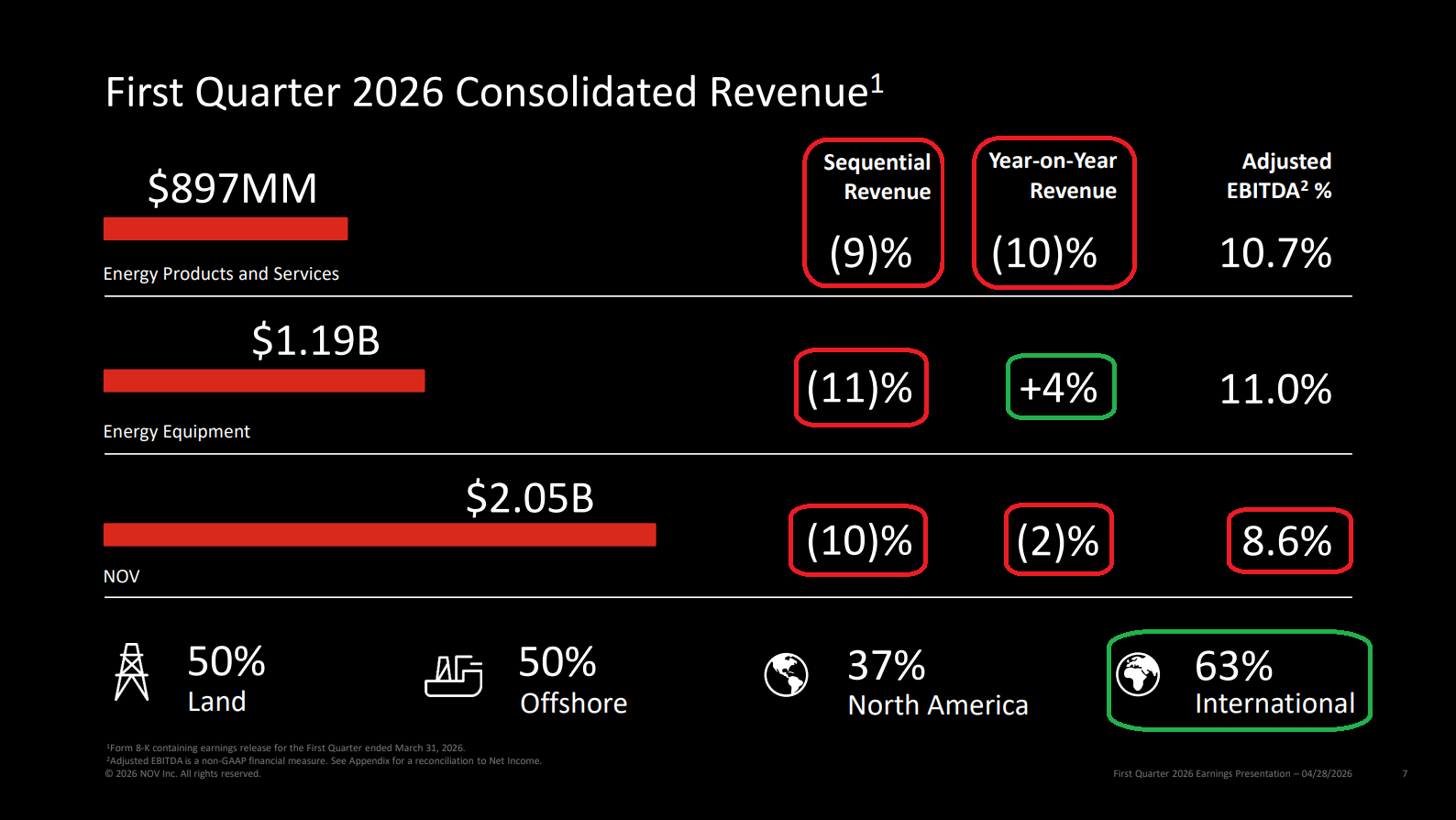

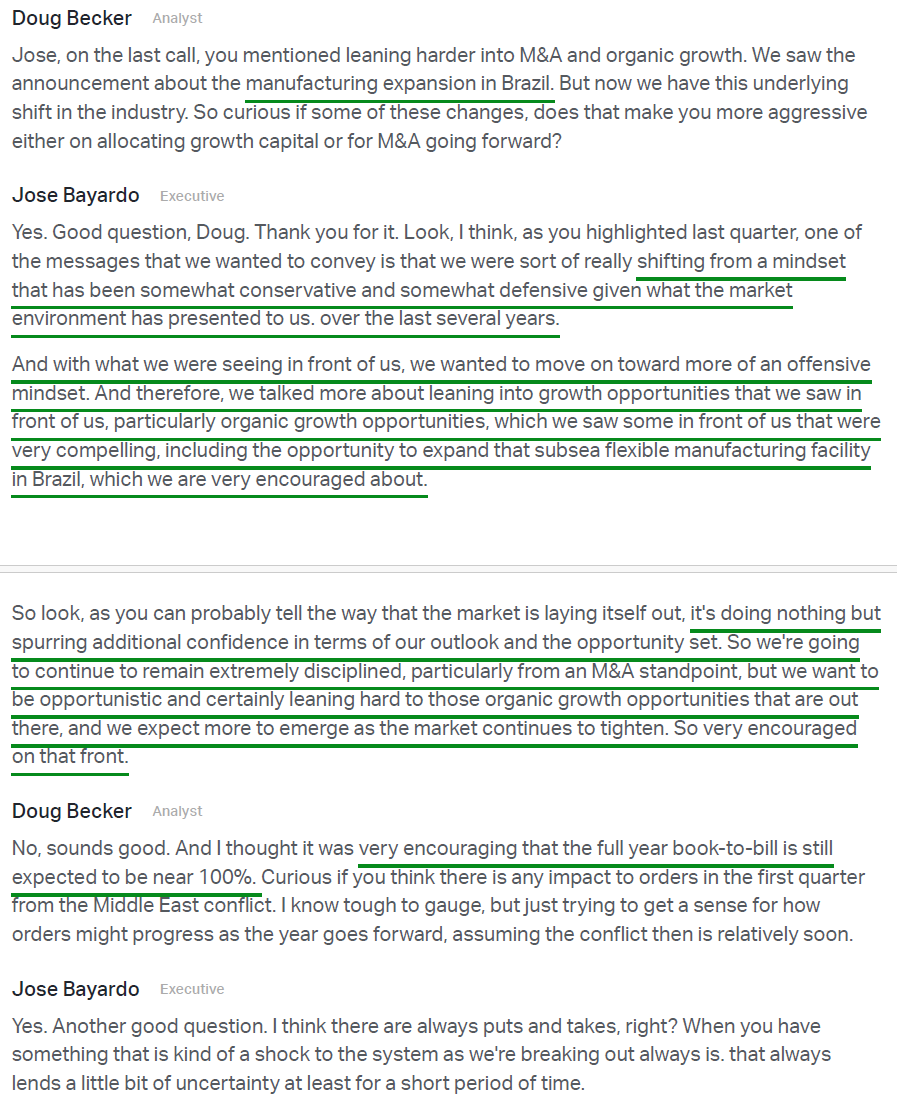

3) Energy Equipment segment revenue of $1.19B (+4% Y/Y and -11% Q/Q) marked the fourth consecutive quarter of Y/Y revenue growth, led by continued strength in offshore production-related businesses, which drove 16% growth in capital equipment sales, partially offset by a 12% decline in aftermarket sales and services. Adjusted EBITDA of $131M (-21% Y/Y) was pressured by a lower mix of high-margin aftermarket revenue and Middle East disruptions, resulting in 340 bps of Y/Y margin contraction to 11.0%. New orders totaled $520M, up 19% Y/Y and marking the strongest Q1 order intake since 2019, resulting in a book-to-bill ratio of 80%, with backlog ending at $4.23B (-$184M Y/Y). Encouragingly, management continues to expect full-year 2026 book-to-bill at or near 100%. A bright spot within the segment remains the subsea flexible pipe business, which posted record quarterly EBITDA for the third consecutive quarter, with backlog now extending into 2028 and a book-to-bill ratio exceeding 100% for four straight years. To capitalize on that strength, NOV recently approved a $200M expansion of its subsea flexible pipe facility in Brazil aimed at doubling capacity over the next three years to address a developing capacity shortfall as offshore activity accelerates.

