Key Market Outlook(s) and Pick(s)

On Monday, I joined Charles Payne on Fox Business to discuss markets, the economy, the consumer, QXO ($QXO), GXO ($GXO), Boeing ($BA), VF Corp ($VFC), Papa John’s ($PZZA), and more. Thanks to Charles and Nicholas Palazzo for having me on:

On Tuesday, I joined Stuart Varney and Taylor Riggs on Fox Business’ Varney & Co. to discuss markets, the economy, outlook, the Fed, Apple ($AAPL), PayPal ($PYPL), Amazon ($AMZN), Disney ($DIS), and more. Thanks to Stuart, Taylor, and Maggie Edwards for having me on:

On Tuesday, I joined Brian Brenberg and Lydia Hu on Fox Business’ The Bottom Line to discuss AI, the infrastructure buildout, energy, Comstock Resources ($CRK), and more. Thanks to Brian, Lydia, and Samantha McCormack for having me on:

On Wednesday, I joined Brian Brenberg, Taylor Riggs, Jackie DeAngelis, and Dagen McDowell Fox Business’ The Big Money Show to discuss markets, the economy, outlook, Iran, AI, Warren Buffett, and more. Thanks to Brian, Taylor, Jackie, Dagen, and Anastasia Cavounis for having me on:

On Monday, I joined Diane King Hall on the Schwab Network to discuss markets, the economy, outlook, Iran, earnings, VF Corp ($VFC), Papa John’s ($PZZA), Cooper Standard ($CPS), and more. Thanks to Diane and Kaitlyn Crist for having me on:

On Monday, I joined Ashley Mastronardi on NYSE TV to discuss markets, the economy, outlook, Iran, earnings, VF Corp ($VFC), Papa John’s ($PZZA), and more. Thanks to Ashley and Mel Montanez for having me on:

On Thursday, I joined Brian Sozzi on Yahoo! Finance to discuss markets, the economy, Iran, Intel ($INTC), and more. Thanks to Brian and Justin Oliver for having me on:

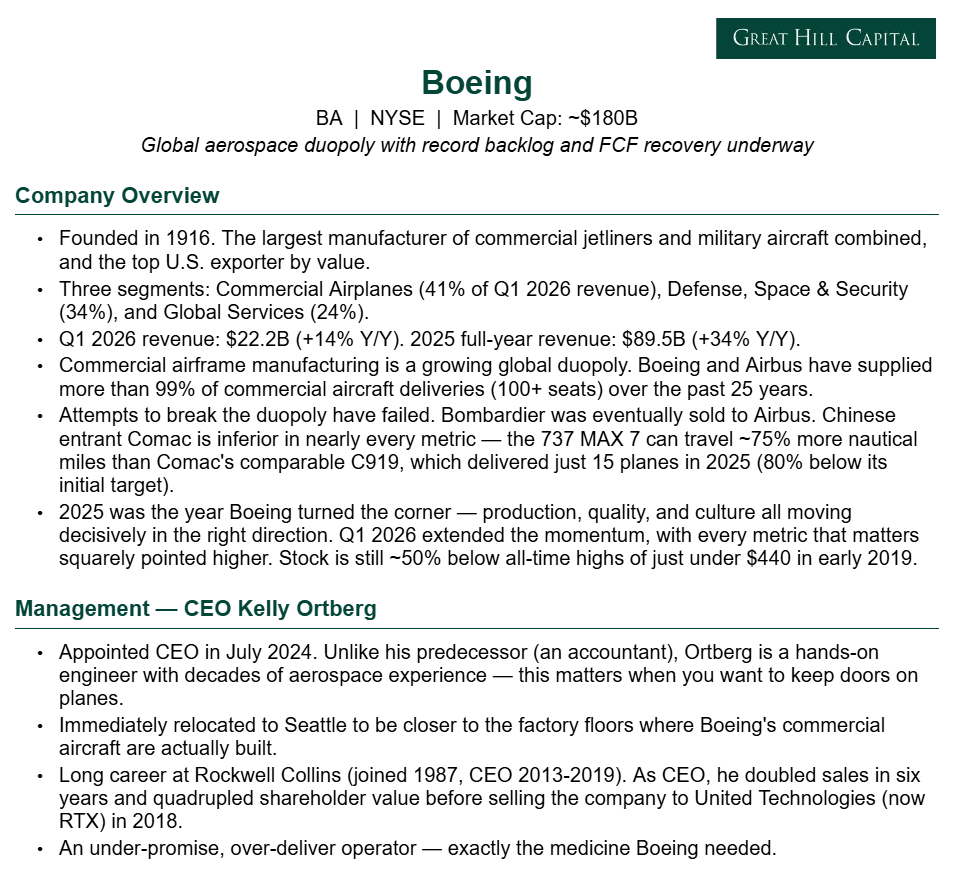

Boeing Update

For newer readers, here’s a brief overview of the key drivers behind our Boeing thesis, as one half of the global commercial aerospace duopoly where demand has never been the issue and supply, under CEO Kelly Ortberg, is finally starting to catch up:

Boeing kicked off our Q1 earnings season on the right foot, with every metric that matters in this multi-year recovery moving in the right direction.

