Key Market Outlook(s) and Pick(s)

On Monday, I joined Ash Webster on Fox Business’ Varney & Co. to discuss markets, the economy, outlook, Iran, and a lot more. Thanks to Stuart Varney, Ash, and Maggie Edwards for having me on:

QXO Update

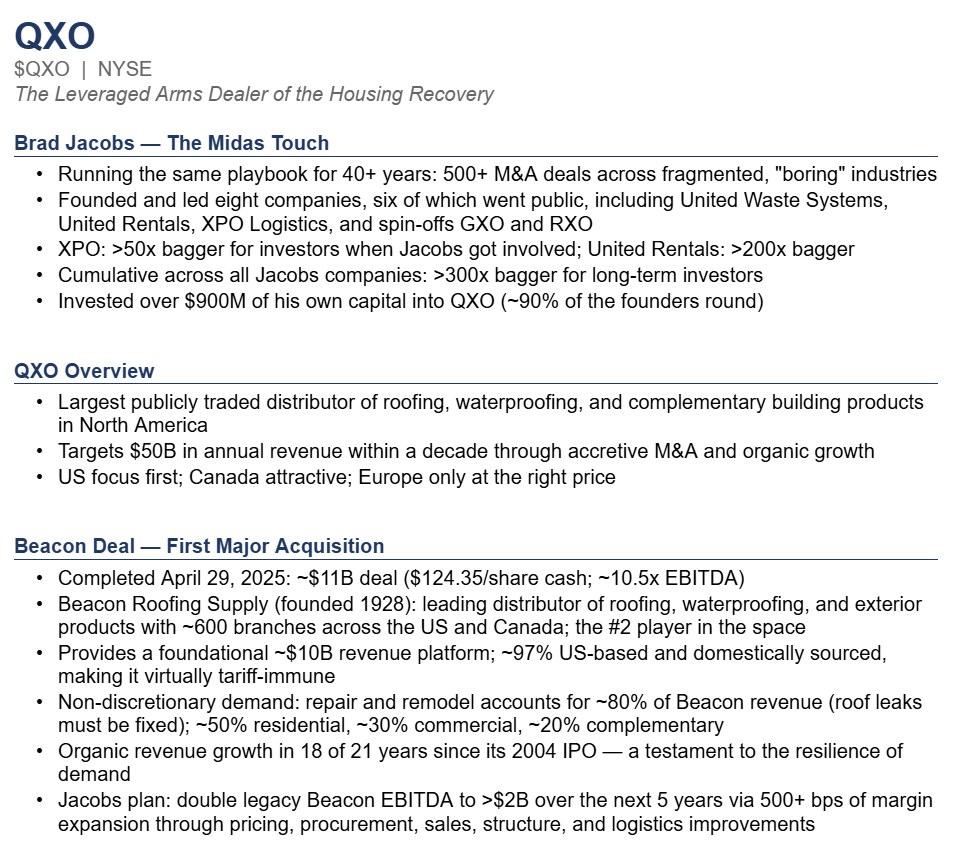

For newer readers, here’s a quick overview of the key drivers behind our thesis on QXO, Brad Jacobs’ latest venture and one of our favorite arms dealer plays on a U.S. housing market recovery:

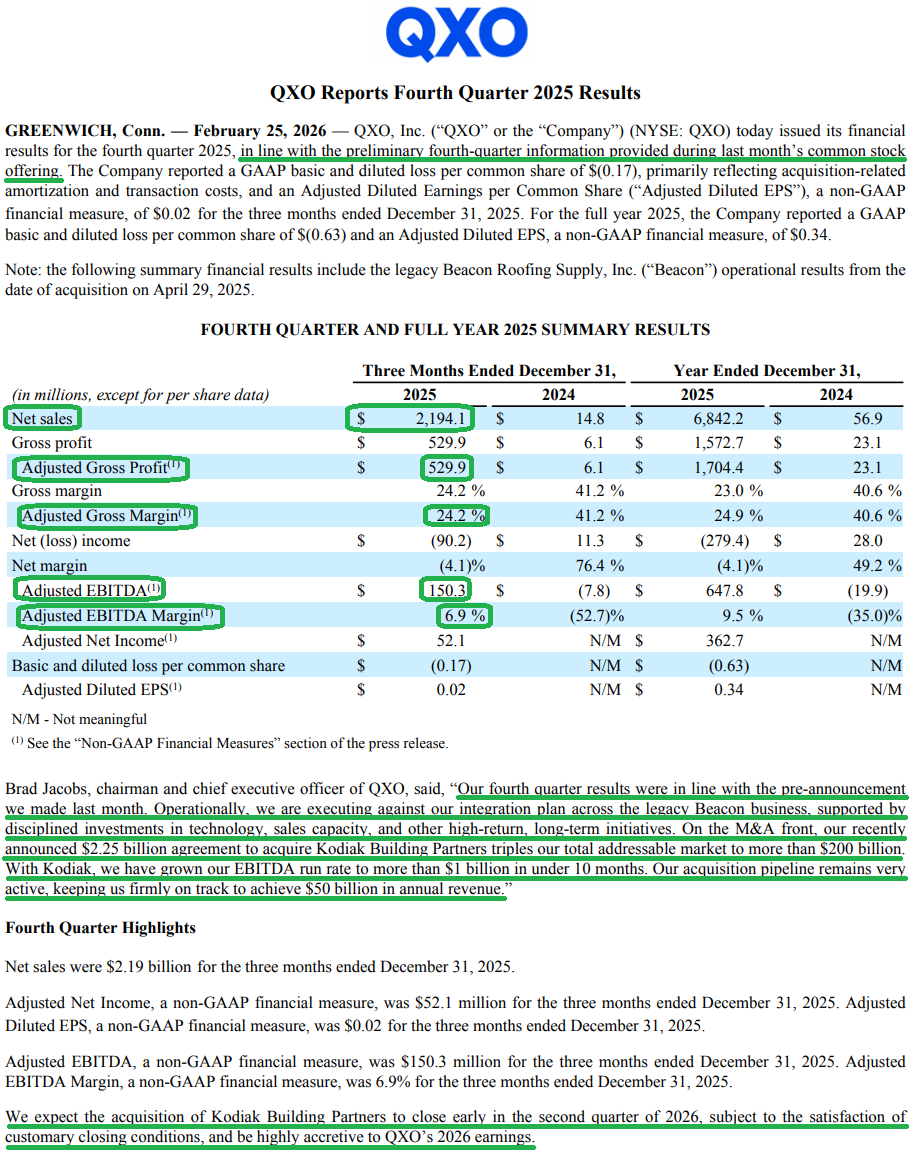

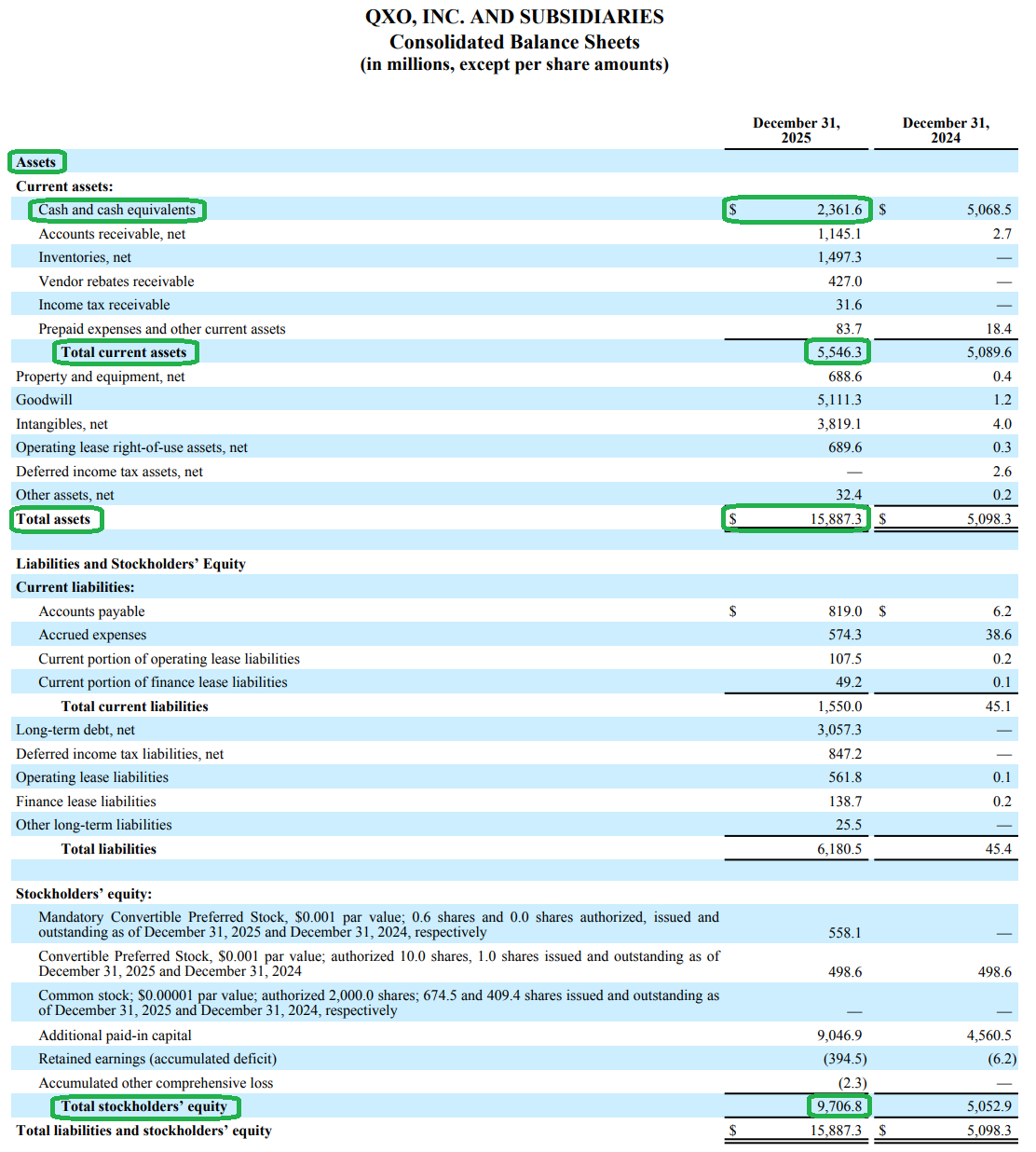

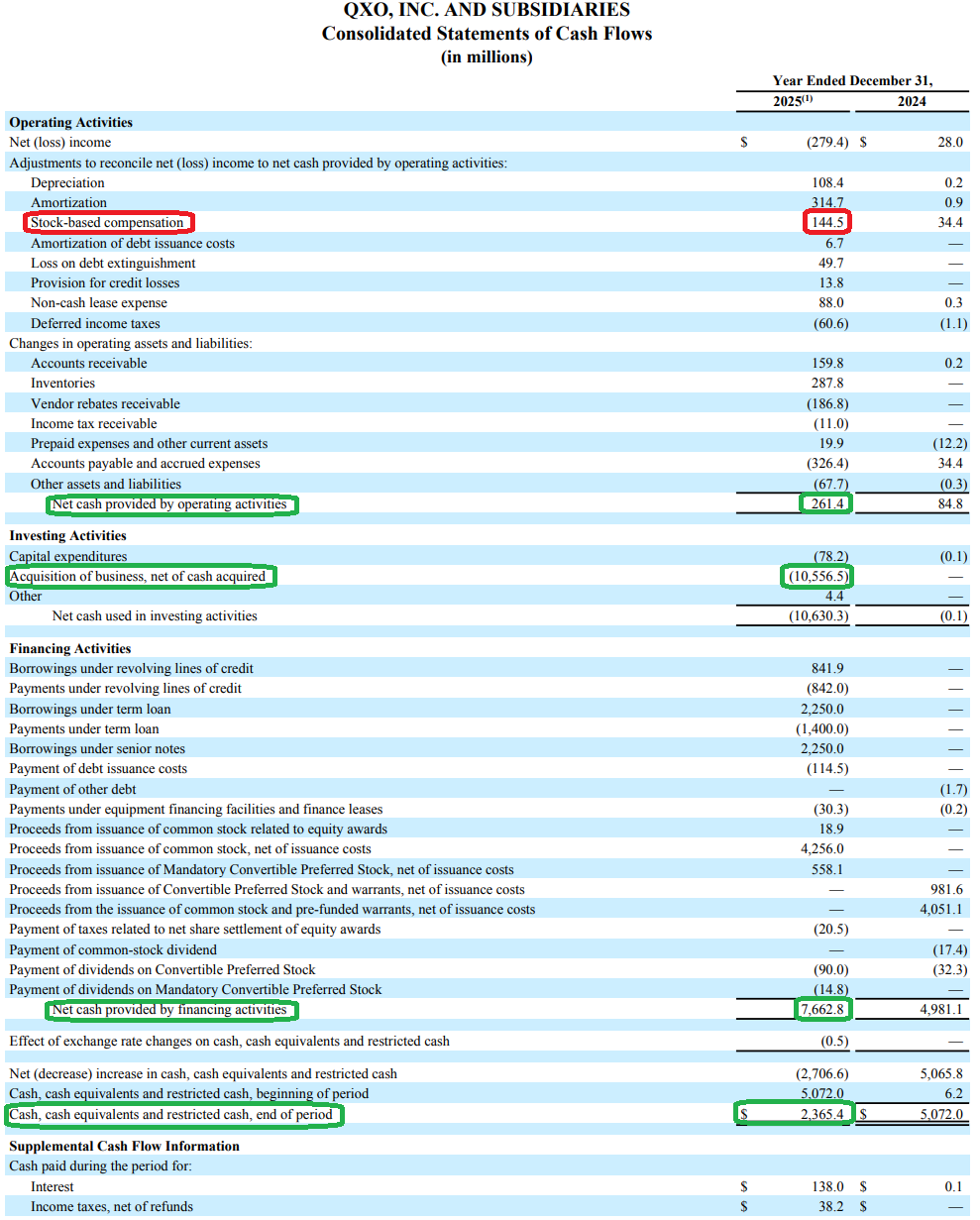

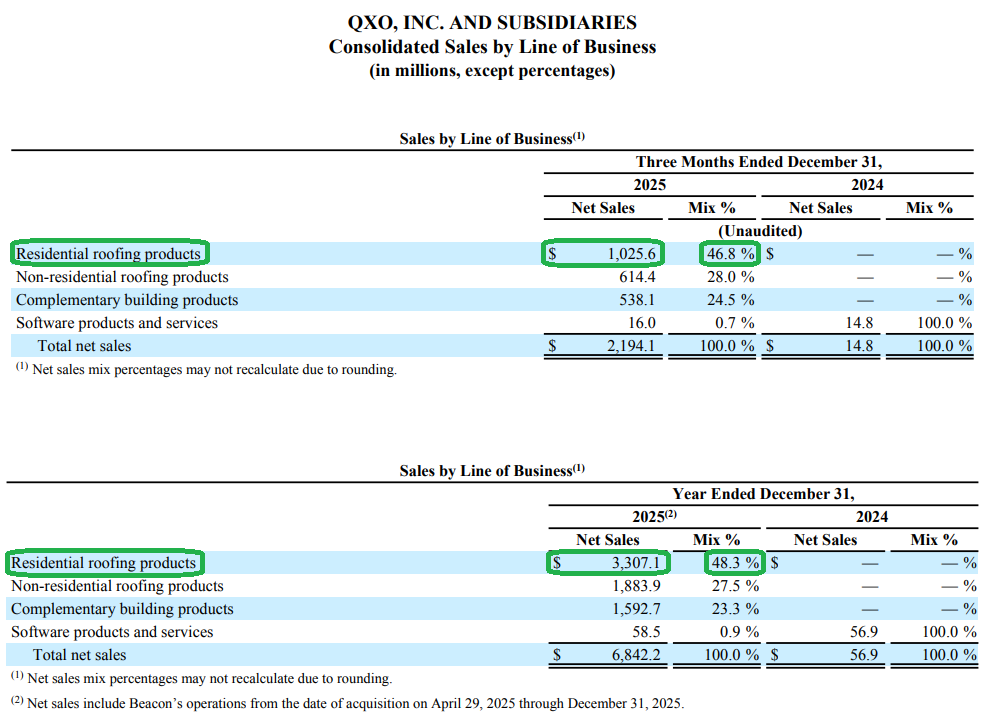

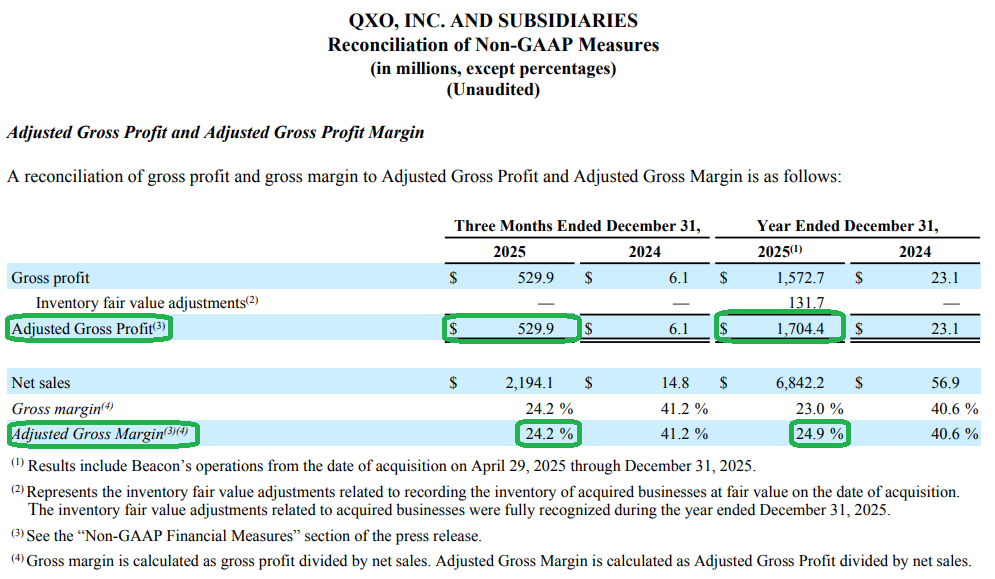

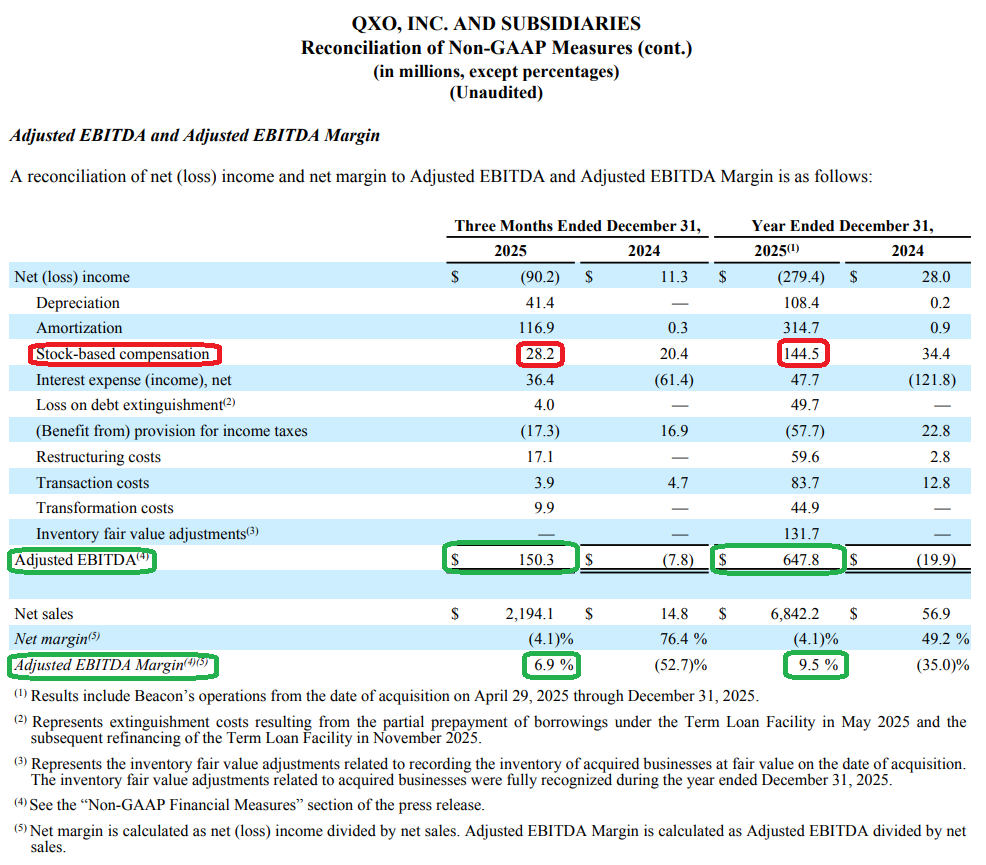

QXO’s fourth quarter results came with no surprises and landed right where expected, with preliminary figures released alongside the equity raise earlier this year. Net sales of $2.194B and adjusted EBITDA of $150.3M were essentially in line with pre-announced targets of $2.19B and ~$150M.

Near-term macro pressure on the U.S. housing market, driven by elevated rates and slowing activity, has weighed on shares of QXO, as one would expect for a leveraged housing recovery play. We continue to see this as largely noise. While QXO isn’t immune to market conditions, the real driver of the long-term thesis has nothing to do with any single quarter’s print and everything to do with disciplined M&A execution within the fragmented $800B building products distribution industry.

