While most managers/investors like to talk about their winners (in hindsight), we prefer to spend the bulk of our time on ideas that have not yet left the station or are stalling before takeoff. In other words, things we can make money with prospectively versus ideas we have already made big money from.

That brings us to this week’s first focus of Baxter International.

Baxter International Inc., through its subsidiaries, develops and provides a portfolio of healthcare products worldwide. The company operates through four segments: Medical Products and Therapies, Healthcare Systems and Technologies, Pharmaceuticals, and Kidney Care. Baxter International Inc. was incorporated in 1931 and is headquartered in Deerfield, Illinois.

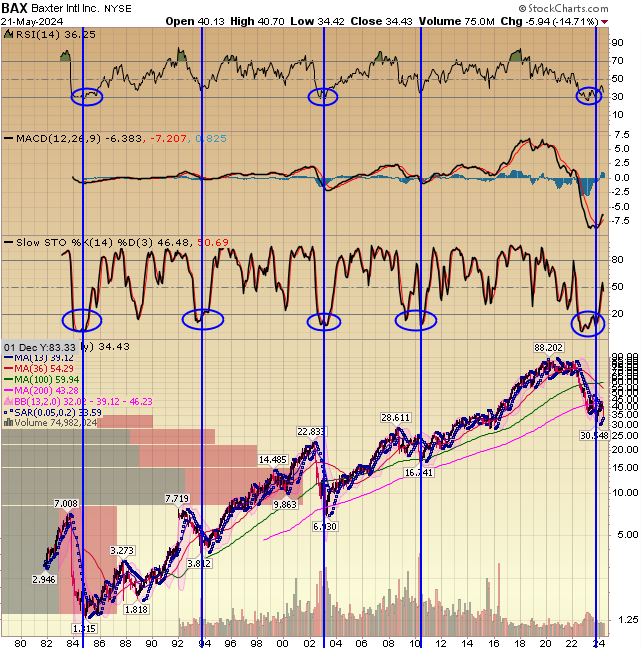

While the company was started in the heart of the Great Depression – 1931 – it is evident that it is not only a durable company (seen many cycles), but one that rarely affords the opportunity to buy the stock at a greater than 50% discount from its previous highs. In the last 40+ years there have only been 4 other such opportunities. In each case, the company eventually worked back up to new highs yielding a multi-bagger return for investors with enough staying “stomach” power to sit tight and trust the company to work through – yet another natural cycle.

This business has been a serial compounder for decades, but in recent years bit off a bit more than it could chew with the acquisition of HillRom in 2021. It’s taken a few years to digest, but now the company seems to be inflecting and turning the corner.

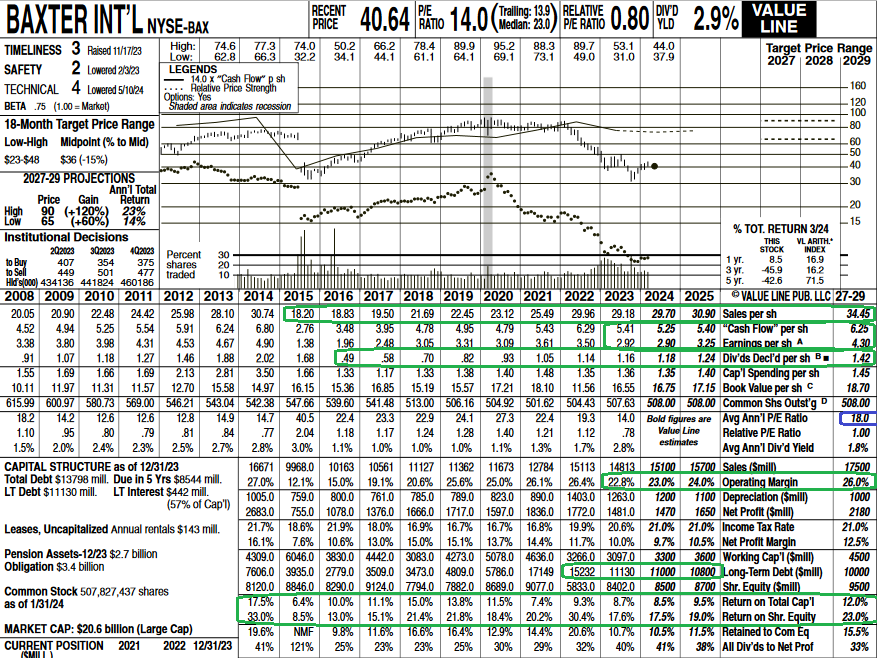

It currently trades at 10.7x forward earnings and offers a 3.31% (and GROWING) dividend yield while you wait for capital appreciation. This compares to its historic multiple of 18x and significantly lower dividend yield.