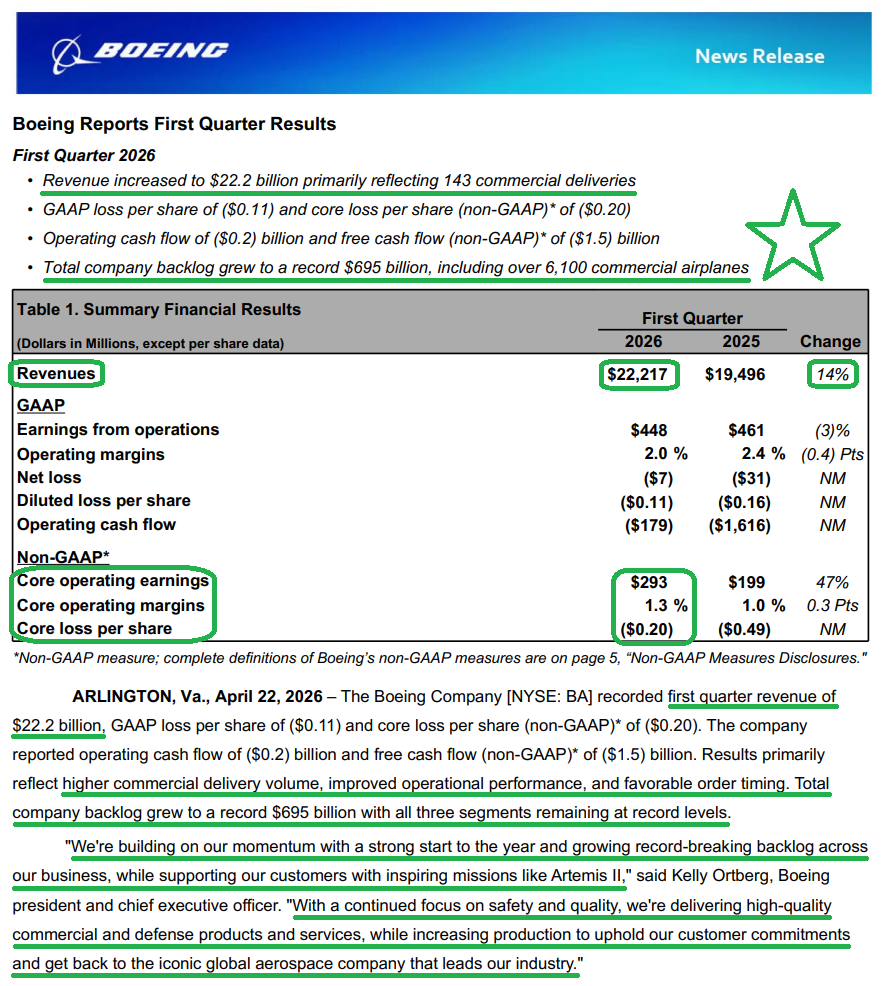

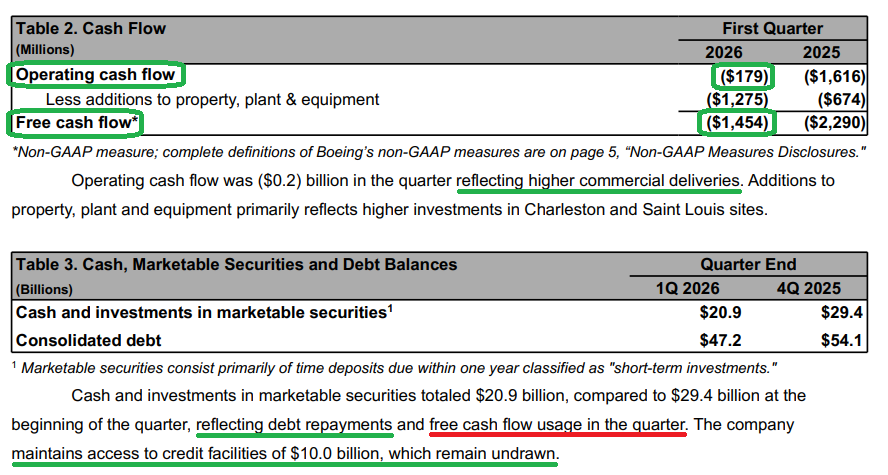

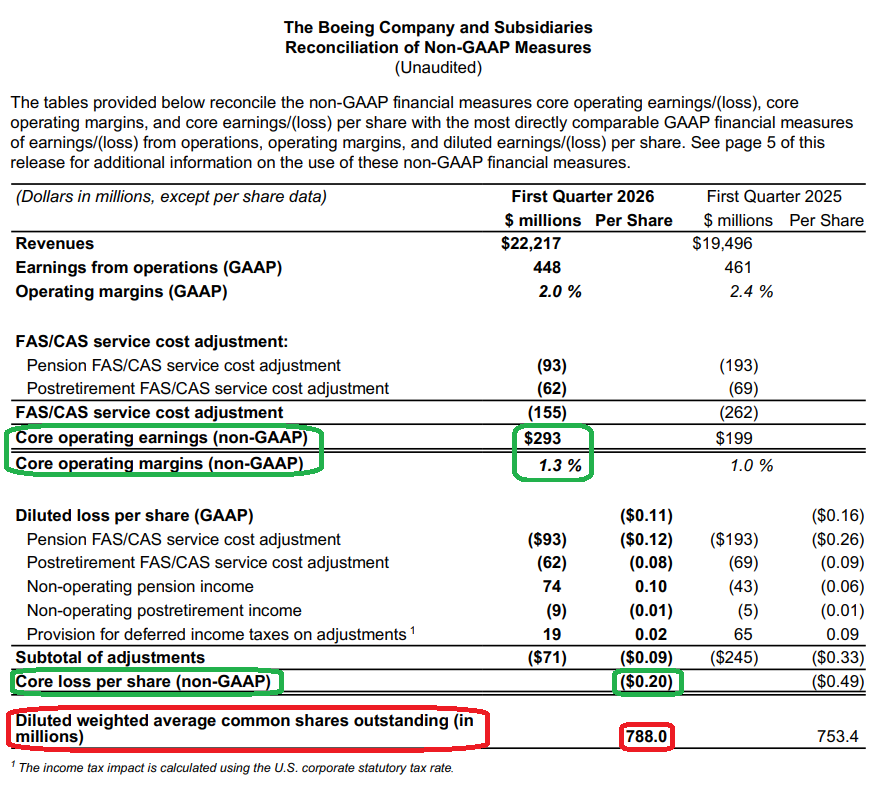

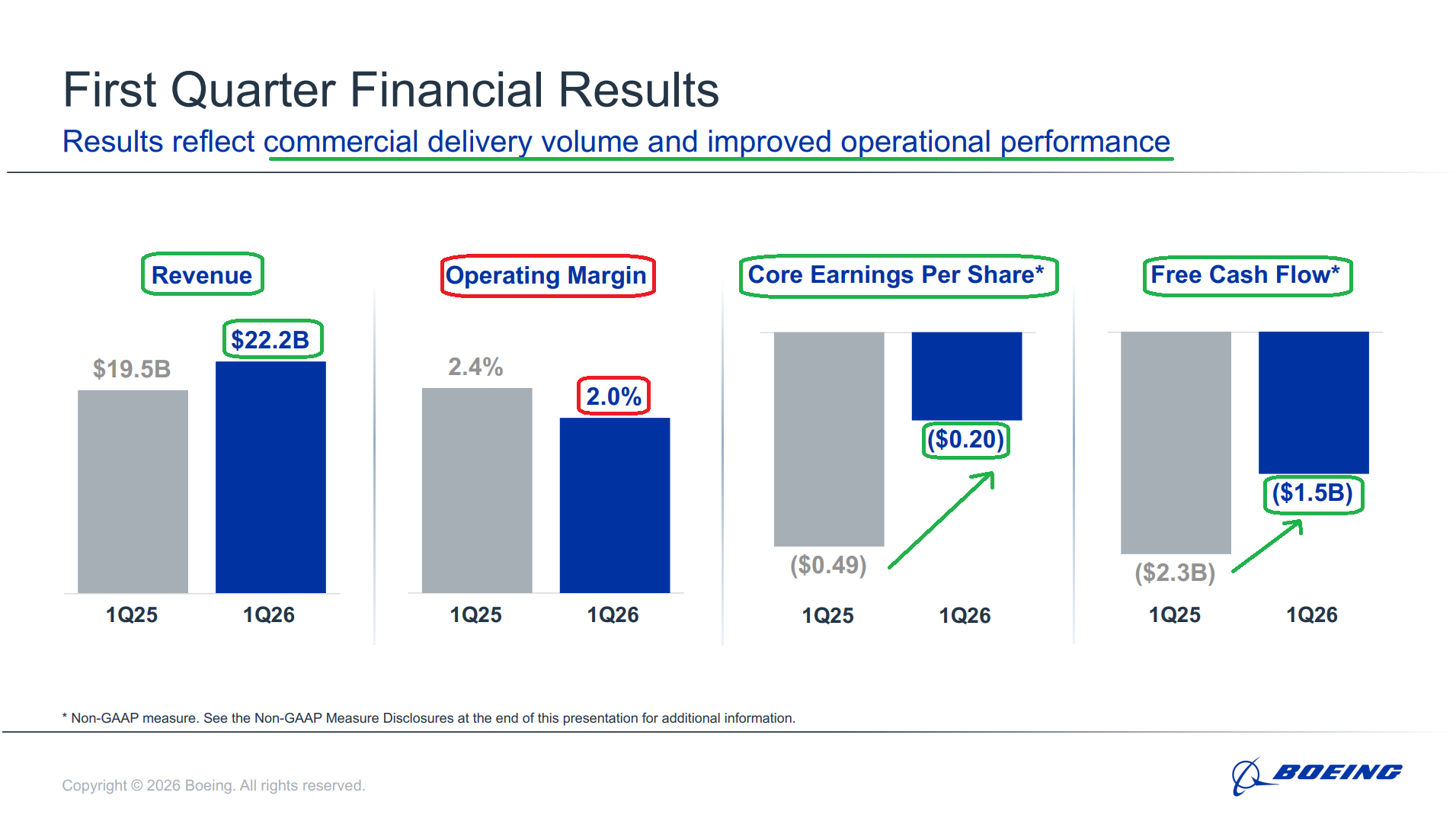

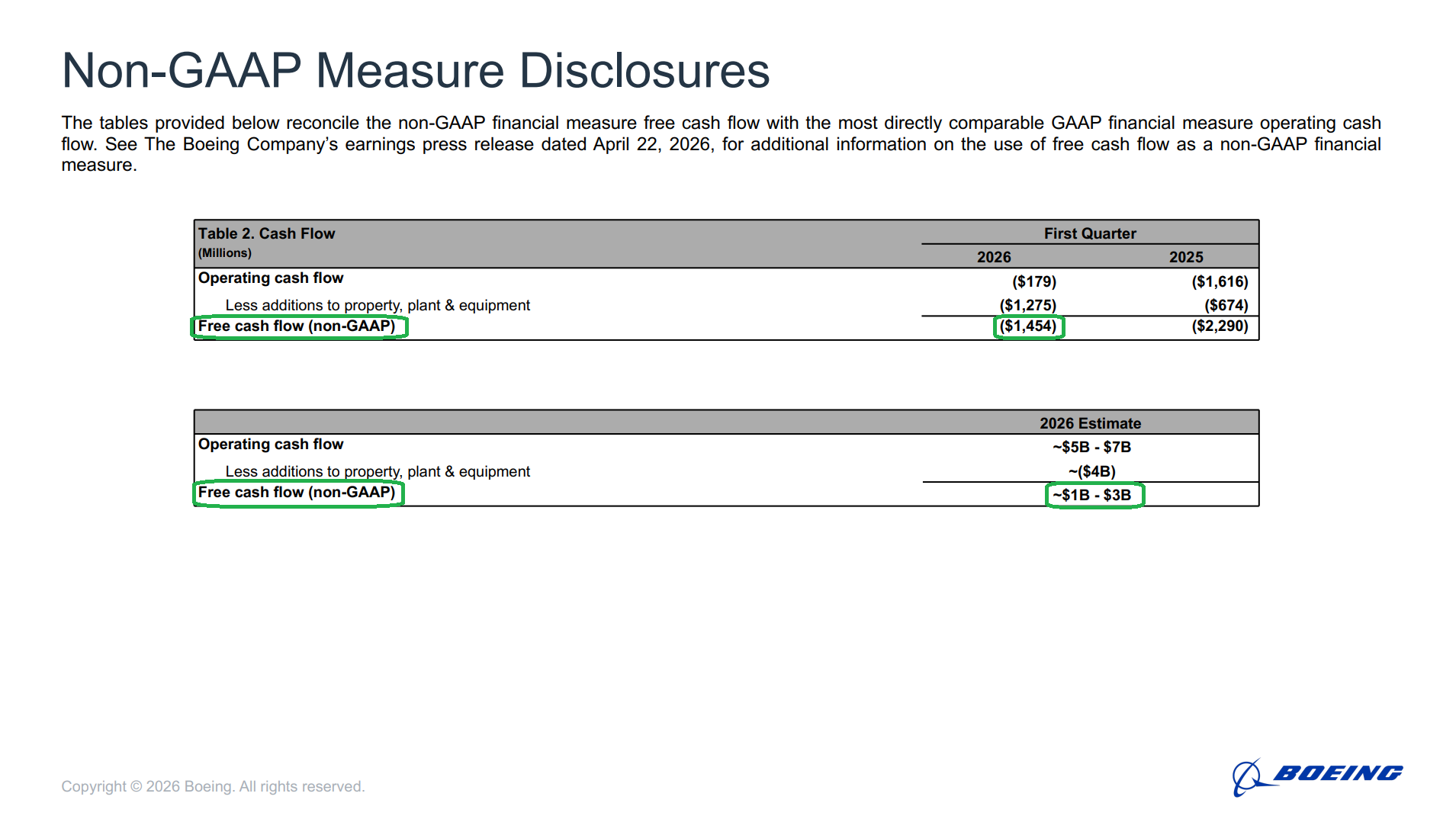

Starting with the headline numbers, revenue of $22.2B (+14% Y/Y) beat consensus by $290M, the adjusted loss of $0.20 per share came in far better than the $0.76 loss the Street was bracing for, and free cash flow burn of just $1.45B was nearly half of the $2.61B consensus had penciled in. Clean beats across the board.

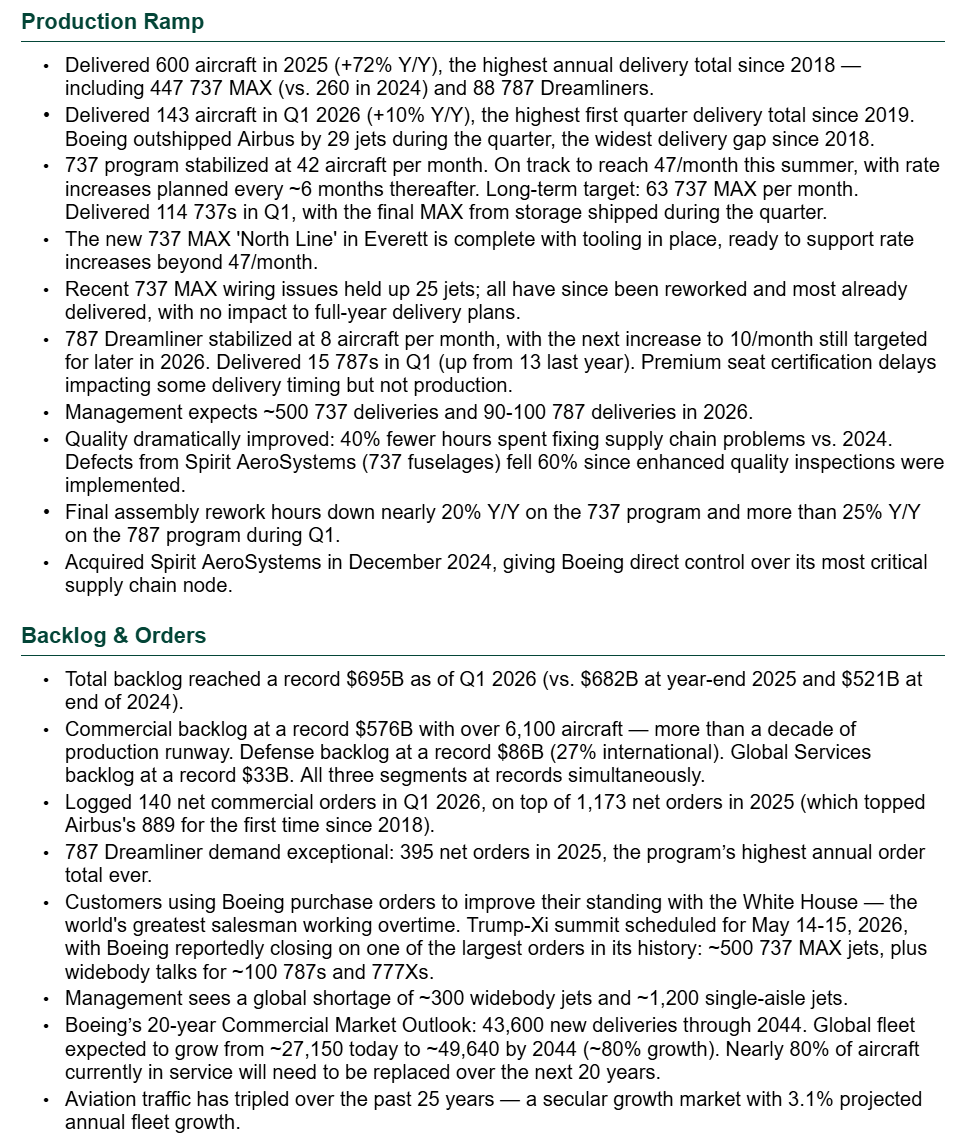

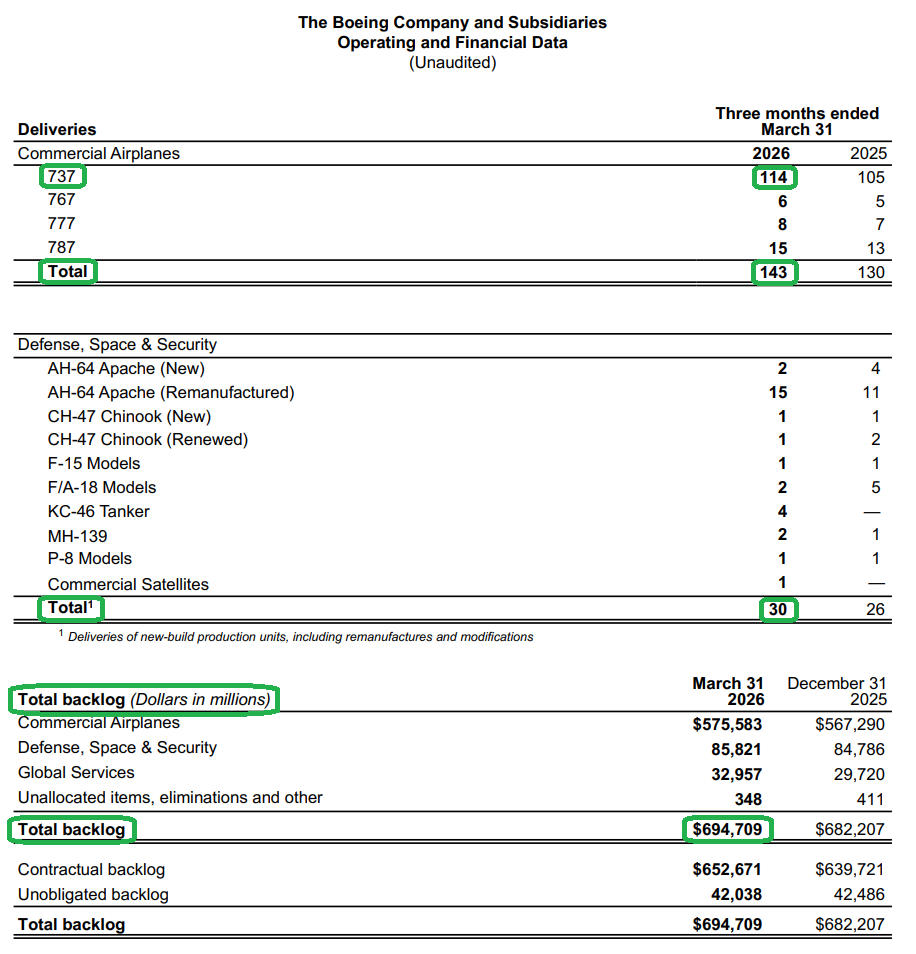

Commercial deliveries once again did the heavy lifting. Boeing handed over 143 airplanes in the quarter, the most in any first quarter since 2019, and outshipped European rival Airbus by 29 jets. That’s the widest delivery gap over Airbus going back to 2018, a stat that would have sounded like fiction twelve months ago, when being constructive on Boeing got you looked at like you had three heads. Now that the stock has climbed nearly 70% since the Liberation Day lows, investors have suddenly rediscovered the global aerospace leader and are excited again. Welcome aboard, albeit at prices where we’re already well on our way to a double.

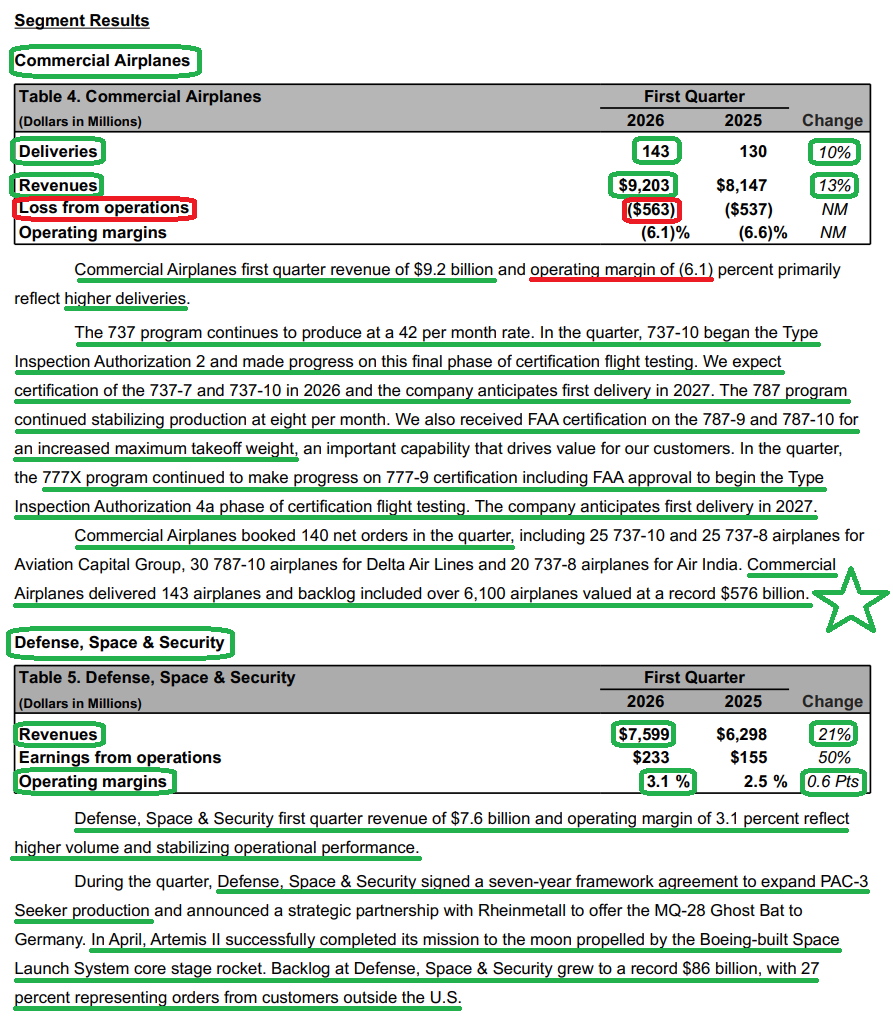

One of the big reasons we got comfortable making the original investment, besides Boeing being a national champion and global duopoly, was the long and forgiving runway of a half-trillion-dollar backlog. That backlog continues to set new records, reaching $695B with over 6,100 commercial airplanes, more than a decade of production runway at the current pace. Boeing’s troubles never stemmed from a demand problem. Demand has consistently outstripped supply, with airlines clamoring for every plane they can get their hands on. All Boeing had to do was safely build them, something they are finally starting to do.