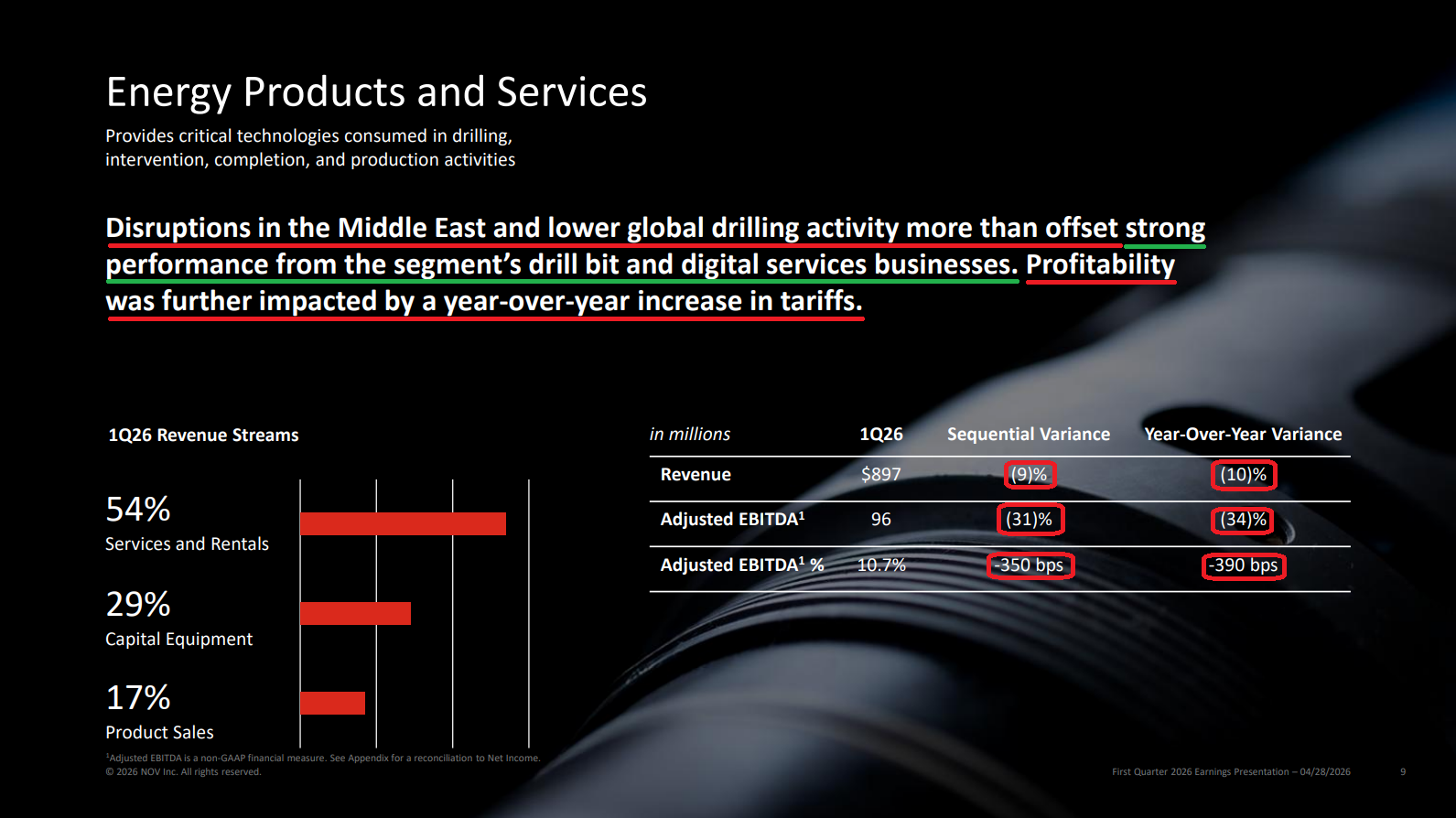

4) Energy Products and Services segment revenue of $897M (-10% Y/Y and -9% Q/Q) was negatively impacted by Middle East disruptions that delayed capital equipment deliveries, more than offsetting market share gains in the drill bit business and increasing adoption of digital services. Adjusted EBITDA of $96M (-34% Y/Y) was pressured by lower volumes, manufacturing absorption impacts, higher tariff costs, and inflationary raw material pressures, leading to 390 bps of Y/Y margin contraction to 10.7%. A bright spot across the segment was the composites business, which posted record quarterly bookings, resulting in backlog reaching its highest level in 10 quarters. Drill pipe orders also outpaced the past three years’ average quarterly bookings, with backlog at its highest level in 2.5 years.