It currently trades at 10.7x forward earnings and offers a 3.31% (and GROWING) dividend yield while you wait for capital appreciation. This compares to its historic multiple of 18x and significantly lower dividend yield.

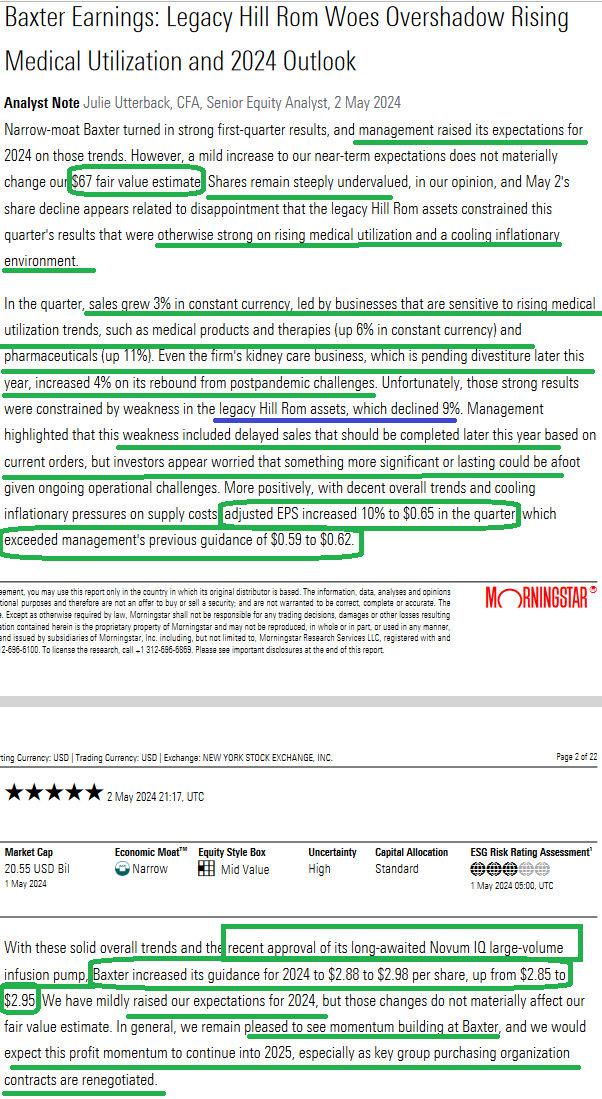

While the company has identified a solution to fix the low multiple and get the stock re-rated (spin or sell the slowest growing division – kidney care). The stock currently has an overhang due to the fact that management stated that the kidney care business may be sold instead of spun out to shareholders – but either way it will be completed in 2H 2024.

Markets don’t like uncertainty. With the recent sale of the biopharma business – they were able to pay down ~$3B of debt.