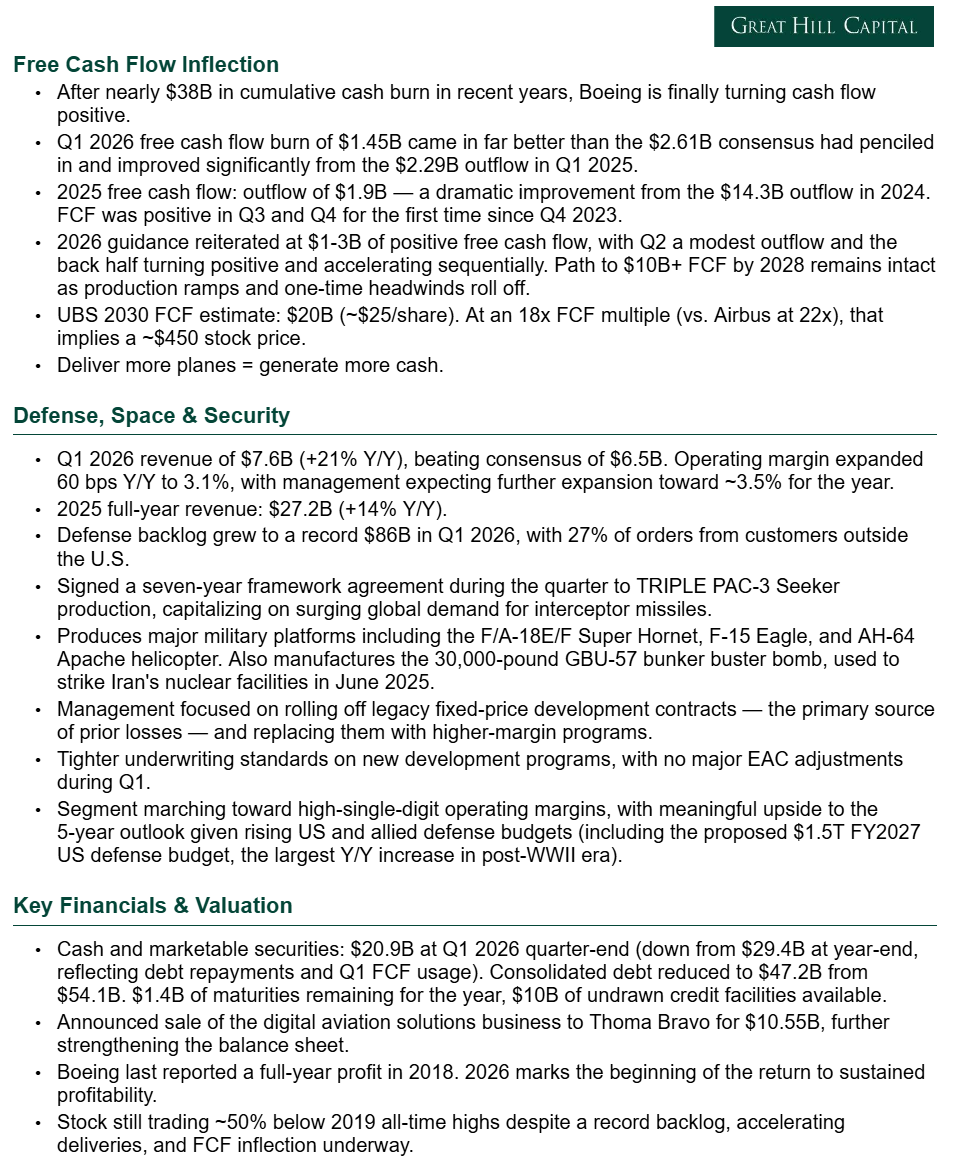

Which brings us to the heart of the thesis: free cash flow. Deliver more planes, generate more cash. Six words that capture the entire turnaround.

Q1 showed continued progress on this front, with the $1.45B burn (normal seasonality) coming in far better than feared and management reiterating the $1-3B positive FCF target for the full year, the first positive year since 2023. And while it’s great to see FCF finally flip positive, the recovery is still in the very early innings. As production ramps and one-time headwinds roll off, the long-awaited $10B annual figure should have the green light by 2028, a figure that increasingly looks like a pit stop rather than the final destination.

Beyond the numbers, the setup for the back half looks as clean and catalyst-rich as anything we’ve seen in years. We’re finally closing in on the long-awaited Trump-Xi summit (set for May 14-15), the key driver behind Boeing reportedly closing on one of the largest orders in its history: ~500 737 MAX jets, along with discussions for another ~100 widebody aircraft, including 787s and 777Xs. As we’ve said before, a Boeing order has increasingly become the price of admission in US trade negotiations. With the world’s greatest salesman setting up shop in Beijing in a few weeks, we’d be surprised if he came home empty-handed.

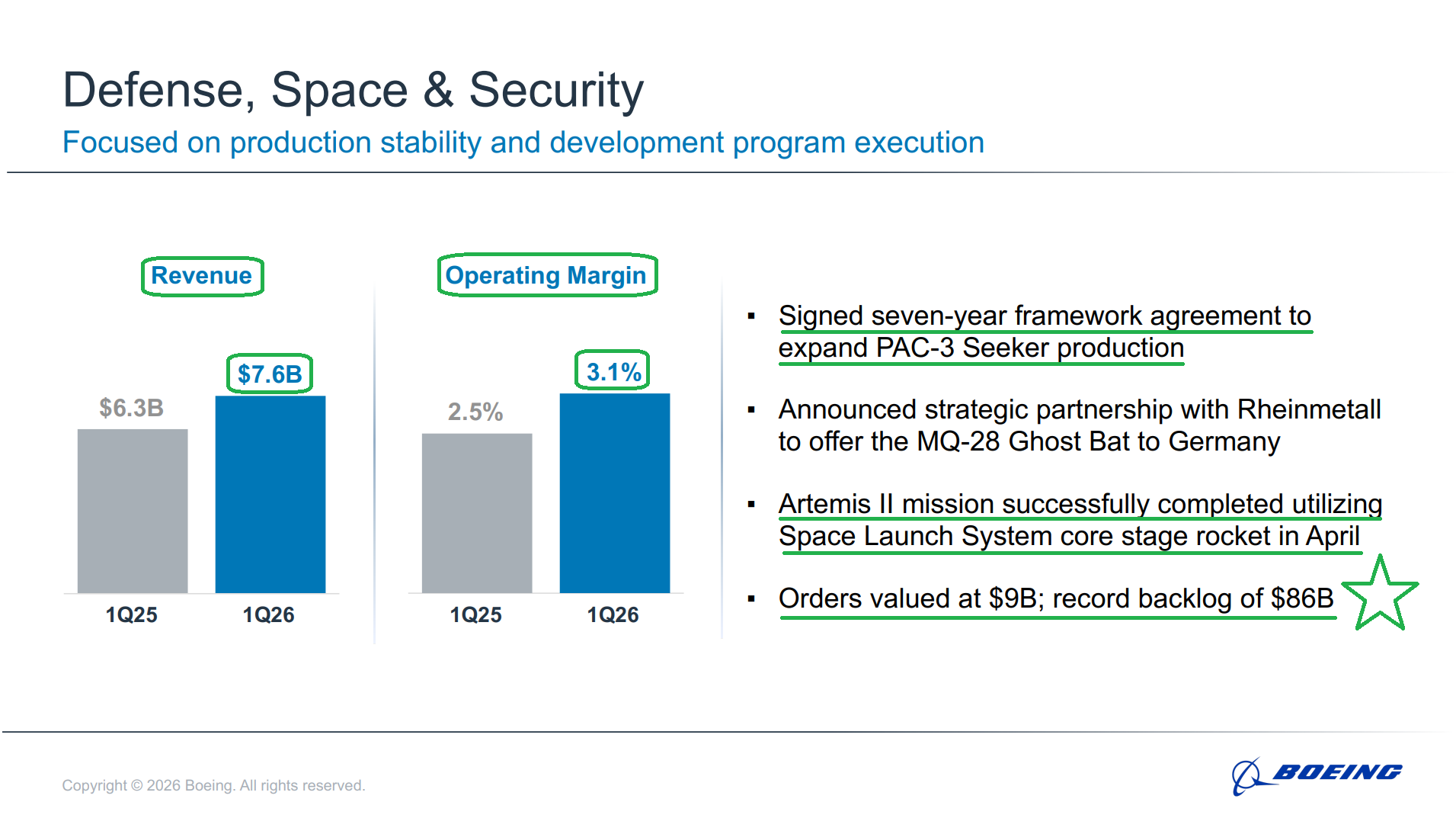

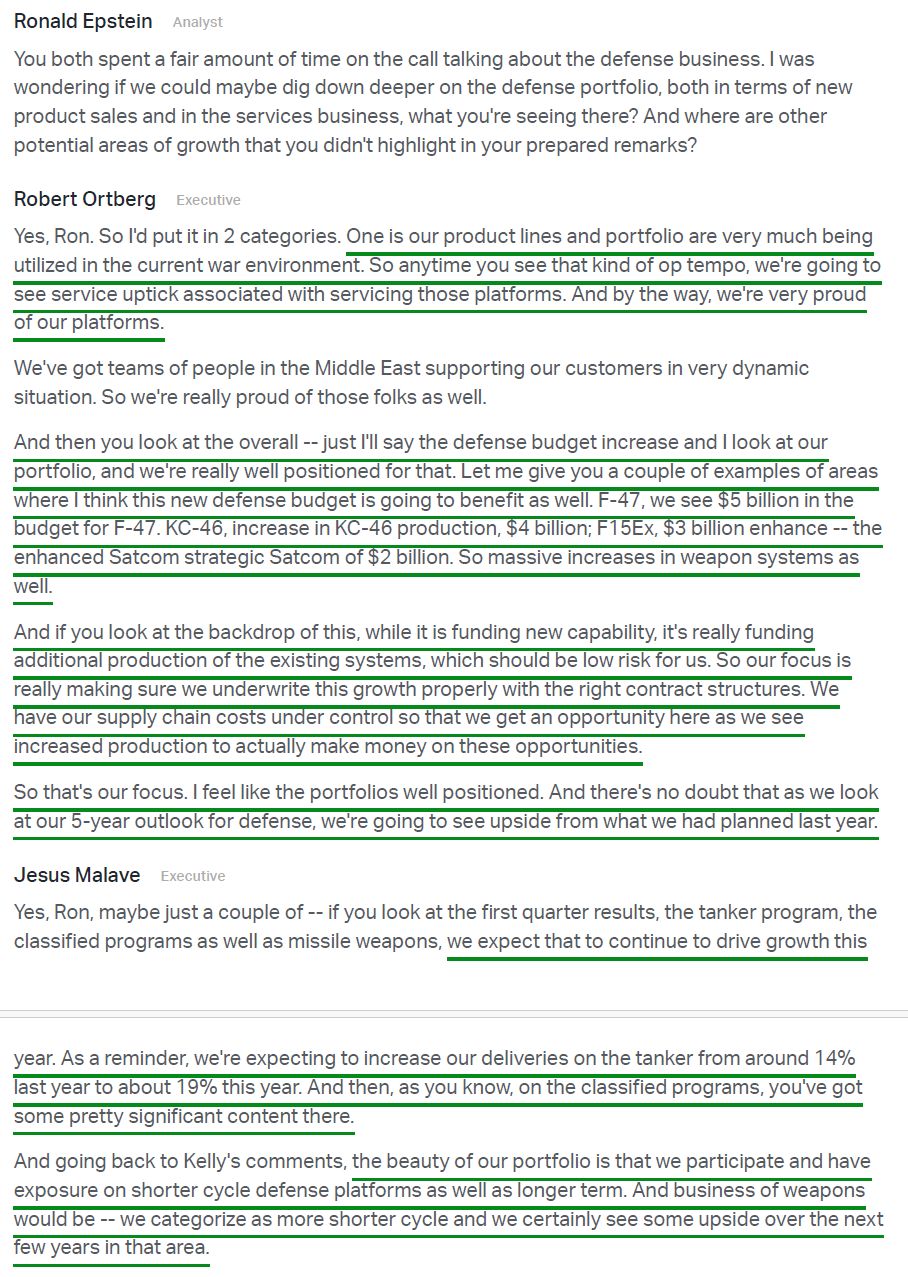

On top of that, Boeing is benefiting from tailwinds across its booming defense business, with revenue climbing 21% in the quarter to $7.6B and a newly signed seven-year framework agreement to TRIPLE PAC-3 Seeker production. With a proposed $1.5T FY2027 defense budget (the largest year-over-year increase in defense spending in the post-WWII era), no let-up looks to be in sight.

On top of that, Boeing is benefiting from tailwinds across its booming defense business, with revenue climbing 21% in the quarter to $7.6B and a newly signed seven-year framework agreement to TRIPLE PAC-3 Seeker production. With a proposed $1.5T FY2027 defense budget (the largest year-over-year increase in defense spending in the post-WWII era), no let-up looks to be in sight.

All of which is to say, this quarter marked another meaningful step forward for the global aerospace leader, and investors are finally starting to take notice. The national champion and proxy for US manufacturing that you couldn’t give away in the $130s last year is now doing exactly what we expected: delivering more planes, generating more cash, and reminding everyone why duopolies with decade-long backlogs tend to work out just fine for investors who can stomach a little short-term noise.

There’s still plenty of work to be done, but with Kelly Ortberg in the pilot seat and the factory floor (safely) humming again, our confidence in the turnaround has never been higher. From here, it’s all about execution, and there’s nobody we’d rather have in charge of it than Ortberg.

Clear skies ahead.

Q1 Earnings Breakdown

10 Key Points

1) Boeing posted Q1 revenue of $22.2B (+13.8% Y/Y), beating consensus of $21.9B by $290M, driven by solid growth across all three segments. Adjusted loss per share came in at $0.20, far better than the $0.76 loss analysts had forecast.