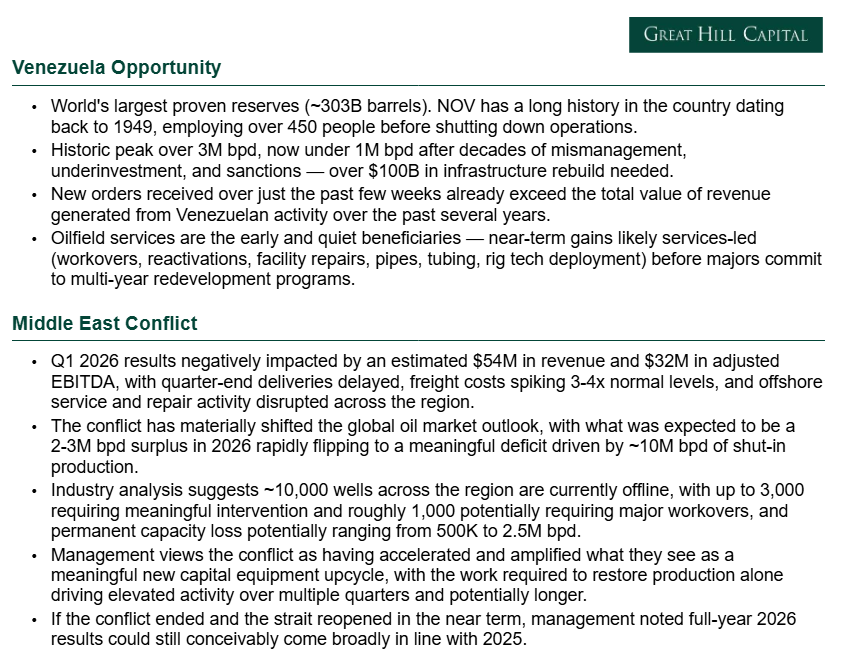

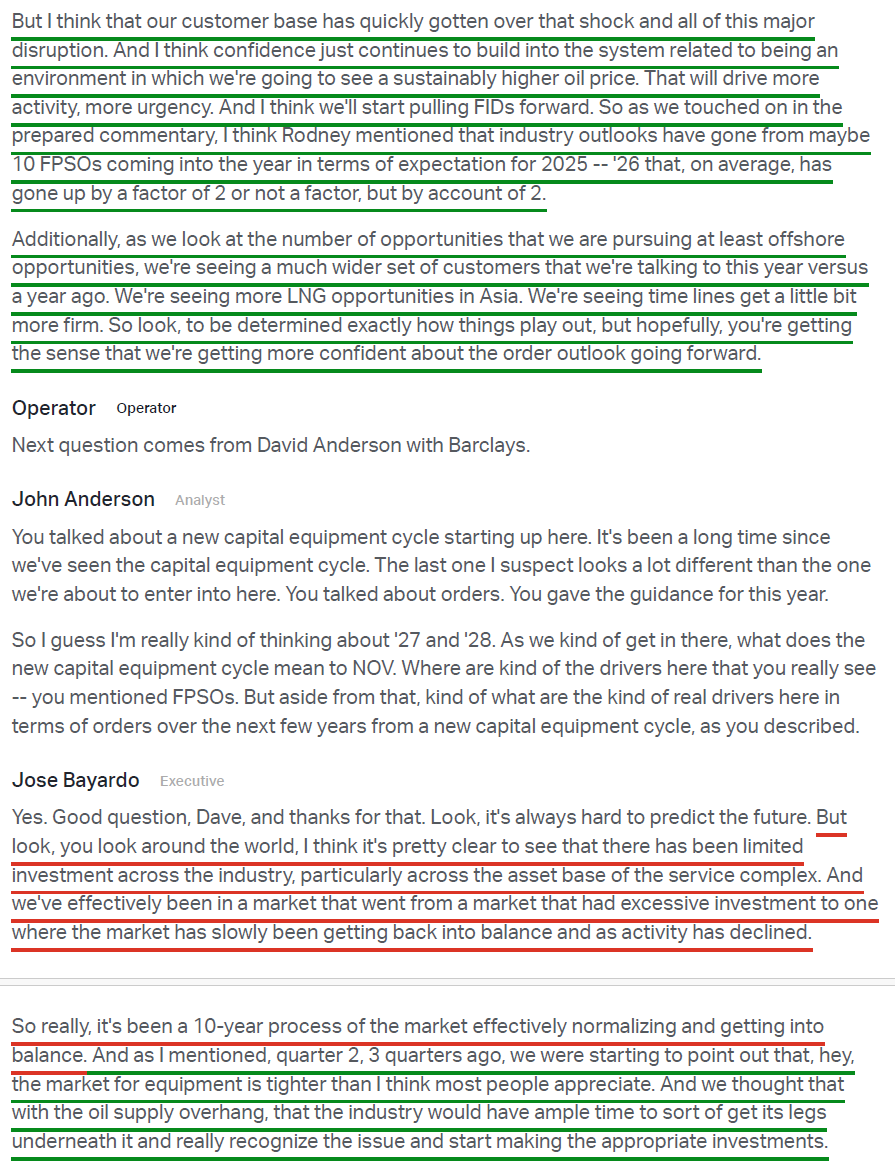

5) The conflict in the Middle East created significant operational disruptions during the quarter, with quarter-end deliveries delayed, freight costs spiking to 3-4x normal levels, and offshore service and repair activity disrupted across the region. While near-term challenges are expected to persist into Q2, conditions have improved meaningfully from the height of the conflict as the ceasefire holds. More importantly, once disruptions fully normalize, management views the situation as having accelerated and amplified what they see as a meaningful new capital equipment upcycle. The global oil market, expected to be oversupplied by 2-3M bpd coming into the year, has shifted to a meaningful deficit, with ~10M bpd of shut-in production and damaged regional infrastructure requiring drawdowns of strategic reserves worldwide. Management cited industry analysis suggesting ~10,000 wells across the region are currently offline, with up to 3,000 requiring meaningful intervention, ~1,000 potentially requiring major workovers or recompletions, and permanent capacity loss potentially ranging from 500K bpd to 2.5M bpd. The work required to restore production alone should drive elevated activity over multiple quarters, and potentially longer, with management noting the market will remain undersupplied for an extended period even after the conflict resolves.