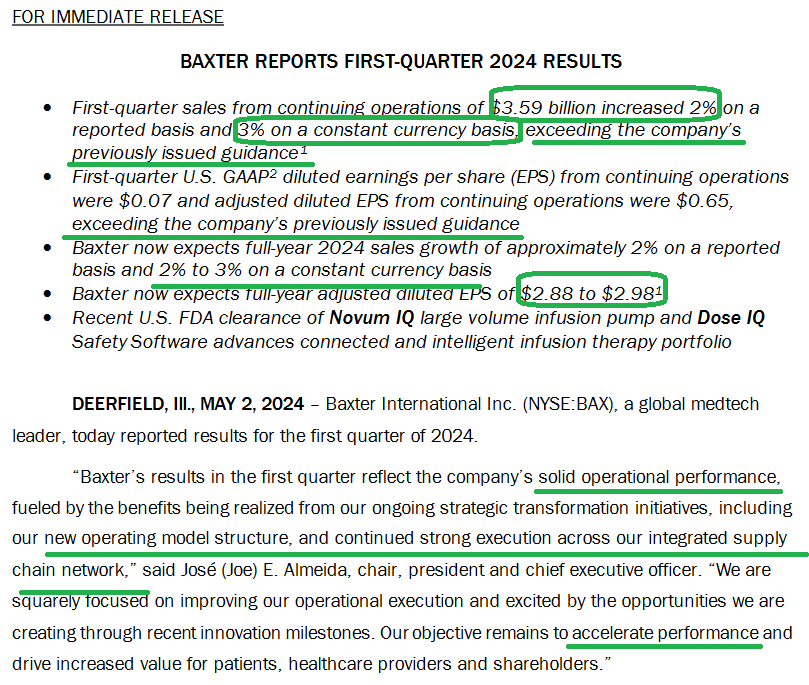

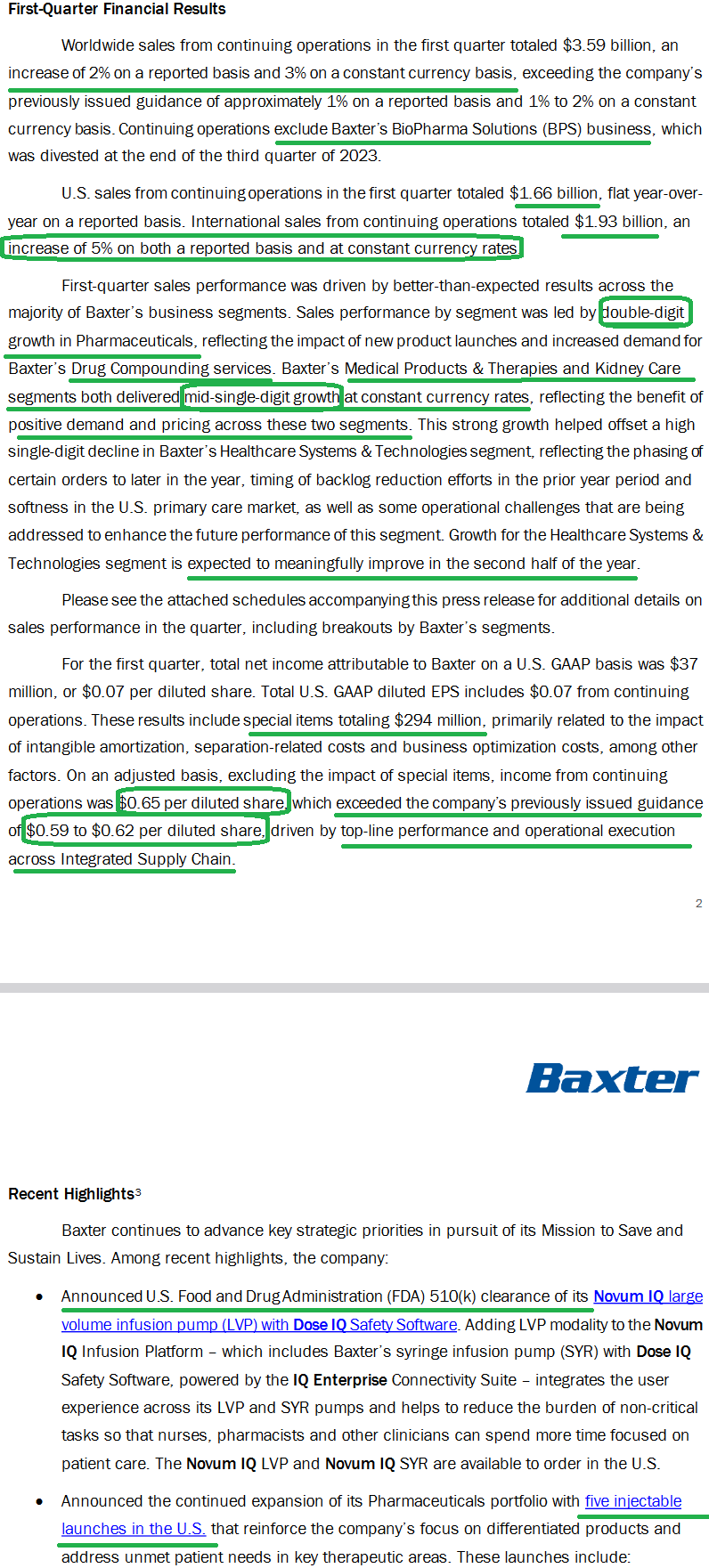

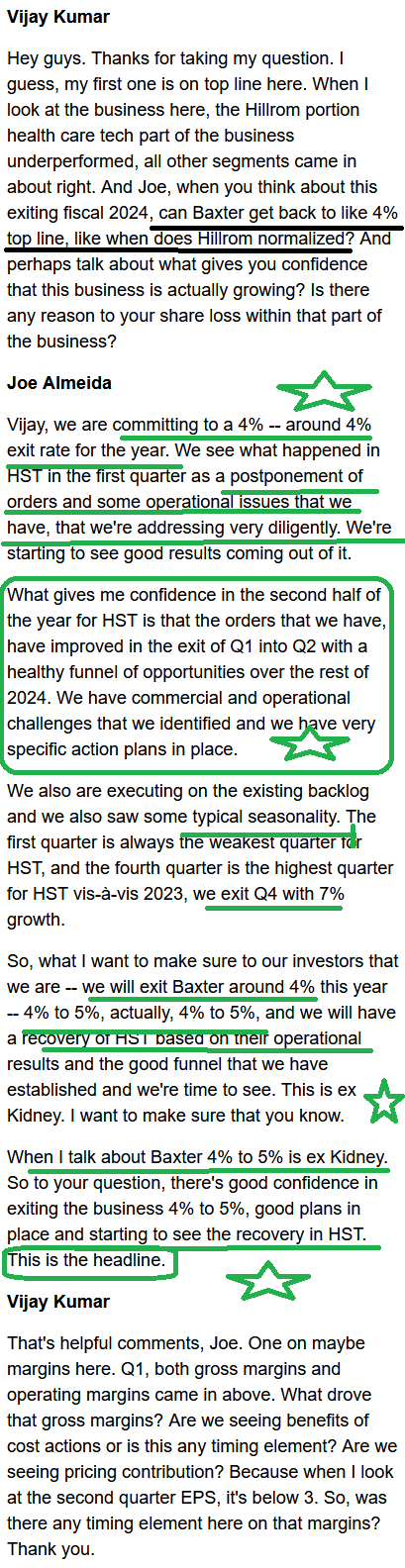

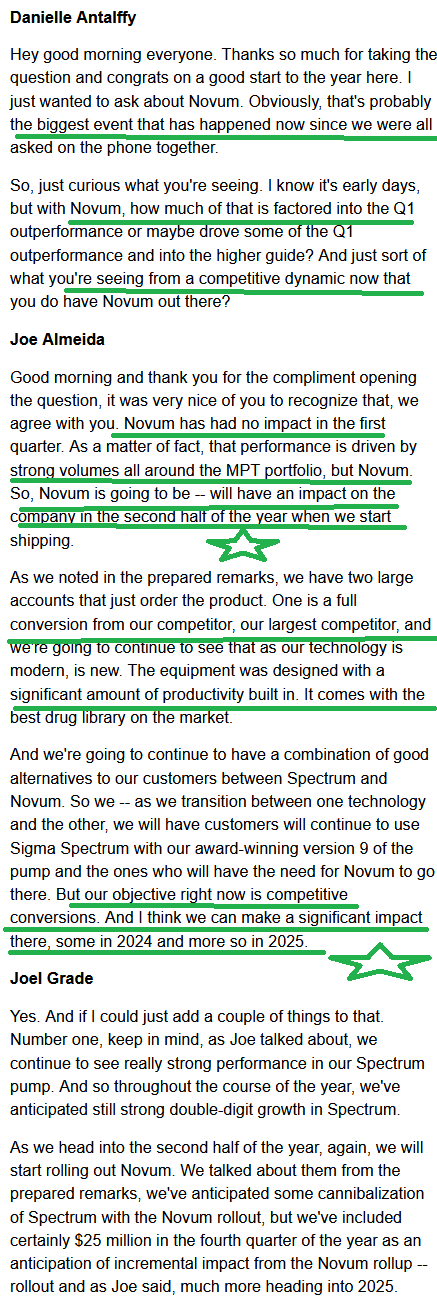