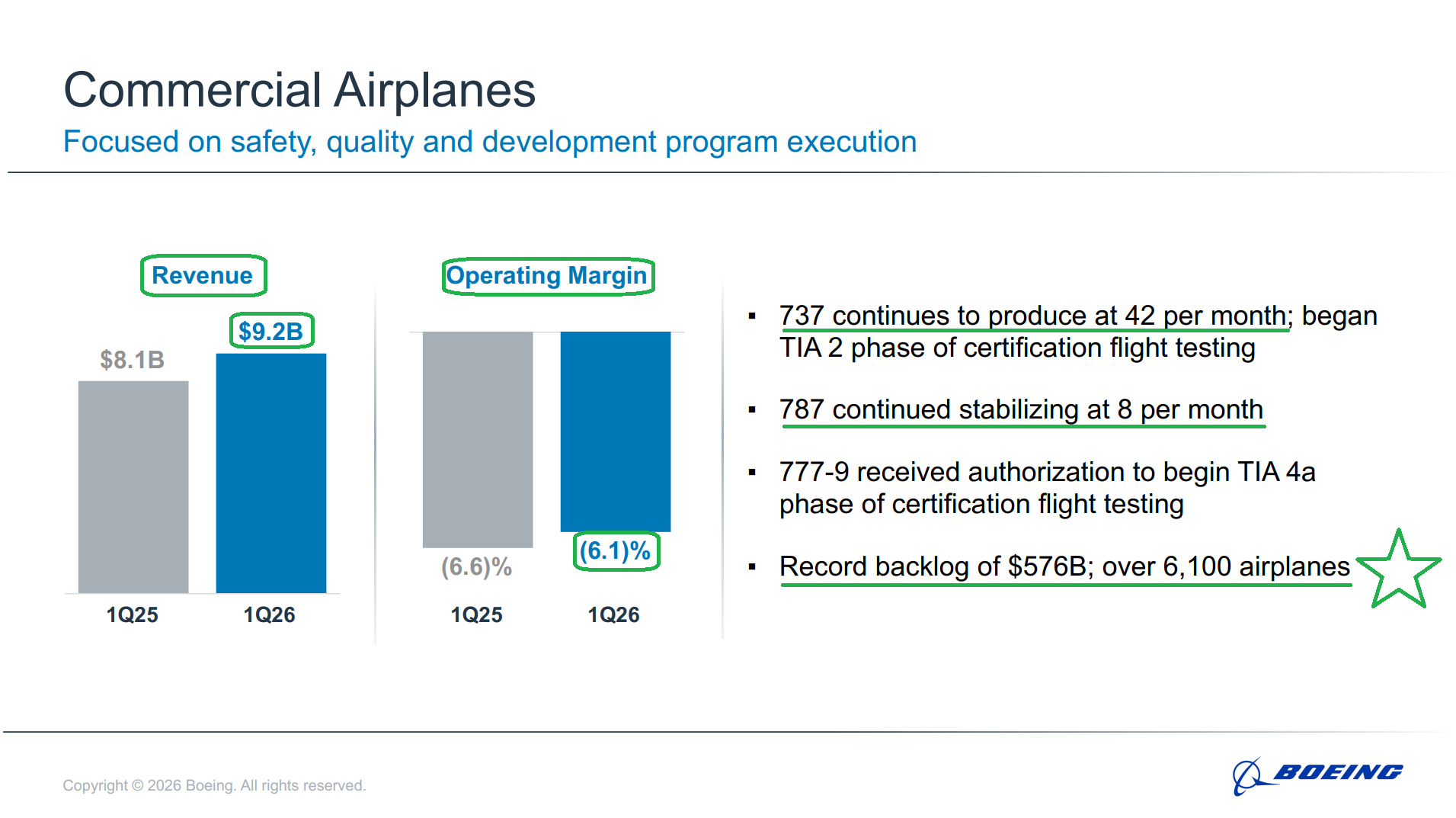

2) The Commercial Airplanes segment posted revenue of $9.2B (+13% Y/Y) during the quarter, driven by 143 deliveries, up 10% Y/Y and the highest first quarter delivery total since 2019. Notably, Boeing outshipped European rival Airbus by 29 jets during the quarter, the widest delivery gap since 2018. Segment operating margin improved modestly to (6.1%) from (6.6%) last year, with management expecting sequential improvement throughout the year and positive operating margins by mid-2027. Commercial backlog reached a record ~$576B, including over 6,100 airplanes, with 140 net orders booked during the quarter.

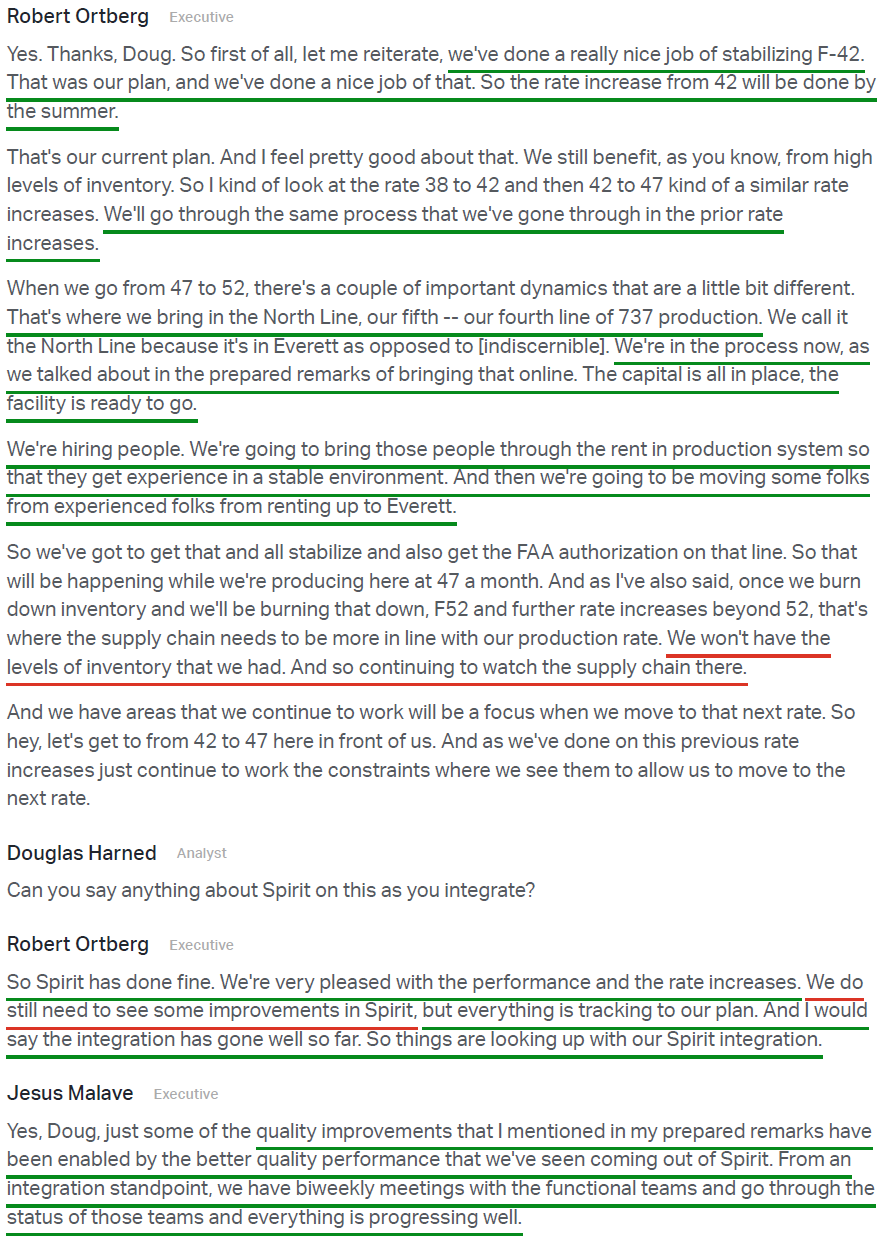

3) The 737 program stabilized at 42 aircraft per month during the quarter, delivering the final 737 MAX out of storage while continuing to drive quality improvements, with final assembly rework hours down nearly 20% Y/Y. Boeing delivered 114 737s in Q1 and remains on track for the full-year target of ~500 deliveries. Management also reiterated its plan to increase production to 47 per month this summer, noting that the recent wiring issue (which held up 25 jets, most of which have since been reworked and delivered) will not affect full-year delivery plans. Both internal and external supply chains are well positioned for the next step up, with the new Everett North Line now prepared to support future rate increases beyond 47 per month.

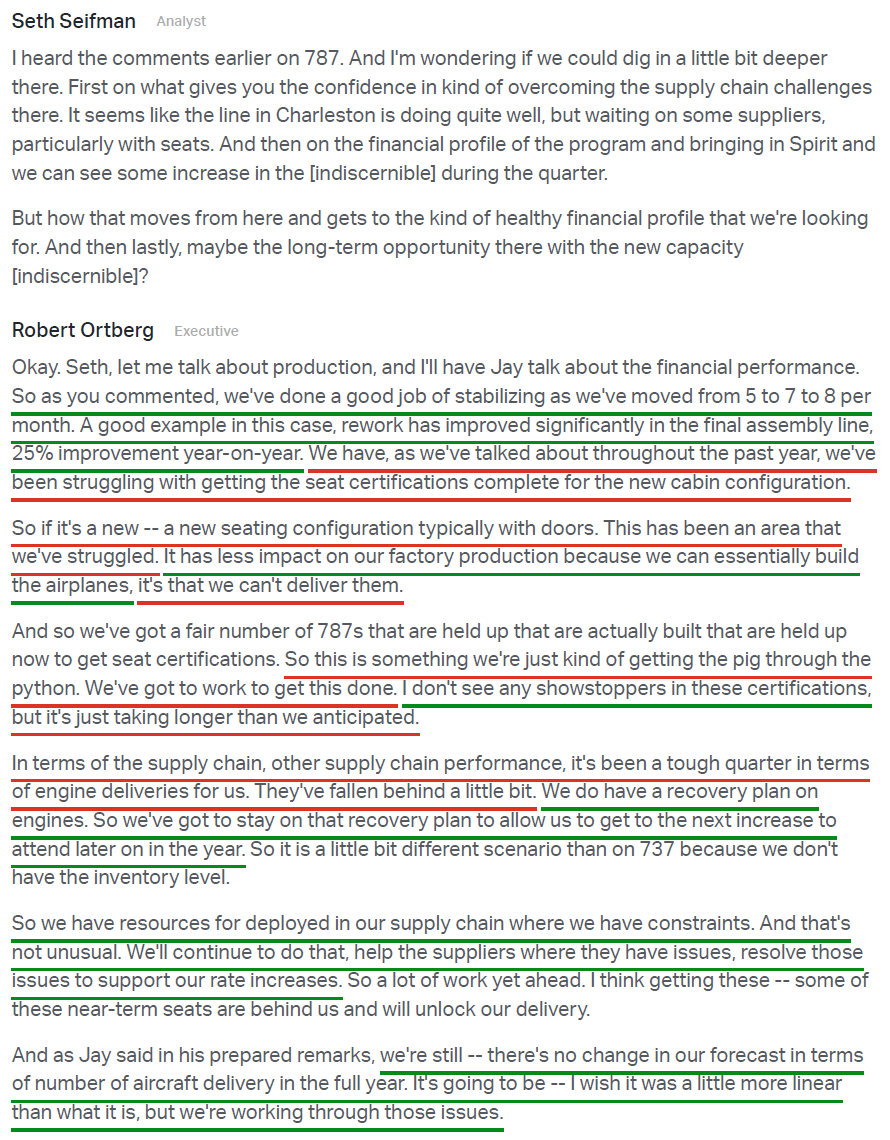

4) The 787 program stabilized at 8 aircraft per month during the quarter, with rework hours down more than 25% Y/Y. Boeing delivered 15 787s in Q1, in line with guidance and up from 13 last year, and continues to target 90-100 deliveries for the full year. The program is working through some premium seat certification delays that have impacted delivery timing, though management emphasized the impact is contained to deliveries rather than production, as the airplanes can still be built but not yet handed over to customers. The next rate increase to 10 per month remains on track for later this year.

5) The Defense, Space & Security segment posted revenue of $7.6B (+21% Y/Y), handily beating consensus estimates of $6.5B. Operating margin expanded 60 bps Y/Y to 3.1%, driven by higher volume on KC-46 Tanker, missiles and weapons, and classified programs, with management expecting further expansion toward ~3.5% throughout the year. Boeing booked $9B of orders during the quarter, growing the backlog to a record ~$86B with 27% coming from international customers, and signed a seven-year framework agreement to TRIPLE PAC-3 Seeker production amid surging demand. Management reiterated its confidence in the segment’s march toward high-single-digit operating margins and expects meaningful upside to its five-year defense outlook given the current environment and rising US and allied defense budgets. Most importantly, the segment continues to reduce risk across development programs, with no major EAC adjustments during the quarter and new opportunities subject to tighter underwriting standards.