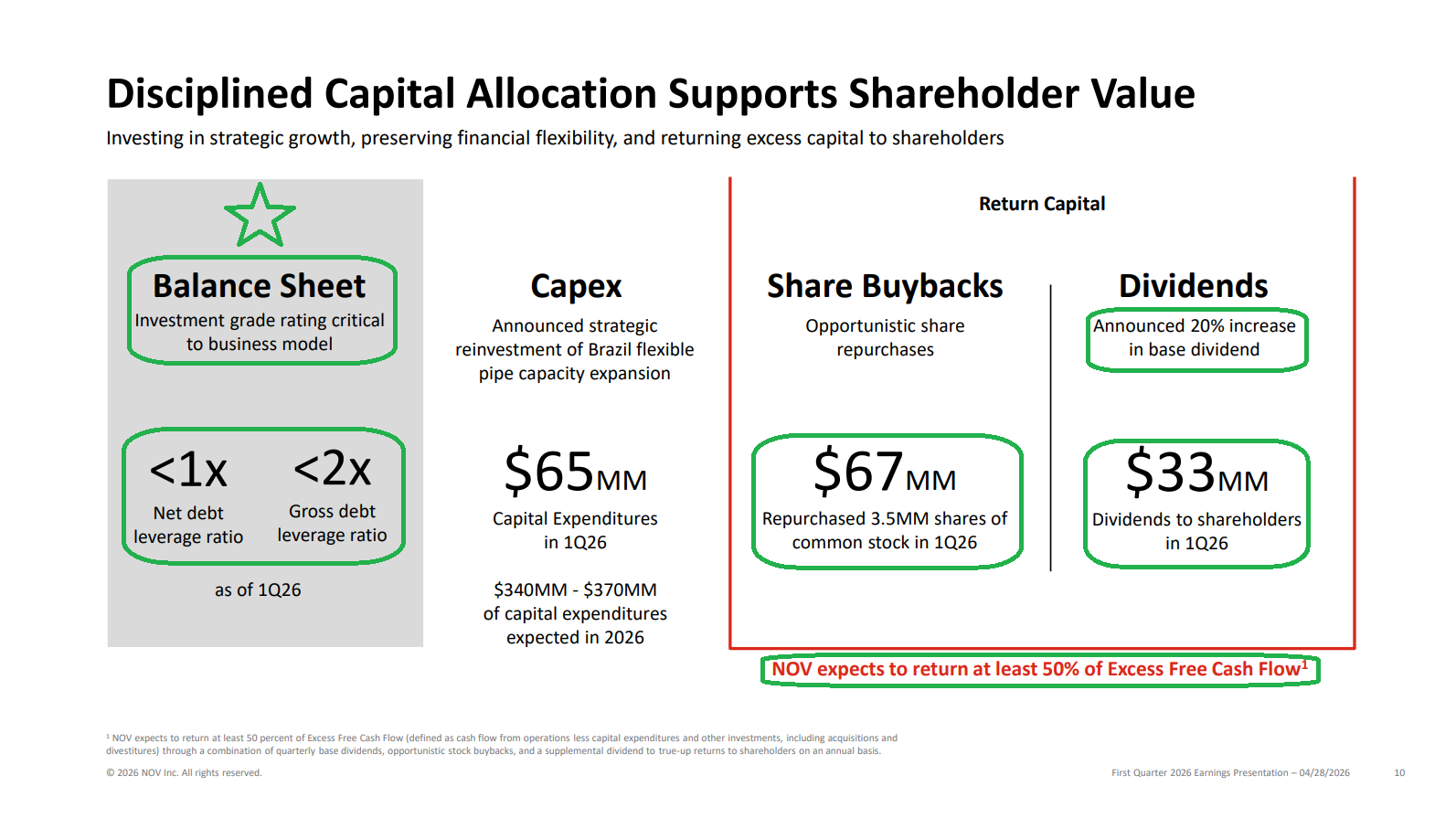

6) NOV returned $100M of capital to shareholders during the quarter through $67M in share repurchases (~3.5M shares) and $33M in dividends, reflecting the previously announced 20% increase in the quarterly base dividend. Over the past eight quarters, NOV has returned more than $900M to shareholders, with a supplemental dividend planned for Q2 to true up the ongoing commitment of returning at least 50% of excess FCF.

7) NOV continues to maintain a fortress balance sheet, with $1.34B in cash and equivalents, $1.50B available on its primary revolving credit facility (recently extended one year through 2030), and total debt of $1.72B, with the next maturity not until 2029. This implies net debt leverage of <1x and gross leverage of <2x, supporting NOV’s investment-grade credit rating.

8) Free cash flow during the quarter was an outflow of $91M (vs. +$51M in the prior year) on operating cash flow of -$26M, weighed down by Middle East-related working capital build and lower EBITDA. Despite the soft Q1 print, working capital intensity improved 400 bps Y/Y to 26.7% of revenue, with management continuing to expect full-year 2026 EBITDA-to-FCF conversion of 40% to 50% and cash generation ramping through the remainder of the year.