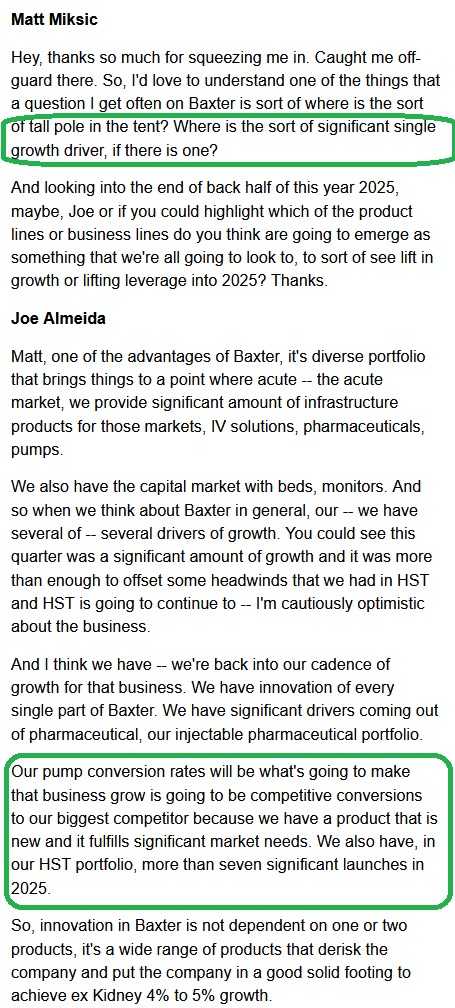

Here’s what we heard from management on this quarter’s earnings release and presentation:

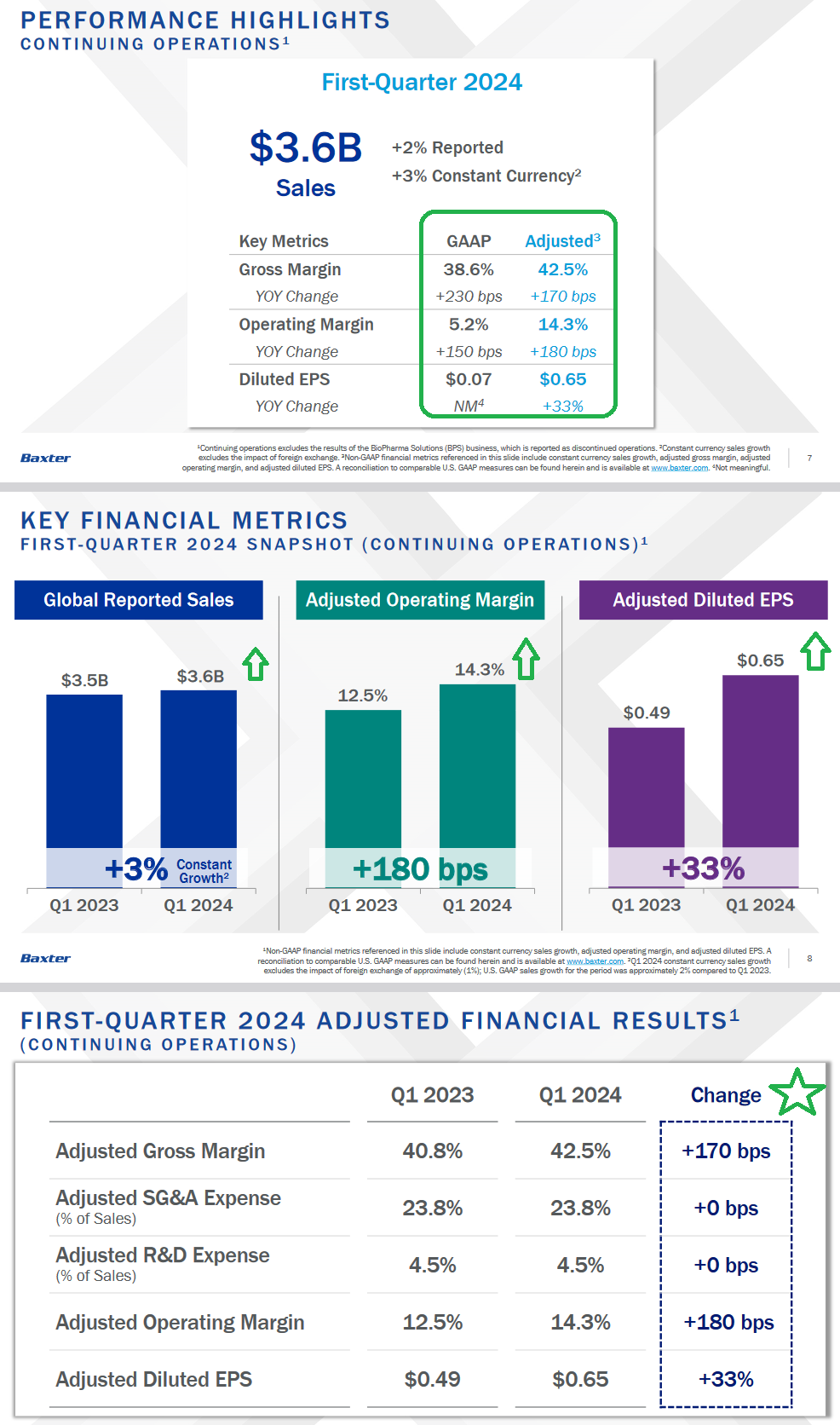

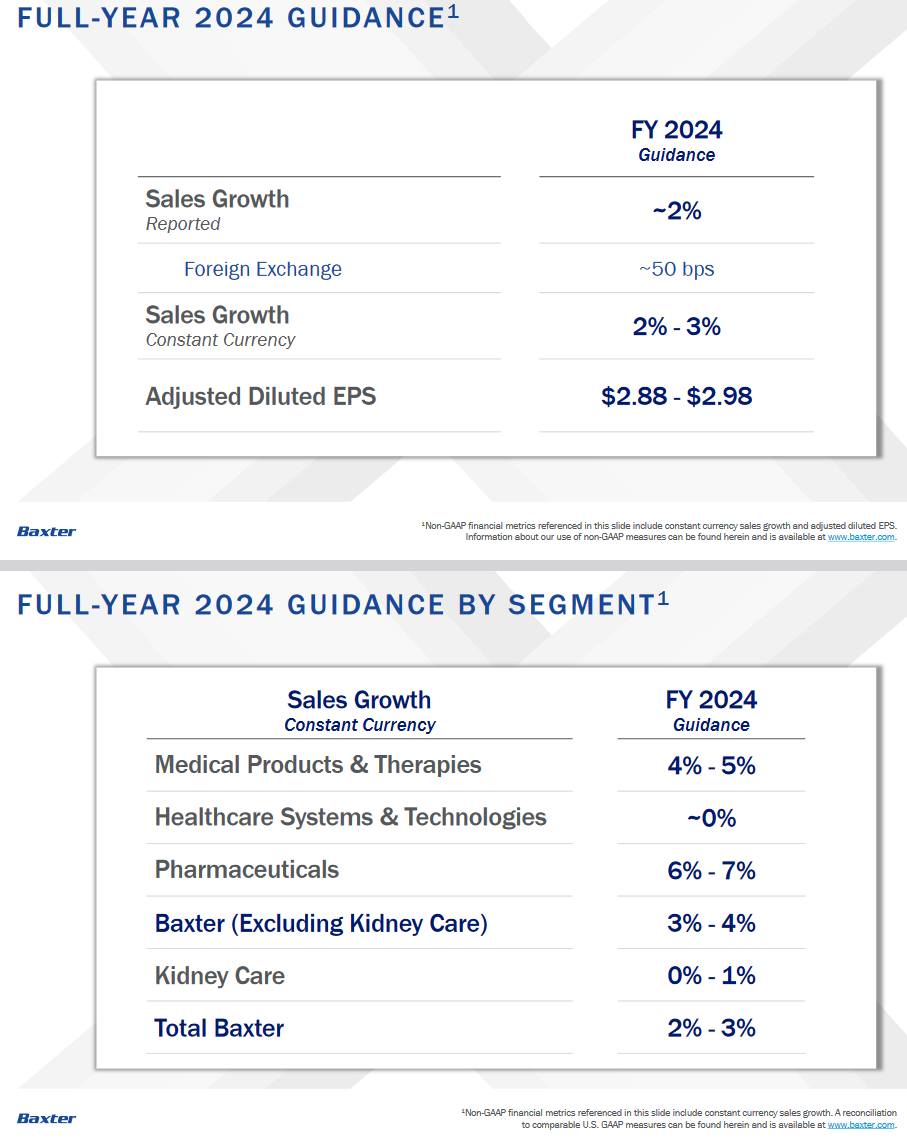

- Exceeded previous guidance on both top and bottom line.

- Raised guidance.

- Released new products.

- Disclosed they were in discussions for outright SALE of kidney business to private equity. Whether sold or spun it would be completed by 2H 2024.

Here’s what Julie Utterback at Morningstar had to say about the results and outlook:

Here’s what Julie Utterback at Morningstar had to say about the results and outlook:

- Sales increasing.

- Operating Margins increasing.

- EPS increasing.

- $5.7B of liquidity.