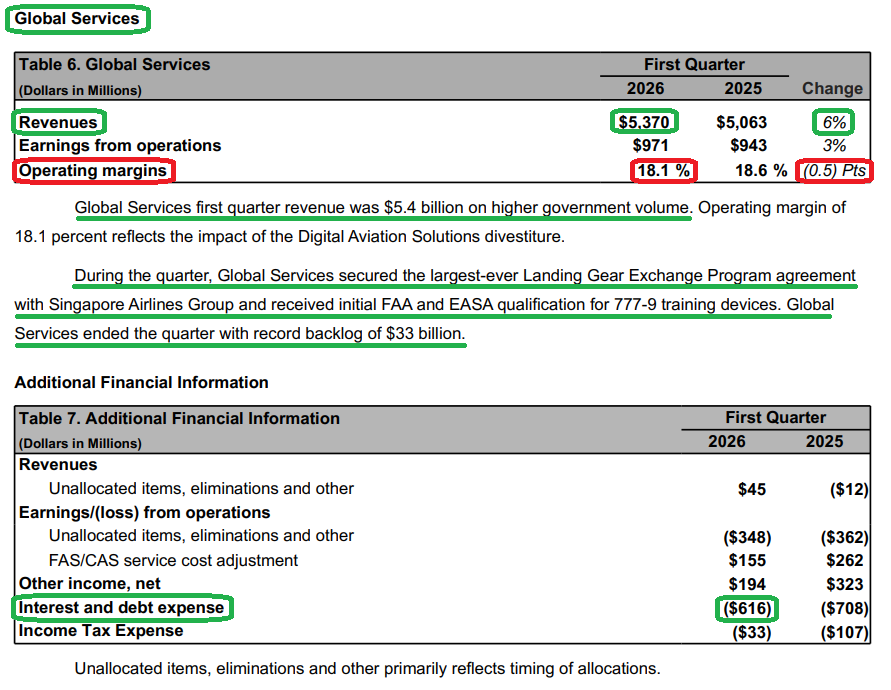

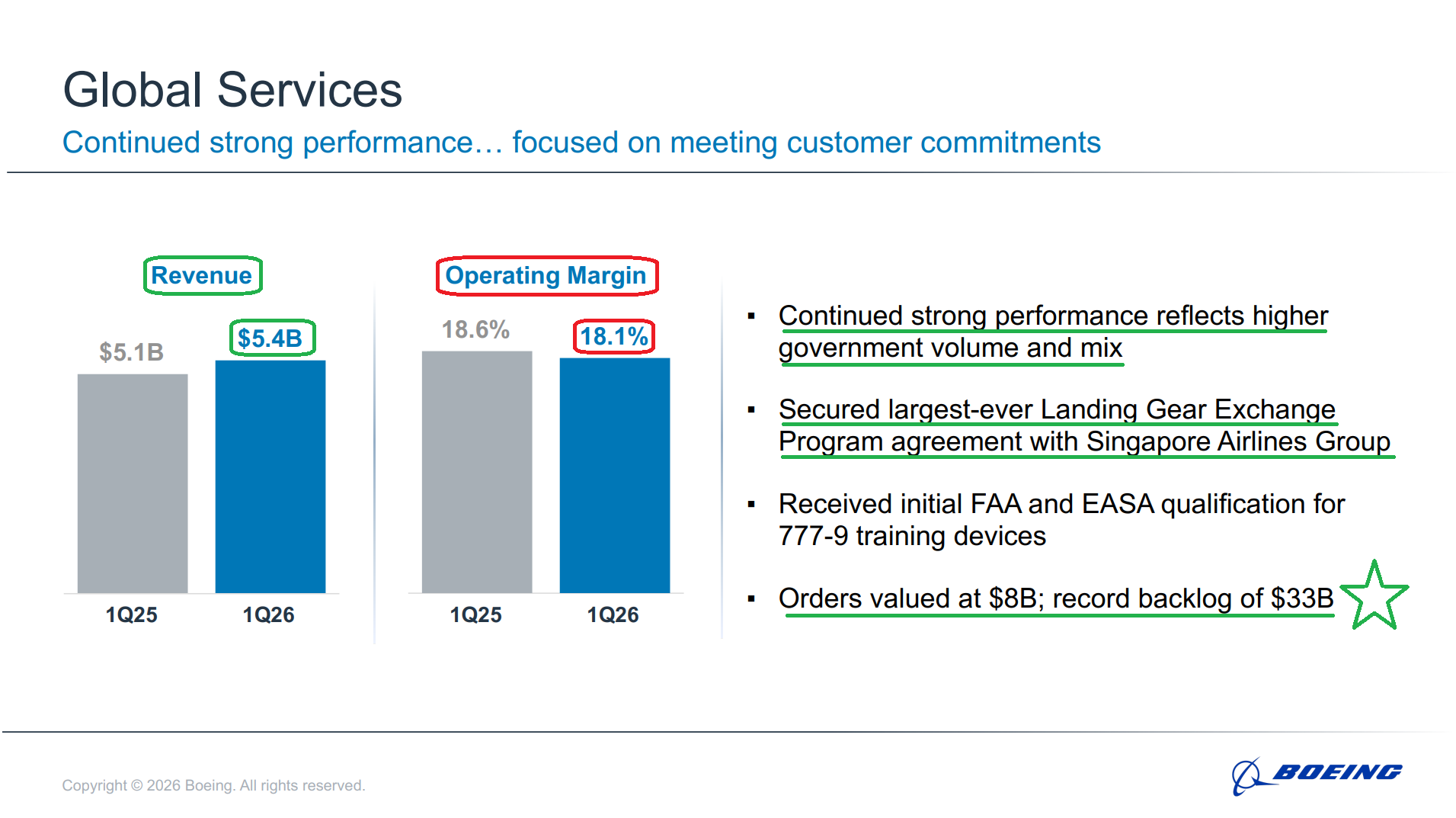

6) The Global Services segment posted revenue of $5.4B (+6% Y/Y) during the quarter, which jumps to +13% Y/Y when excluding the impact of the Digital Aviation Solutions divestiture. Both commercial and government businesses delivered double-digit operating margins, with overall operating margin contracting 50 bps Y/Y to 18.1% on the DAS divestiture and less favorable mix. BGS booked $8B of orders during the quarter for a book-to-bill of 1.6, ending with a record backlog of ~$33B. The segment also signed the largest landing gear exchange agreement in Boeing’s history with Singapore Airlines, covering more than 75 aircraft across their 737 MAX and 787 fleets. BGS has also implemented automation and AI to reduce proposal cycle time by ~25% YTD, a great example of what we mean when we say AI BENEFICIARY vs AI COST CENTER.

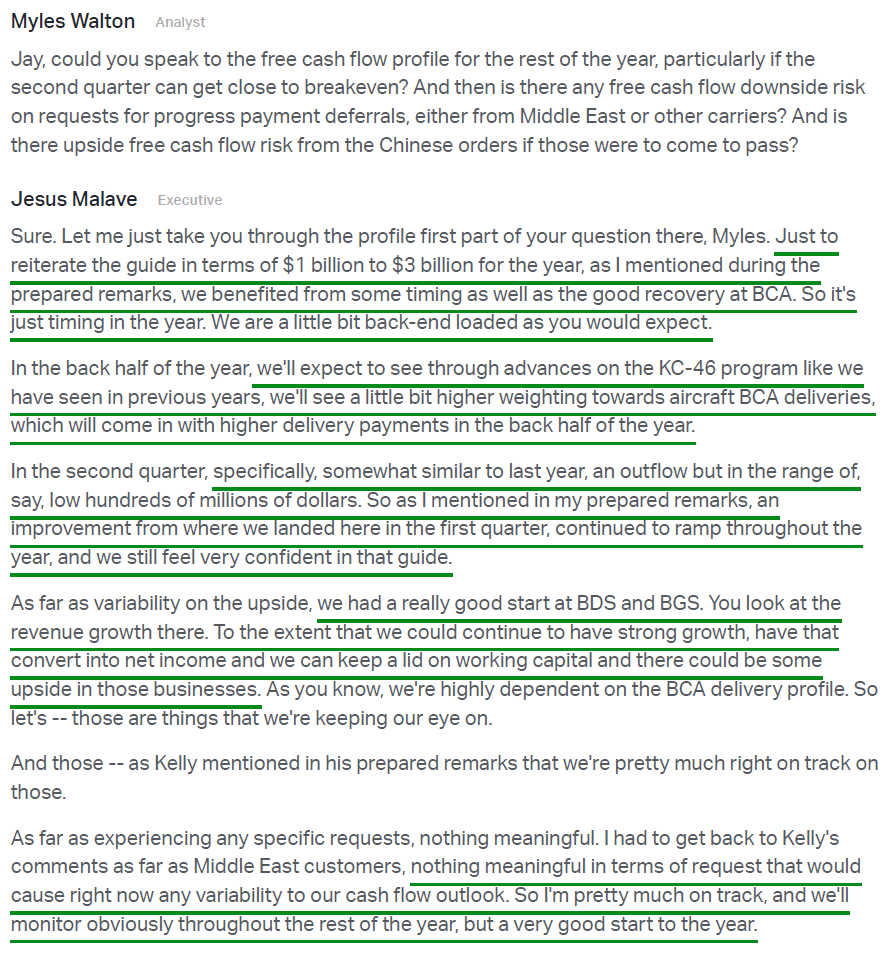

7) Free cash flow burn of $1.45B came in MUCH BETTER than the $2.61B consensus had penciled in and improved significantly from the $2.29B outflow last year. Management reiterated its 2026 free cash flow target of $1-3B, with Q2 expected to be a modest outflow in the range of a few hundred million and the back half turning positive and accelerating sequentially (includes the expected DOJ payment, now assumed to occur in the second half). Management also reiterated that the long-awaited $10B annual free cash flow figure remains very attainable, with significant growth beyond that level into the next decade.

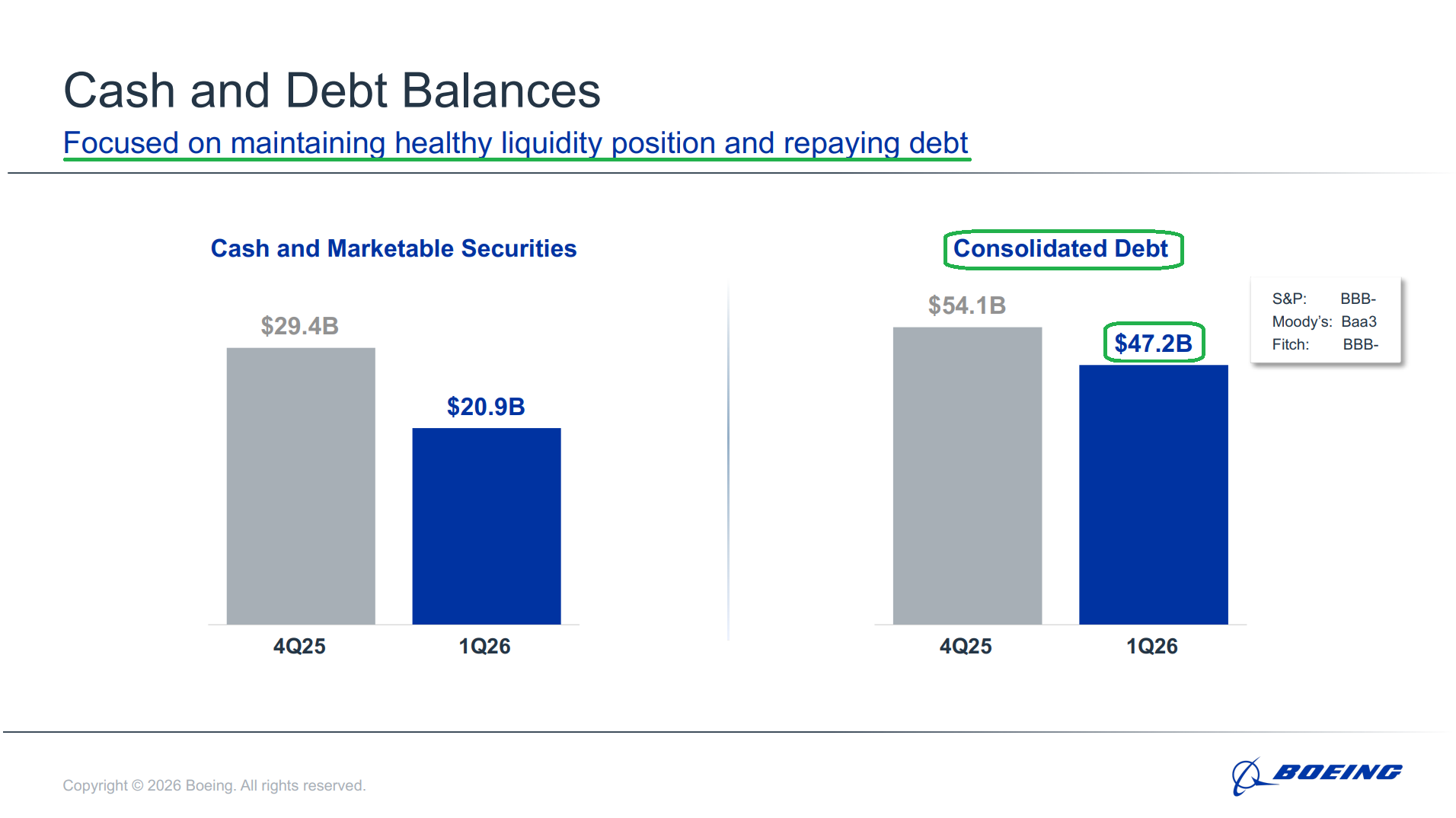

8) Cash and marketable securities ended the quarter at $20.9B, down from $29.4B at year-end, primarily reflecting debt repayments and the quarter’s FCF usage. Consolidated debt declined to $47.2B from $54.1B, with $1.4B of maturities remaining for the year and $10B of undrawn credit facilities available. Management remains firmly committed to strengthening the balance sheet and maintaining Boeing’s investment-grade credit rating as a top priority.

9) Management continues to expect certification of the long-delayed 737 MAX 7 and MAX 10 later this year, with deliveries starting in 2027 and the FAA noting no roadblocks to approval. The 737-10 made progress on the final phase of certification flight testing during the quarter, and the 787-9 and 787-10 received FAA certification for increased maximum takeoff weight. On the 777X, the program continues to make good progress, with first delivery still expected in 2027, and GE Aerospace believes it has identified the root cause of the previously flagged engine durability issue and is working on finalizing a modification.

10) On the Iran War, management noted ZERO impact on airplane deliveries to date, with no customers requesting delivery deferrals and no material supply chain disruptions. Boeing has delivered four airplanes to customers in the region as planned since the conflict began. While ~14% of Boeing’s unit backlog is tied to Middle East customers, two-thirds of that backlog delivers in 2030 and beyond, giving Boeing plenty of flexibility to re-sequence airplanes within a 12-18 month timeframe if needed. Several other customers have also already offered to pull forward deliveries if opportunities arise.