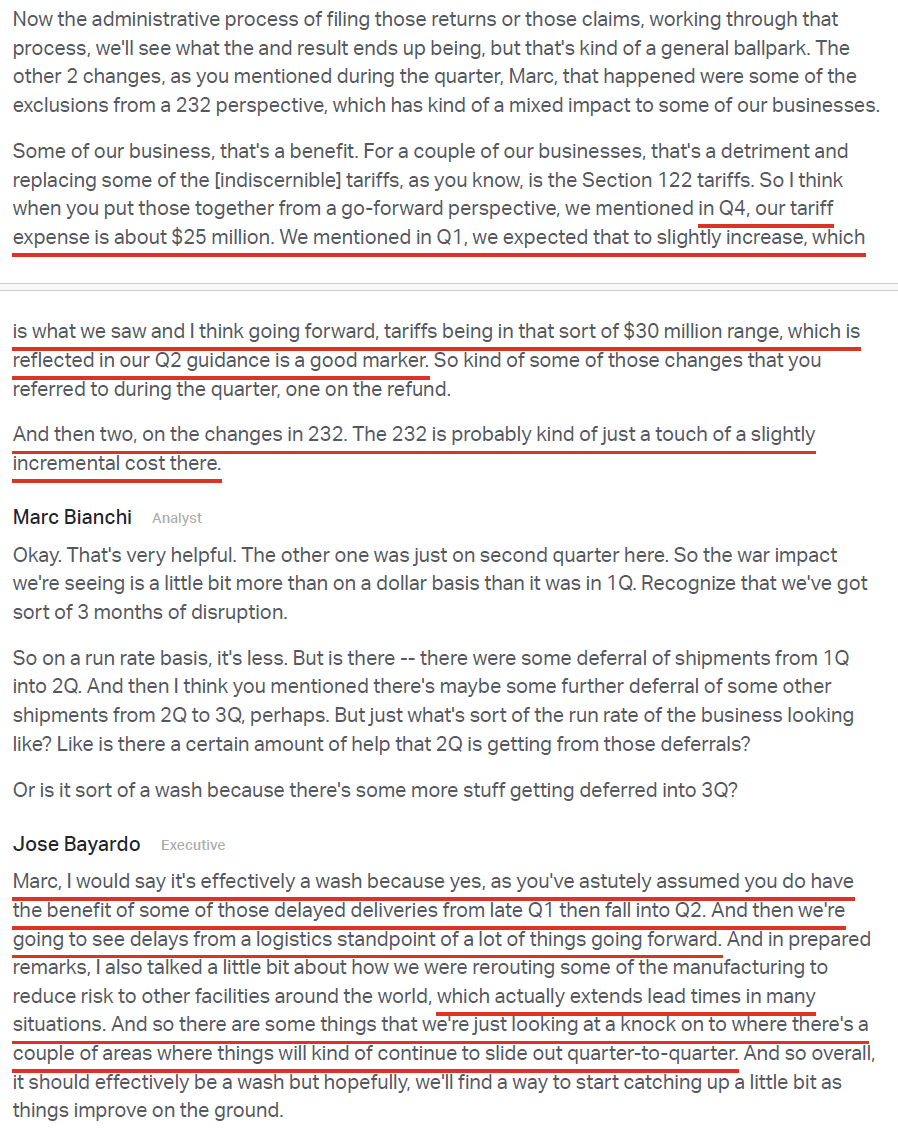

9) Tariff costs reached $30M during the quarter, with Q2 and the foreseeable future expected to remain in roughly the same range, as the Section 232 exclusion-related shift has created incremental cost pressure. On the positive side, NOV filed a claim for a refund associated with the February Supreme Court ruling on EPA tariffs, with a potential recovery of ~$40M not currently reflected in Q2 guidance.