- Share repurchases coming.

- Continuing to retire debt.

- Growth recovery.

- Strong guidance.

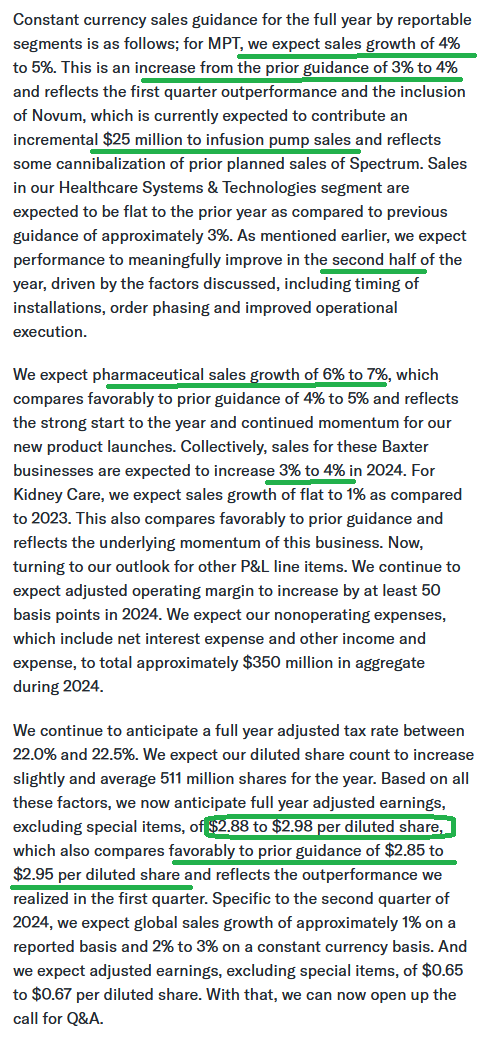

From the earnings call:

VF Corp

VF Corp reported earnings after the bell last night. At first blush, they were not good. Our thesis in VF Corp is predicated on Bracken Darrell’s ability to turn around the company. We are betting on the jockey. It’s what he has a history of doing from his days at Logitech. When he became CEO at Logitech in January of 2013, the stock had been declining for several years – to the tune of -82%. The blue vertical line (below) is when he took over.