Earnings Call Highlights

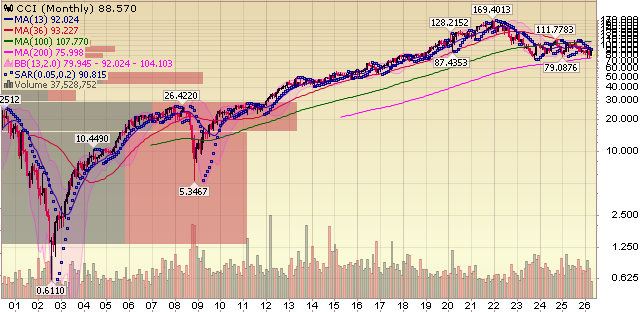

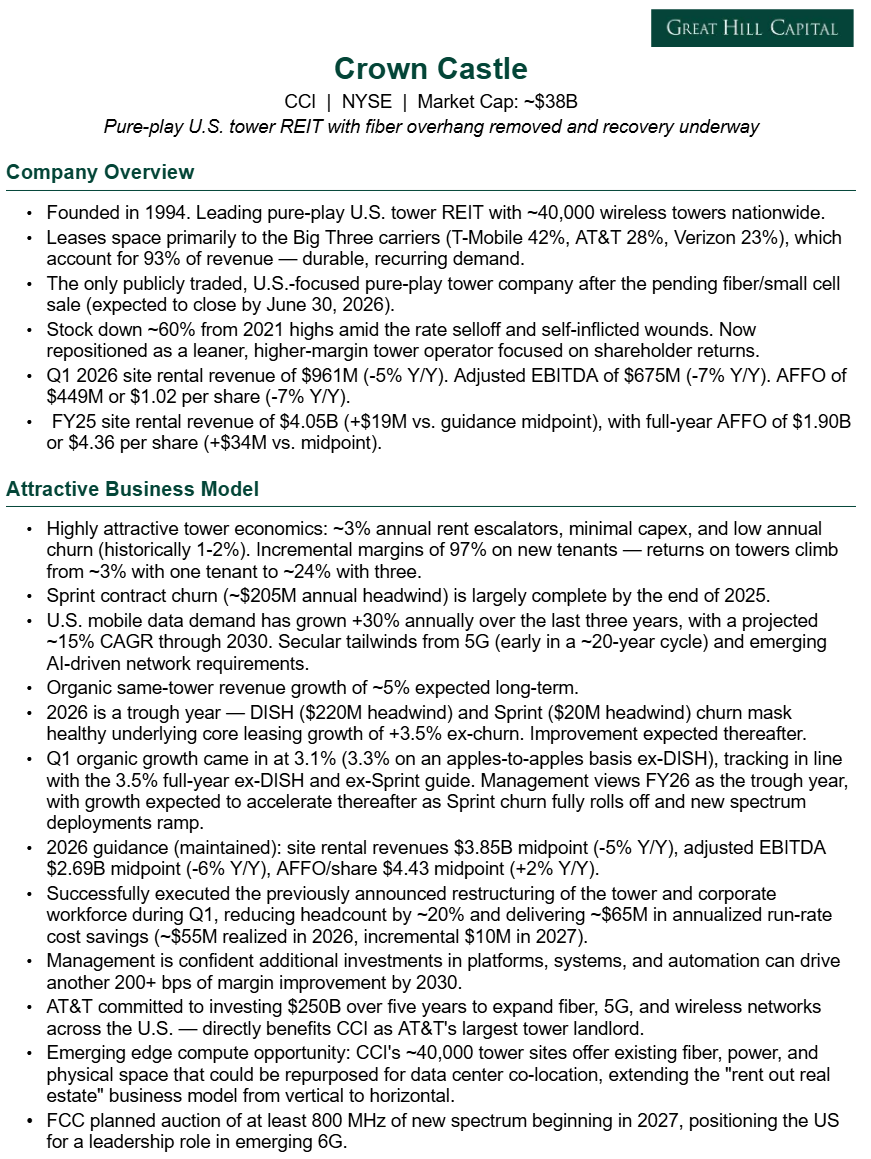

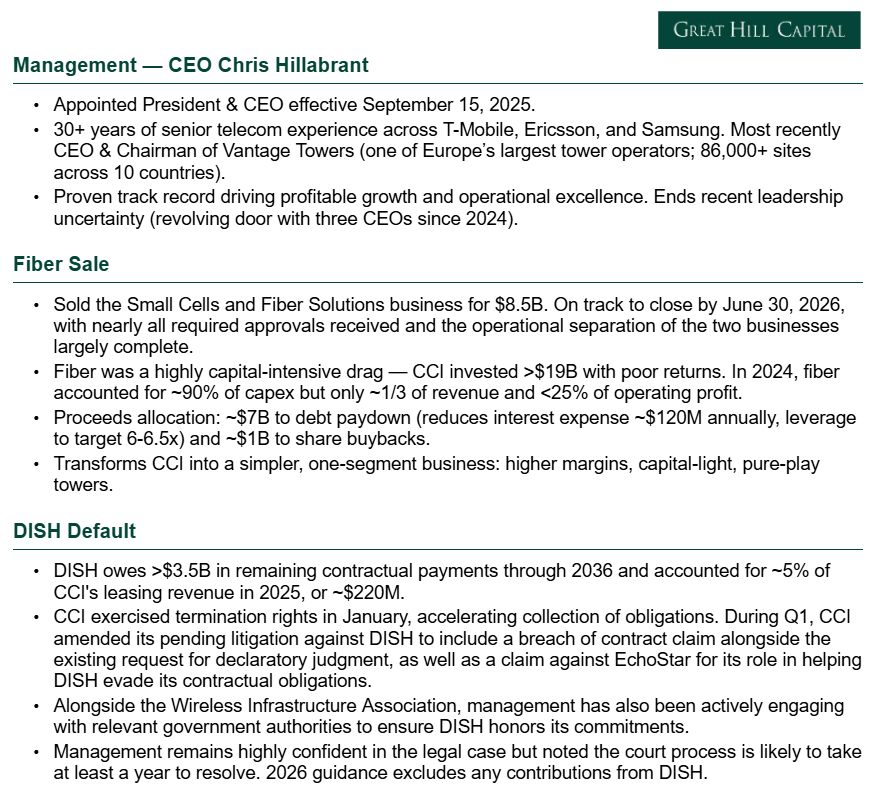

Crown Castle Update

For newer readers, here’s a brief overview of the key drivers behind our Crown Castle thesis, the only pure-play U.S. tower REIT and a high-yield income name that becomes increasingly hard to ignore as rates come down and capital rotates back into yield:

Q1 Earnings Breakdown

10 Key Points

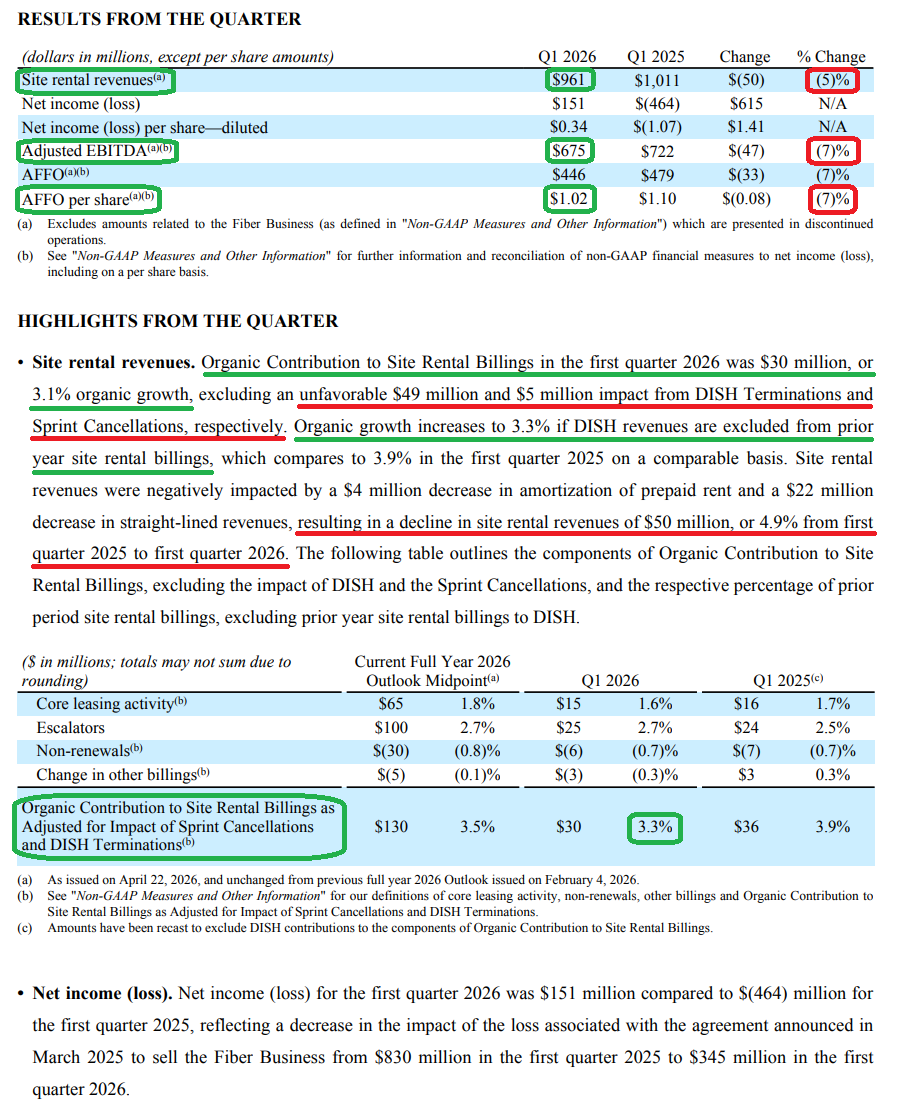

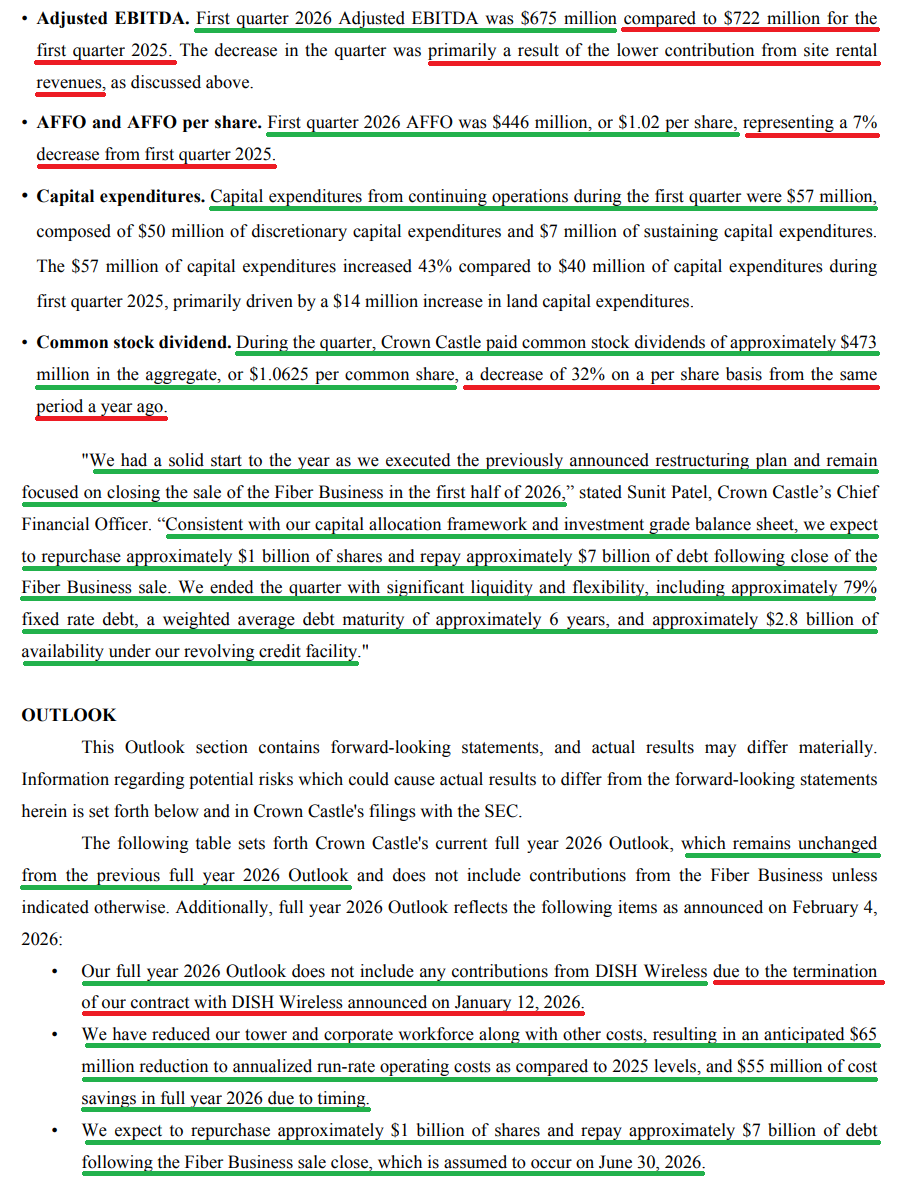

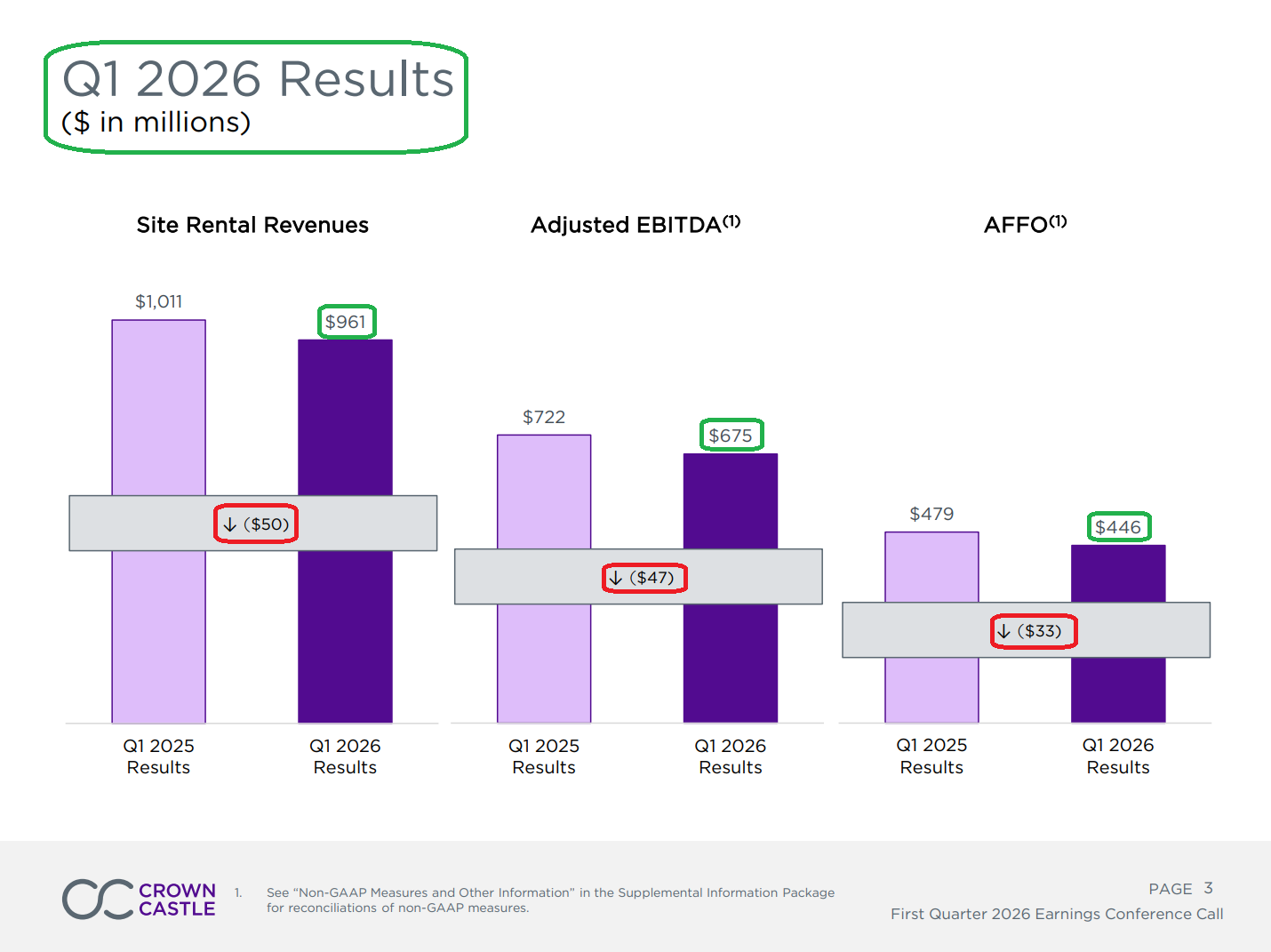

1) Q1 site rental revenue of $961M was down 5% Y/Y, with adjusted EBITDA of $675M (-7% Y/Y) and AFFO per share of $1.02 (-7% Y/Y). The Y/Y declines are almost entirely driven by the DISH termination and residual Sprint churn, masking healthy underlying leasing activity that continues to track in line with management’s full-year expectations.