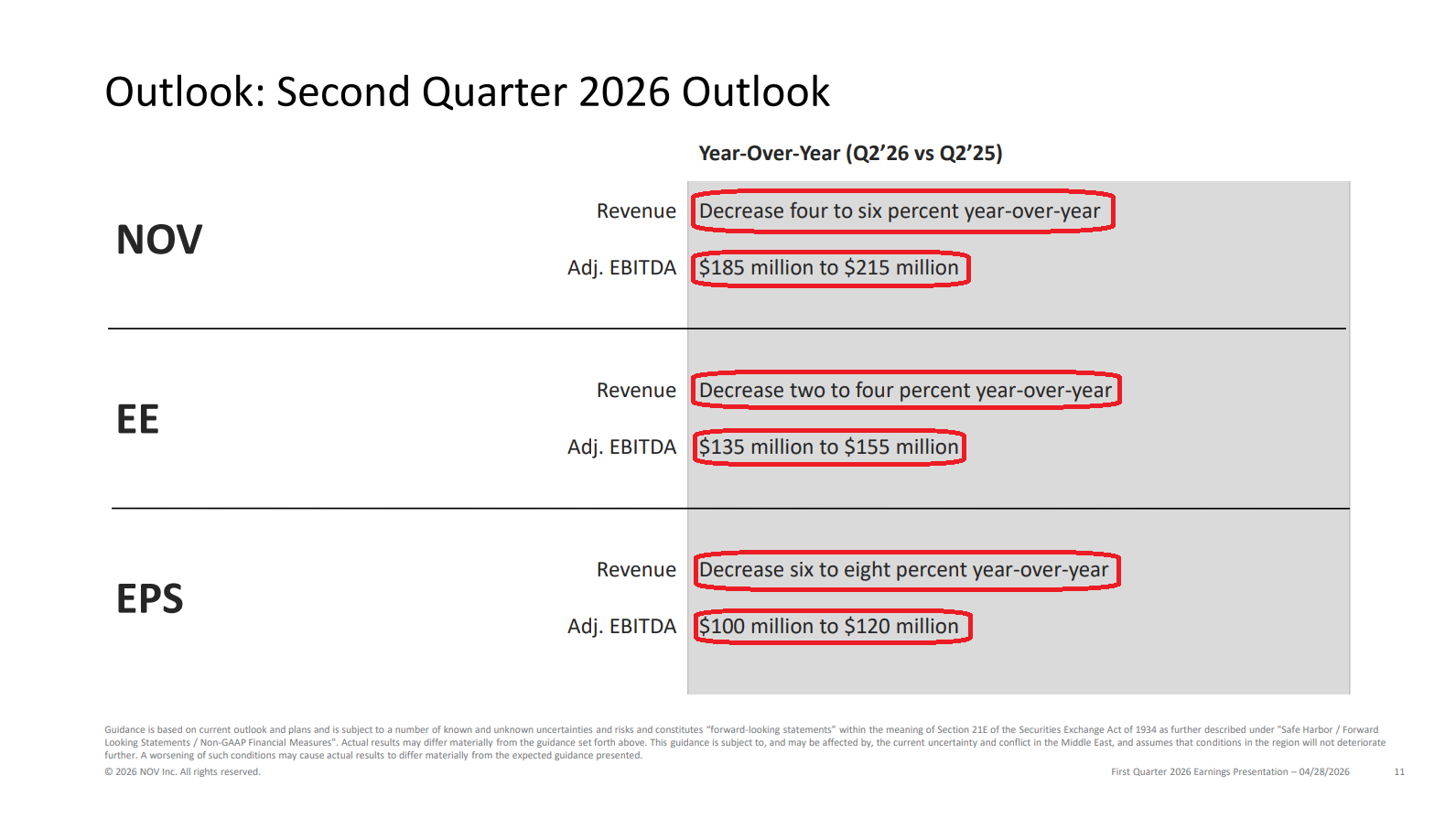

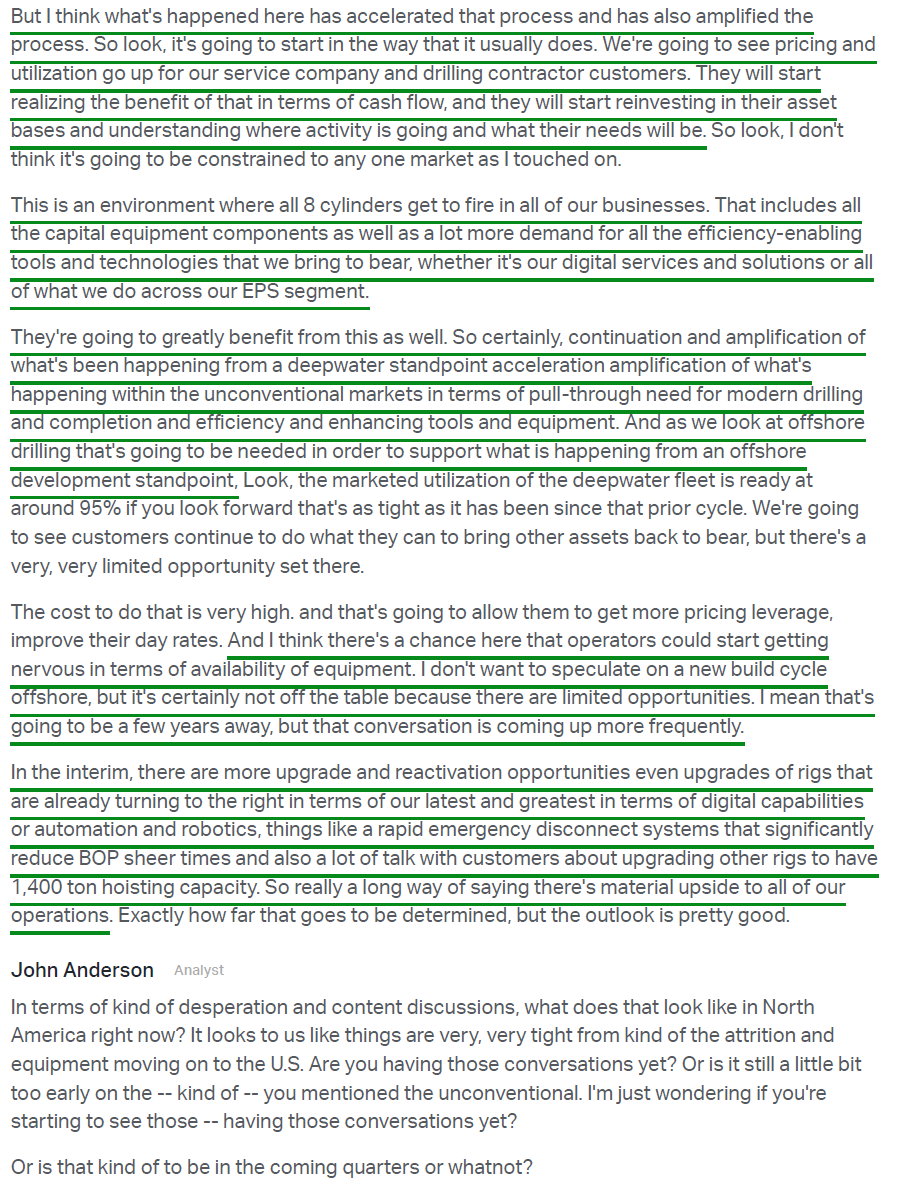

10) For Q2, management expects revenue down 4% to 6% Y/Y and adjusted EBITDA of $185M to $215M (vs. $252M in the prior year), with Energy Equipment revenue down 2% to 4% Y/Y and EBITDA of $135M to $155M, and Energy Products and Services revenue down 6% to 8% Y/Y and EBITDA of $100M to $120M. The Q2 guide assumes the ceasefire holds but the strait remains closed, with Middle East impact slightly larger than Q1 but not materially different. Management noted that if the conflict ended and the strait reopened in the near term, full-year 2026 results could still come in broadly in line with 2025. Management remains highly constructive on the medium- to long-term industry outlook, eyeing late 2026 and 2027 as the environment where “all eight cylinders of NOV’s engine can fire,” a setup that has been years in the making but is being accelerated by the current disruption.