Within 7.5 years the stock was > a 27-bagger ($1M invested became > $27M). Of note, for almost the first year he was CEO and turning the company around from an 82% decline (that preceded him), the stock continued to go lower before it finally turned. The same thing is happening with the turnaround at VF corp. He has made a lot of changes at the company in 10 months, but the stock is drifting down (before it turns around and he shocks everyone – just like he did at Logitech).

Oddly enough, he took the helm in July 2023 (blue vertical line) after the stock was down just over 82% as well and it has drifted lower in his early months at the helm (just like Logitech before the turn).

At the end of the day, the first catalyst will be the sale of the “packs business”(Jansport/Eastpak) and/or a sale of Supreme (rumored that Goldman Sachs has been shopping it for them). One morning we will wake up and see that they have created a billion dollars+ of asset sales and the stock will jump (when no one expects it).

Then, by the grace of God and the hand of Bracken, sales from the remaining units will begin to accelerate (when least expected). Finally, (my guess) we’ll see new hot brands added to the portfolio that no one can imagine right now to anchor the next phase of growth. How do we know this? Because they’ve been running the same playbook since 1899. Same plays, different players. They always reinvent and recover to new levels.

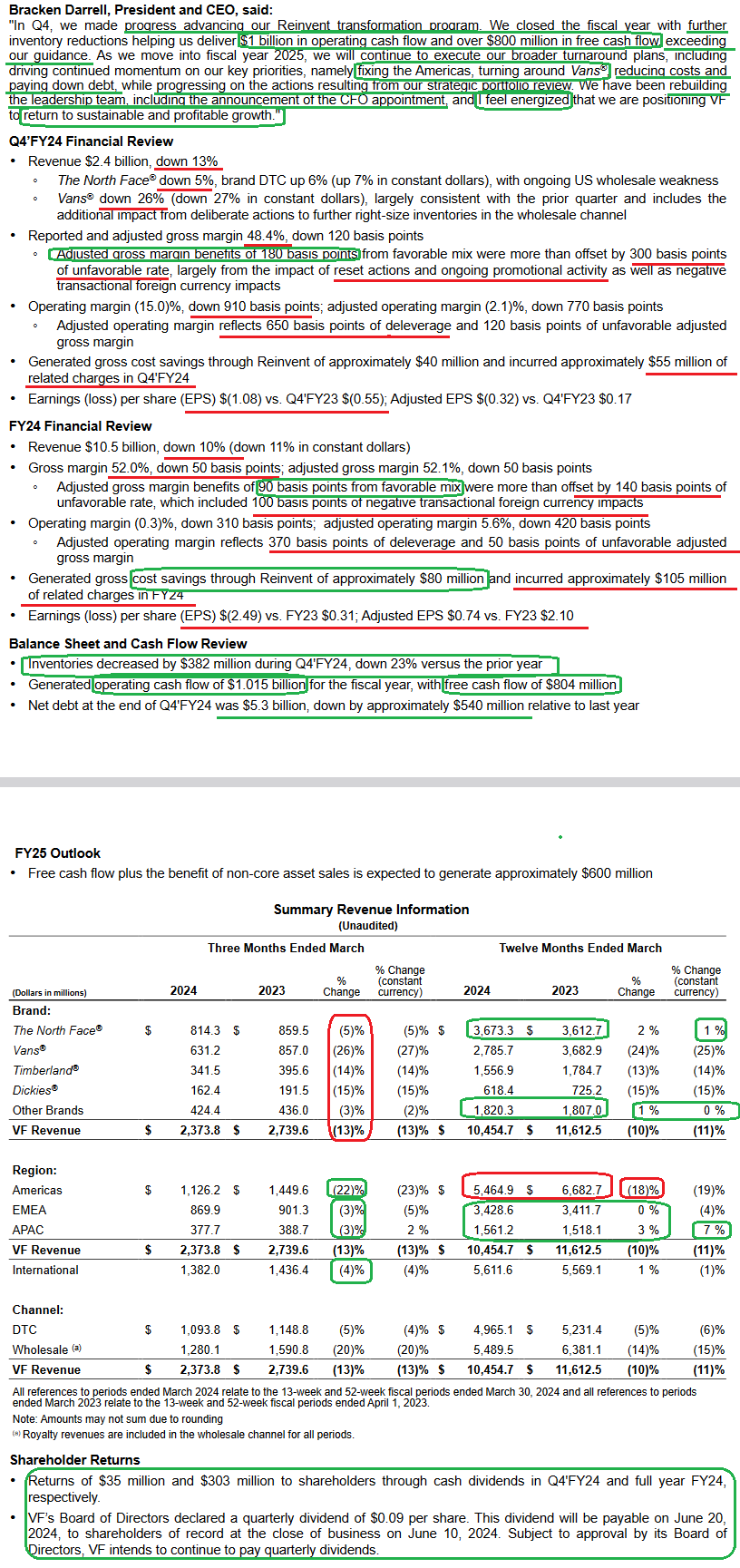

While they missed on the top and bottom lines last night and the market didn’t like it:

![]()

This is a short-term phenomenon. As I always say, the name of the game with turnarounds is FREE CASHFLOW to give them enough runway to implement the turnaround plan. Here’s what happened last night:

- Exceeded Operating Cash Flow Guidance for fiscal year at $1B delivered.