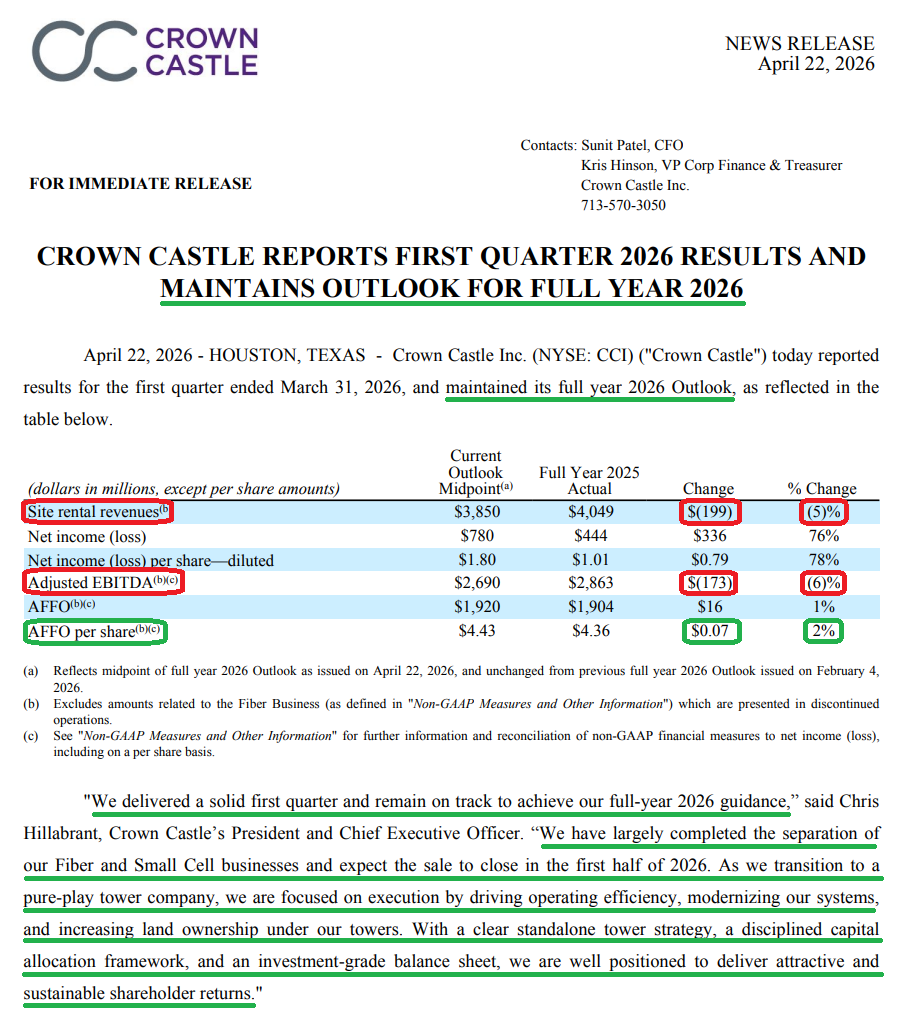

2) The $8.5B sale of the small cell and fiber solutions business remains on track to close by June 30, 2026, with management noting that almost all required approvals have been received and the operational separation of the two businesses is largely complete. Proceeds will be used to repay ~$7B of debt (reducing annual interest expense by ~$120M) and fund ~$1B in share repurchases. Upon closing, CCI will become the only publicly traded pure-play tower company focused exclusively on the US market.

3) Following DISH’s default on its payment obligations in January, CCI terminated the agreement and is now pursuing recovery of the remaining $3.5B+ owed through 2036 via federal court. During the quarter, management amended its pending litigation against DISH to include a breach of contract claim alongside the existing request for declaratory judgment, as well as a claim against EchoStar for its role in helping DISH evade its contractual obligations. Alongside the Wireless Infrastructure Association, management has also been actively engaging with relevant government authorities to ensure DISH honors its commitments. Management remains highly confident in the legal case but noted the court process is likely to take at least a year to resolve, with 2026 guidance excluding any contributions from DISH.

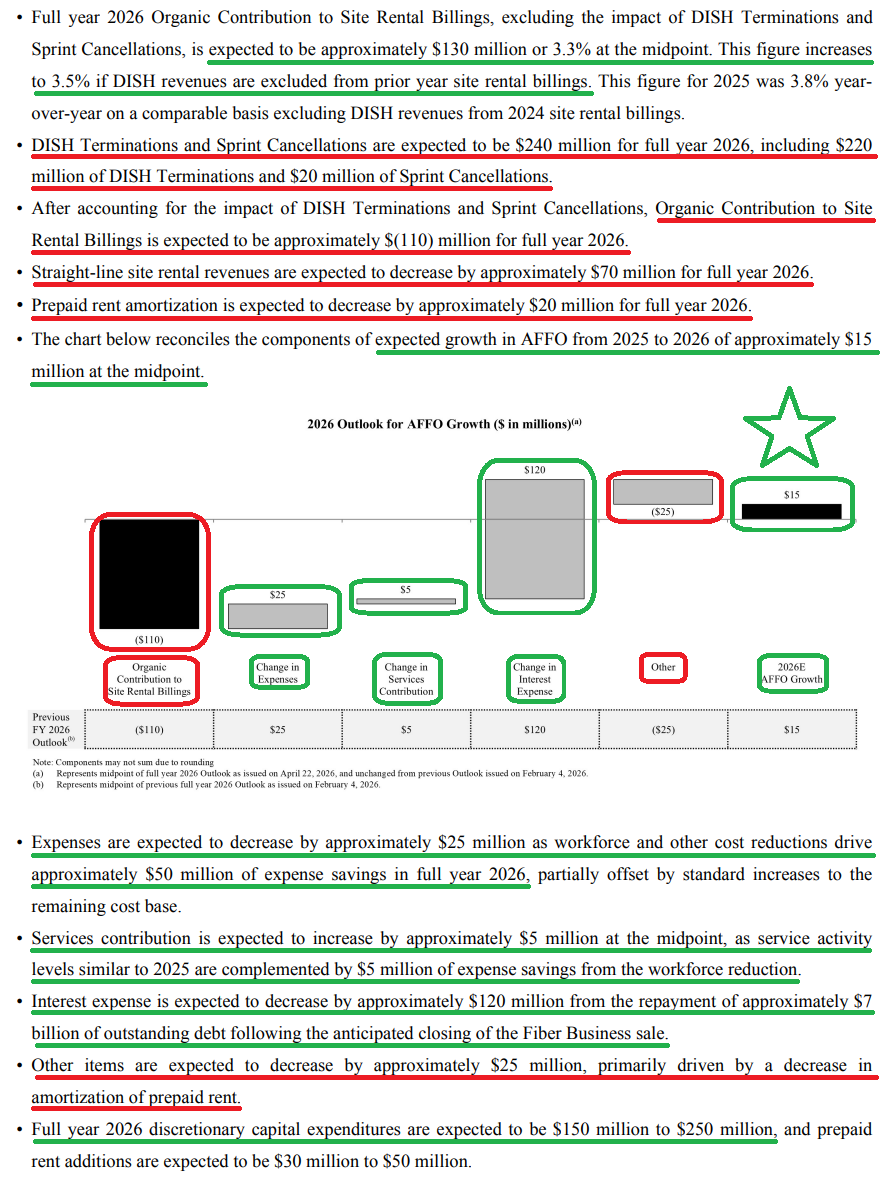

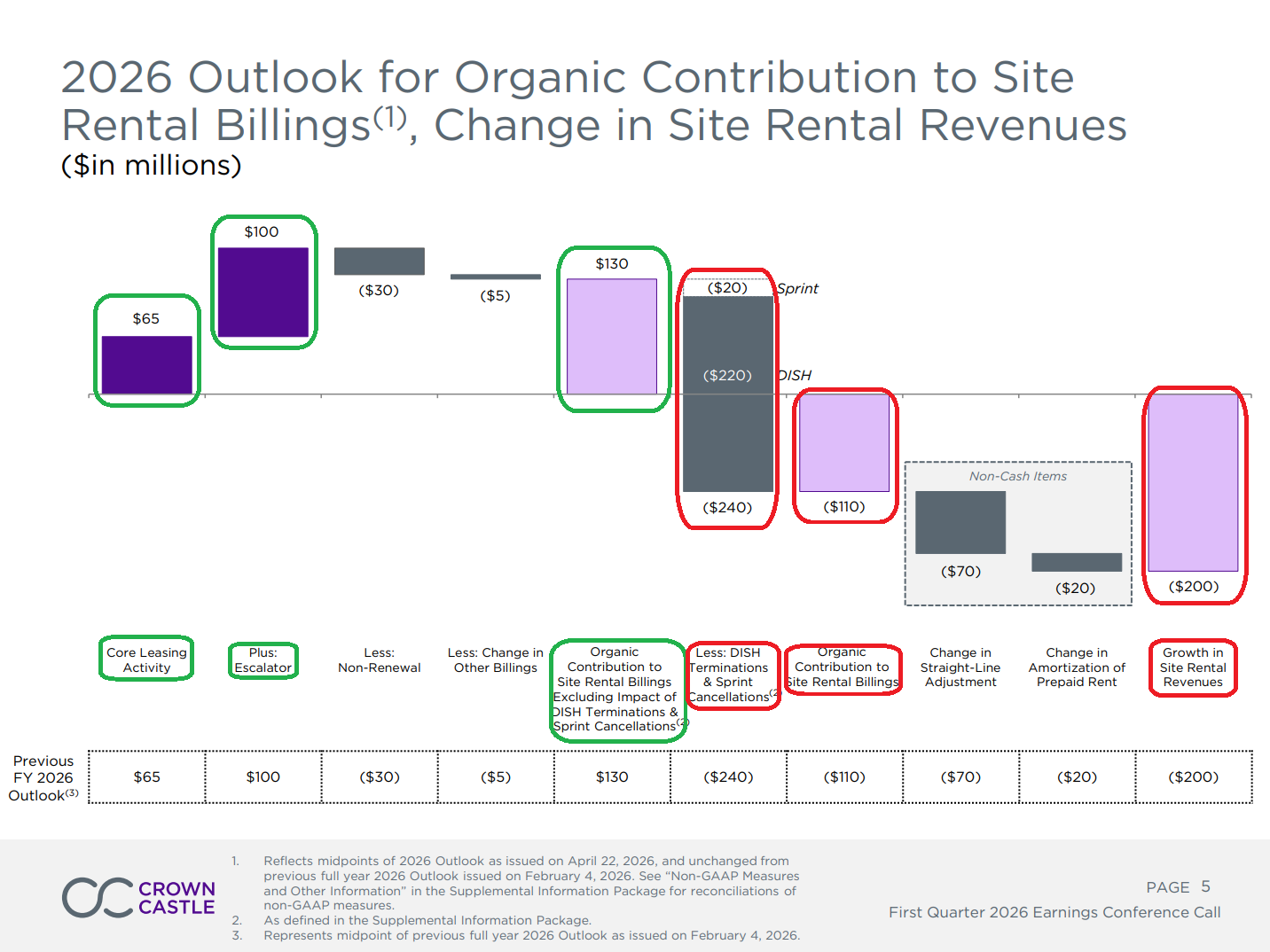

4) Organic growth came in at 3.1% for the quarter, excluding the impact of DISH terminations and Sprint cancellations, or 3.3% on an apples-to-apples basis once DISH is also removed from the prior year base. Growth was driven by +1.6% from core leasing activity and +2.7% from price escalators, partially offset by -0.7% from non-renewals and -0.3% from other billings, compared to 3.9% in Q1 2025. Management continues to view FY26 as the trough year for organic growth at 3.5% ex-DISH and ex-Sprint, with improvement expected thereafter as Sprint churn fully rolls off and new spectrum deployments begin to drive leasing activity higher.

5) Management successfully executed the previously announced restructuring of the tower and corporate organizations during the quarter, reducing the workforce by ~20% and delivering an anticipated $65M reduction in annualized run-rate operating costs versus 2025 levels. Of that total, $55M is expected to be realized in FY26, with the incremental $10M realized in 2027 due to the timing of non-labor reductions following the fiber sale close. Beyond the current restructuring, management is confident that ongoing investments in platforms, systems, and automation can drive an additional 200+ bps of margin improvement by 2030.

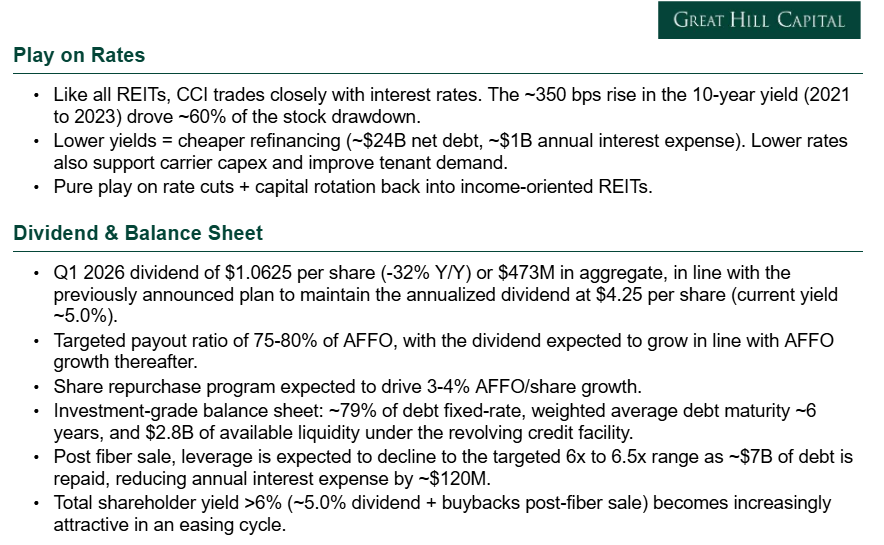

6) Management remains committed to maintaining an investment-grade balance sheet, ending the quarter with 79% of debt fixed, a weighted average debt maturity of ~6 years, and $2.8B of available liquidity under the revolving credit facility. Post fiber sale, leverage is expected to decline to the targeted 6x to 6.5x range as ~$7B of debt is repaid, further strengthening the balance sheet ahead of the pure-play transition.