Earnings Call Highlights

General Market

The CNN “Fear and Greed Index” remained unchanged at 68 week over week. You can learn how this indicator is calculated and how it works here: (Video Explanation)

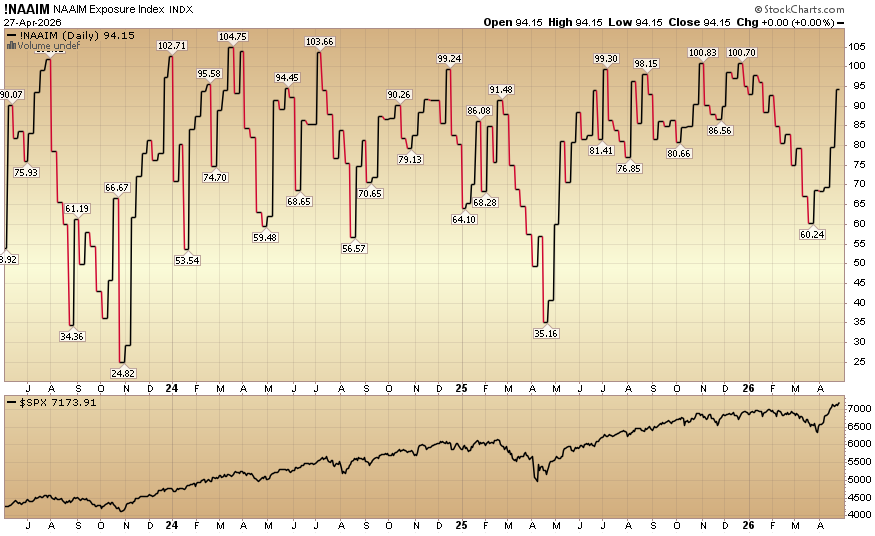

The NAAIM (National Association of Active Investment Managers Index) (Video Explanation) rose to 94.15% equity exposure this week from last week’s 79.49%.

Our podcast|videocast will be out sometime today. We have a lot of great data to cover this week. Each week, we have a segment called “Ask Me Anything (AMA)” where we answer questions sent in by our audience. If you have a question for this week’s episode, please send it in at the contact form here.

Larger accounts $5-10M+ can access bespoke service anytime here.

Not a solicitation.

*Opinion, Not Advice. See Terms