- Exceeded Free Cash Flow Guidance for fiscal year at $800M delivered.

- APAC and EMEA regions grew in aggregate year on year. Americas needs work.

- Inventories normalizing.

- Took $80M of costs out of the business.

Now onto the shorter term view for the General Market:

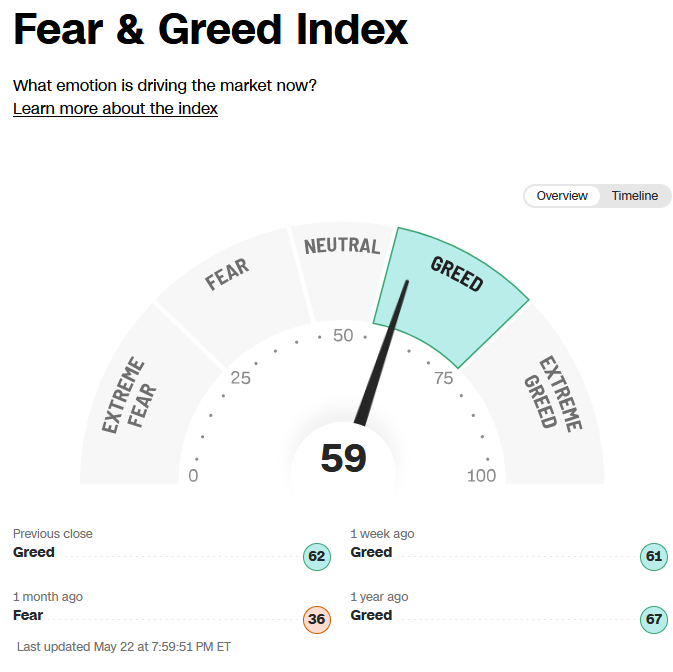

The CNN “Fear and Greed” flat-lined from 60 last week to 59 this week. You can learn how this indicator is calculated and how it works here: (Video Explanation)

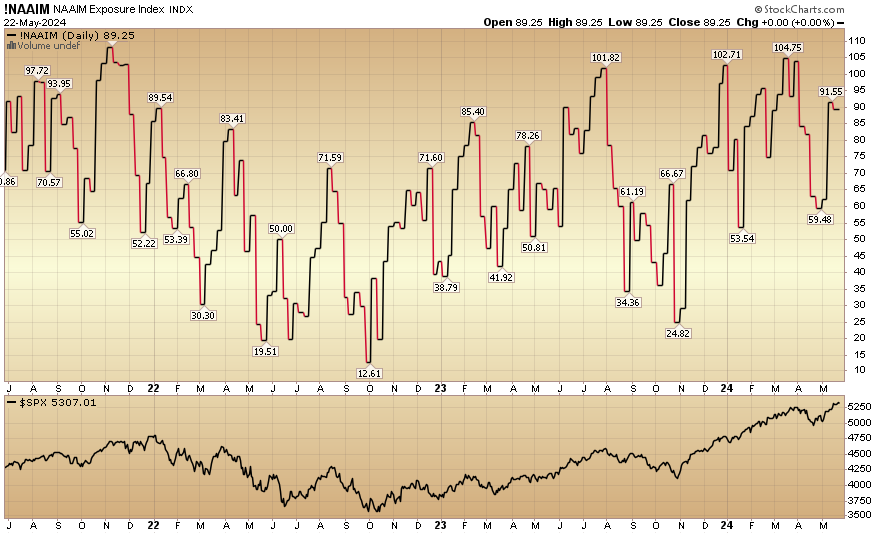

The NAAIM (National Association of Active Investment Managers Index) (Video Explanation) flat-lined to 89.25% this week from 91.55% equity exposure last week.

Our podcast|videocast will be out later today. Each week, we have a segment called “Ask Me Anything (AMA)” where we answer questions sent in by our audience. If you have a question for this week’s episode, please send it in at the contact form here.

Congratulations to all of the new clients who came in so far this year during our Q1 and Q2 openings. We are now closed to smaller accounts ($1M+) again as of three weeks ago and will remain closed to smaller accounts until sometime in Q3. Larger accounts $5-10M+ can access bespoke service at their preference here.

*Opinion, Not Advice. See Terms

Not a solicitation.