7) CCI paid $473M in common stock dividends during the quarter, or $1.0625 per share (-32% Y/Y), in line with the previously announced plan to maintain the annualized dividend at $4.25 per share (current yield of ~5.0%), with a targeted payout ratio of 75-80% of AFFO and the dividend expected to grow in line with AFFO over time.

8) The long-term industry backdrop remains highly attractive, supported by persistent mobile data demand growth, upcoming spectrum deployments from CCI’s customers, and the FCC’s planned auction of at least 800 MHz of new spectrum beginning in 2027, which positions the US for a leadership role in emerging 6G. Management also pointed to an emerging edge compute opportunity, with CCI’s ~40,000 tower sites offering existing fiber, power, and physical space that could be repurposed for data center co-location, effectively extending the “rent out real estate” business model from vertical to horizontal.

9) On the competitive threat from satellite, management noted that current offerings remain a complementary technology rather than a substitute, with meaningful limitations around in-building coverage, line of sight, and mobility use cases. Public statements from carriers, satellite operators, and the Satellite Industry Association all point to the same conclusion, with management describing the impact on CCI’s business as de minimis and tower economics remaining firmly intact.

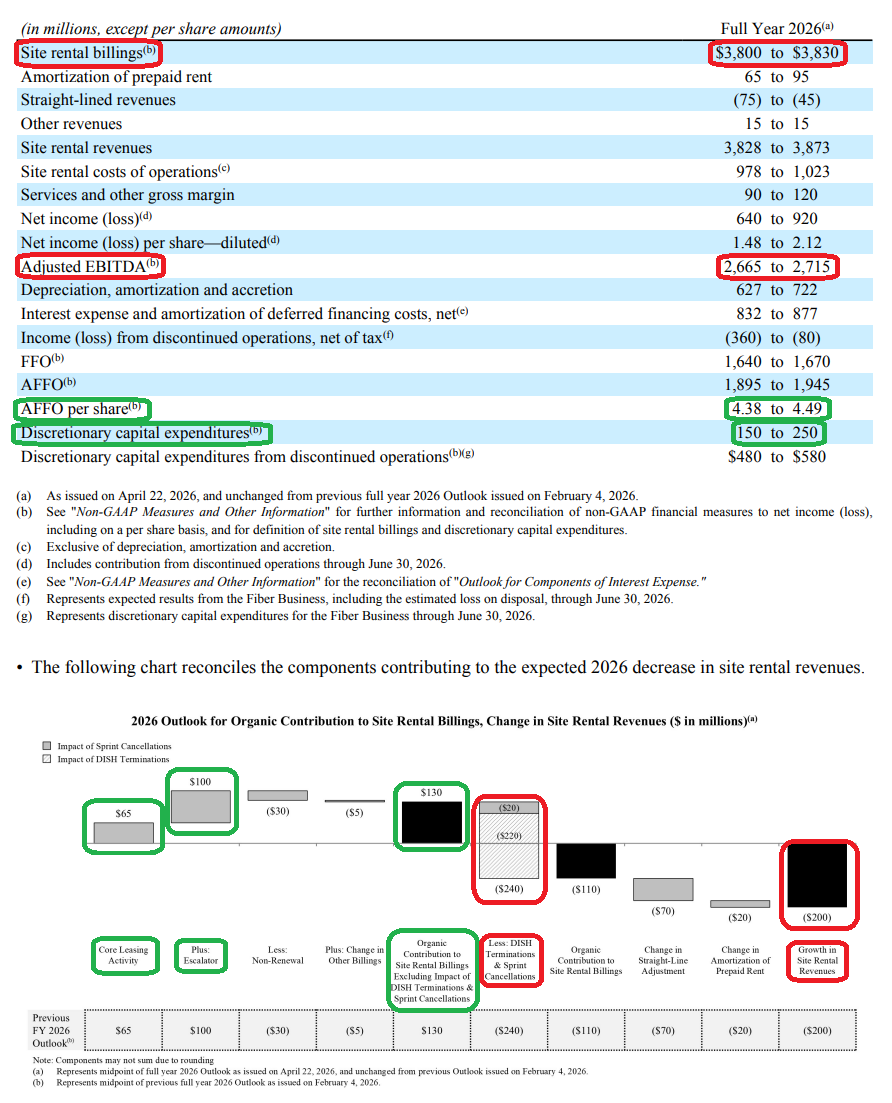

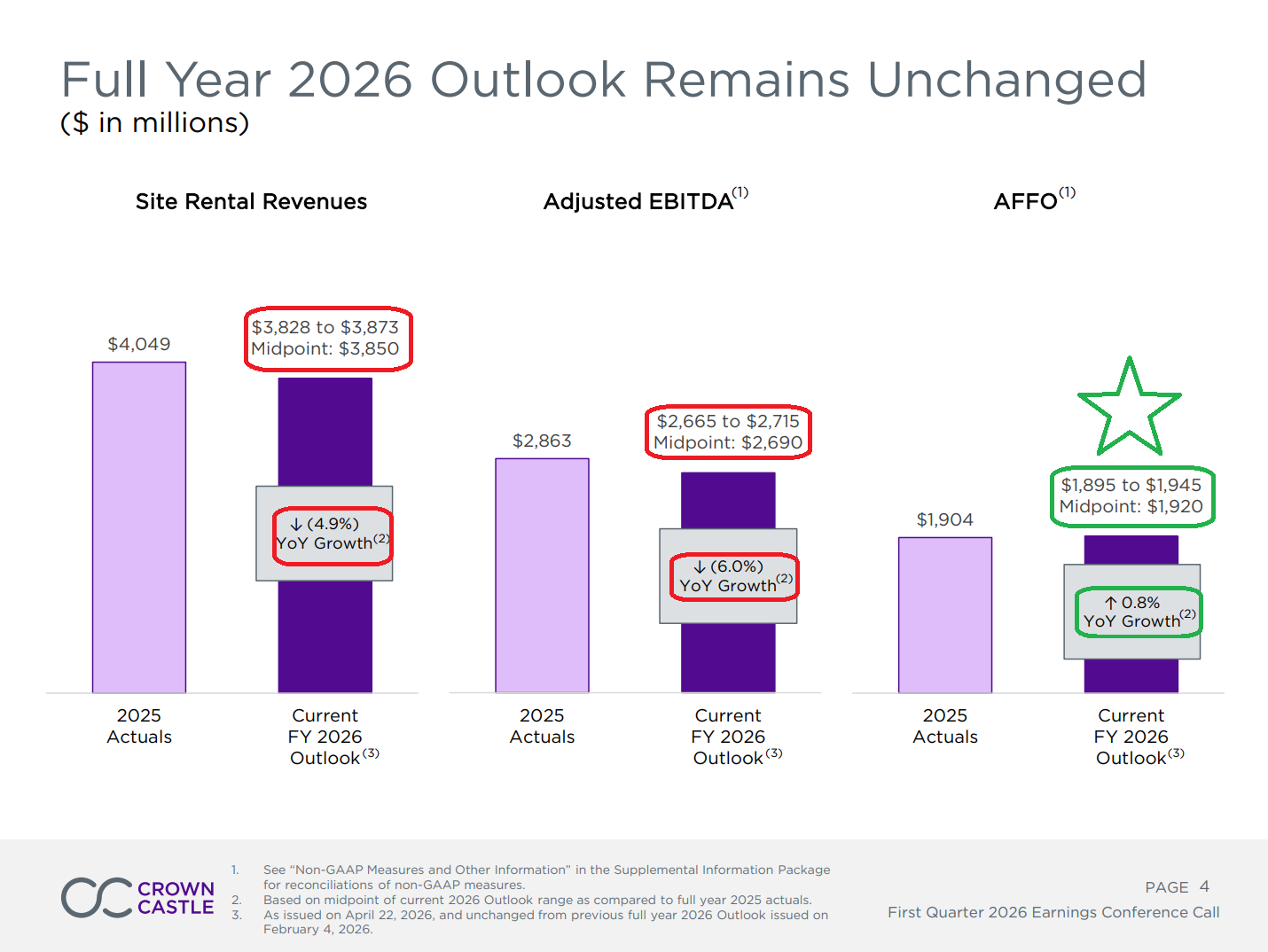

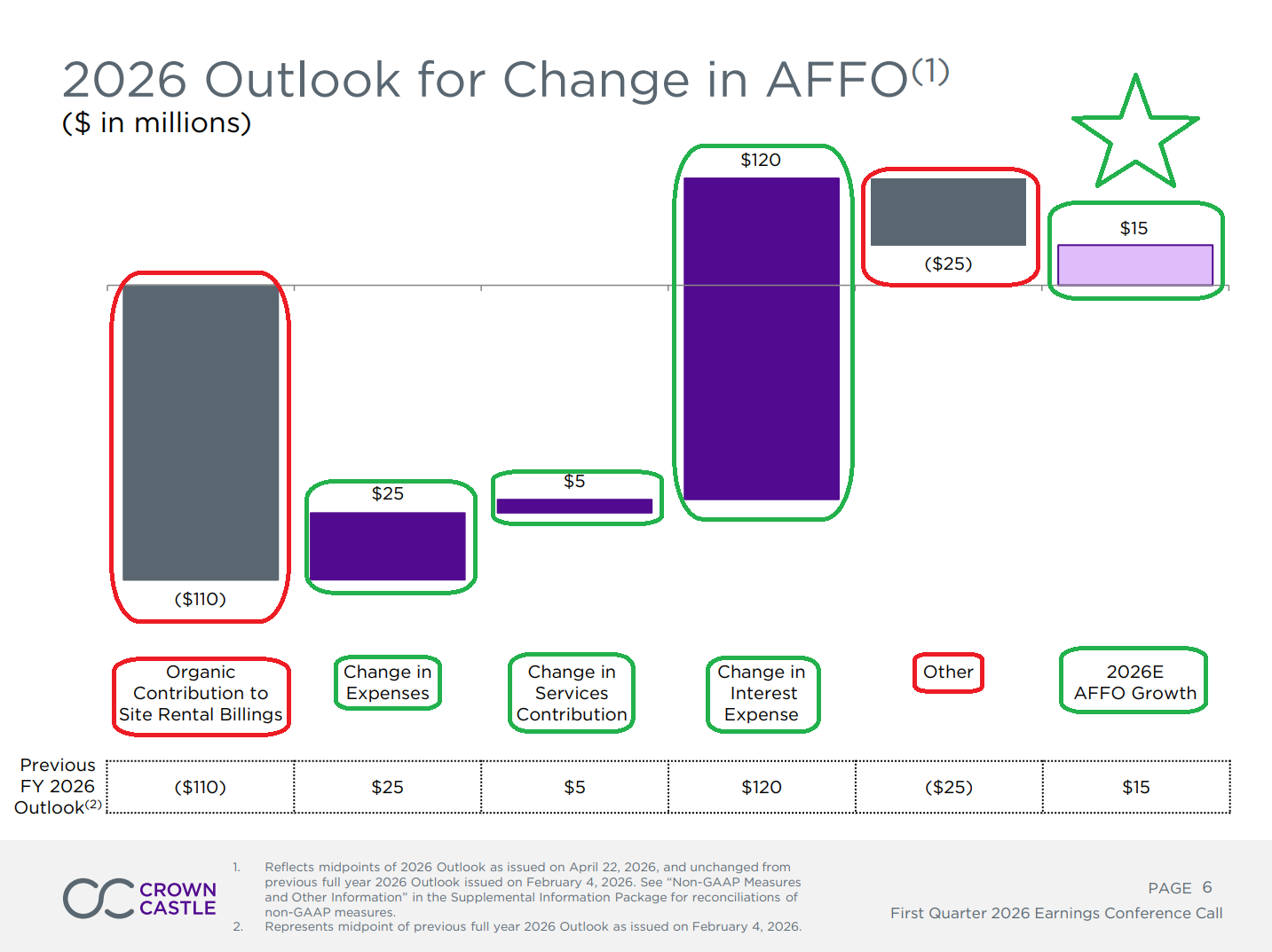

10) Management maintained full-year 2026 guidance across the board, with site rental revenues of $3.85B (-5% Y/Y), adjusted EBITDA of $2.69B (-6% Y/Y), and AFFO of $4.43 per share (+2% Y/Y) at the midpoint. The headline declines are entirely driven by the $220M DISH termination and $20M in residual Sprint cancellations, masking healthy underlying core leasing growth of +3.5% ex-churn. Importantly, AFFO is still expected to grow despite the $240M combined headwind, supported by opex savings and lower interest expense.

Earnings Call Highlights

General Market

The CNN “Fear and Greed Index” ticked up to 68 this week from 47 last week. You can learn how this indicator is calculated and how it works here: (Video Explanation)

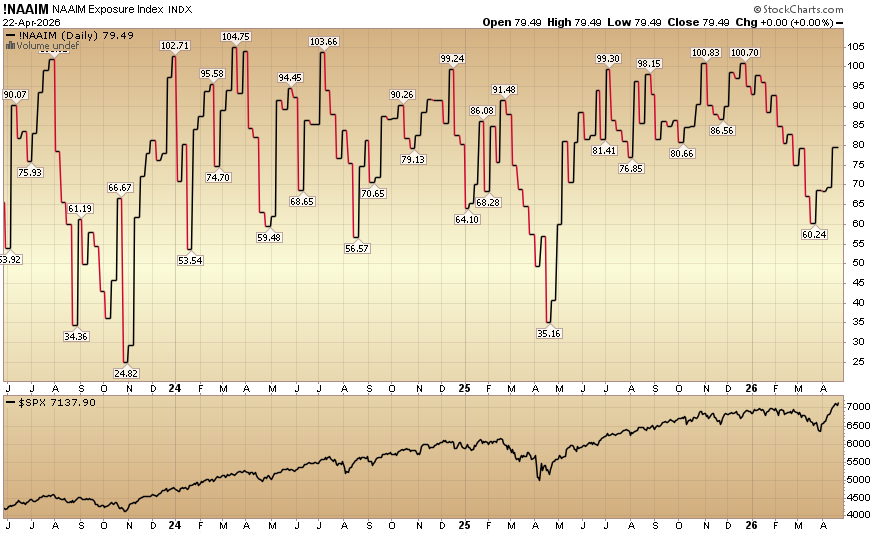

The NAAIM (National Association of Active Investment Managers Index) (Video Explanation) rose to 79.49% equity exposure this week from last week’s 69.38%.

Our podcast|videocast will be out sometime today. We have a lot of great data to cover this week. Each week, we have a segment called “Ask Me Anything (AMA)” where we answer questions sent in by our audience. If you have a question for this week’s episode, please send it in at the contact form here.

Larger accounts $5-10M+ can access bespoke service anytime here.

Not a solicitation.

*Opinion, Not Advice. See Terms