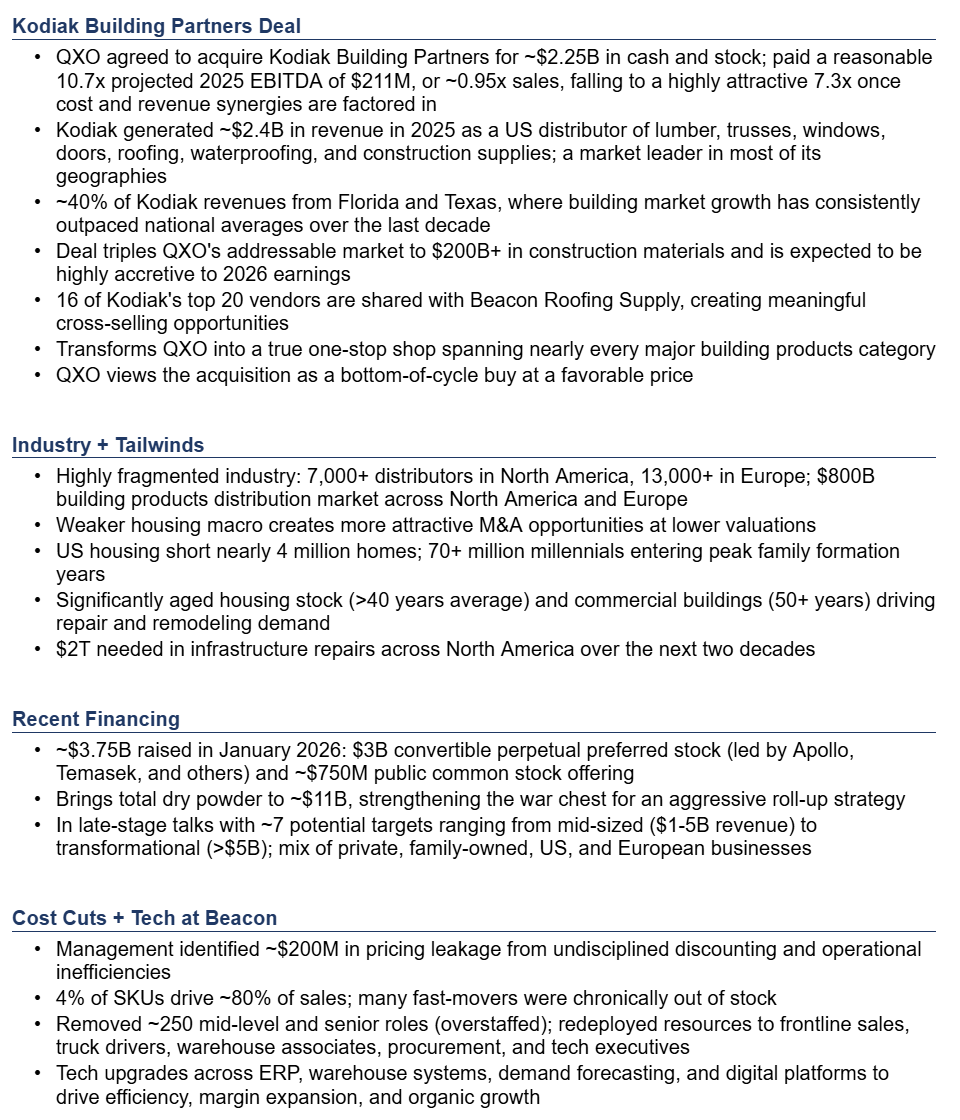

QXO is pursuing a large-scale consolidation strategy aimed at reaching $50B in annual revenue within a decade. With ~$10B on the board today, that leaves ~$40B in incremental revenue to be sourced through a mix of organic growth and, far more importantly, accretive M&A. The good news is that the longer housing stays under pressure, the more motivated and distressed sellers become, creating an attractive pipeline of high-quality assets available at trough valuations. That’s exactly where things stand today, with QXO leaning into the downturn and shopping from the industry clearance rack while the rest of the industry sits on the sidelines.

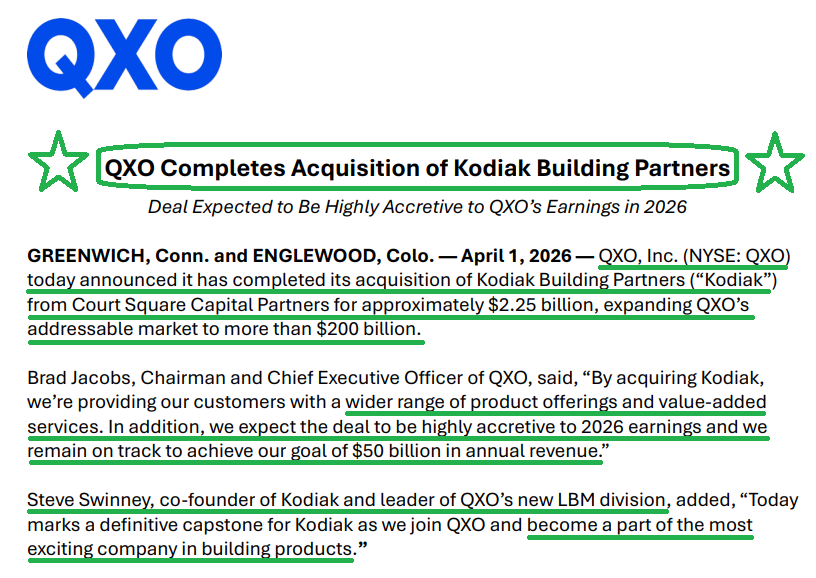

Against that backdrop, QXO closed its $2.25B acquisition of Kodiak Building Partners on April 1st, adding ~$2.4B of incremental revenue and marking the second major step in the roll-up strategy following last year’s $11B Beacon Roofing acquisition. QXO paid a reasonable 10.7x projected 2025 EBITDA of $211M, or ~0.95x sales, a multiple that falls to a highly attractive 7.3x once cost and revenue synergies are factored in.

Strategically, the Kodiak acquisition is a game changer. As a national distributor of lumber, engineered wood products, trusses, windows, doors, roofing, waterproofing, and other exterior products, Kodiak gives QXO a foot in the door to the lumber business, the first product in nearly every construction project. This entry point positions QXO as a true one-stop shop, covering almost every major building products category through a single, scaled national distribution platform. Post-close, QXO’s total addressable market expands more than threefold to $200B+, with greater exposure to structurally attractive markets such as Florida and Texas. These two states accounted for ~40% of Kodiak’s 2025 revenue and have consistently outpaced U.S. construction market growth over the past decade.

With the deal now closed, focus shifts to integration, realizing synergies, and the next acquisition. This is the same playbook Brad Jacobs has run throughout his entire career, spanning waste management, equipment rental, and logistics: consolidate fragmented, outdated industries using scale and technology, and create massive shareholder value in the process.

As the U.S. housing market emerges from what we continue to view as a cyclical trough, leveraged arms dealer plays like QXO stand to be among the cleanest beneficiaries. Until then, we’re more than happy to sit back and watch one of the greatest capital allocators of his generation go on a shopping spree at bottom-of-the-cycle prices.

Q4 Earnings Breakdown

GXO Update

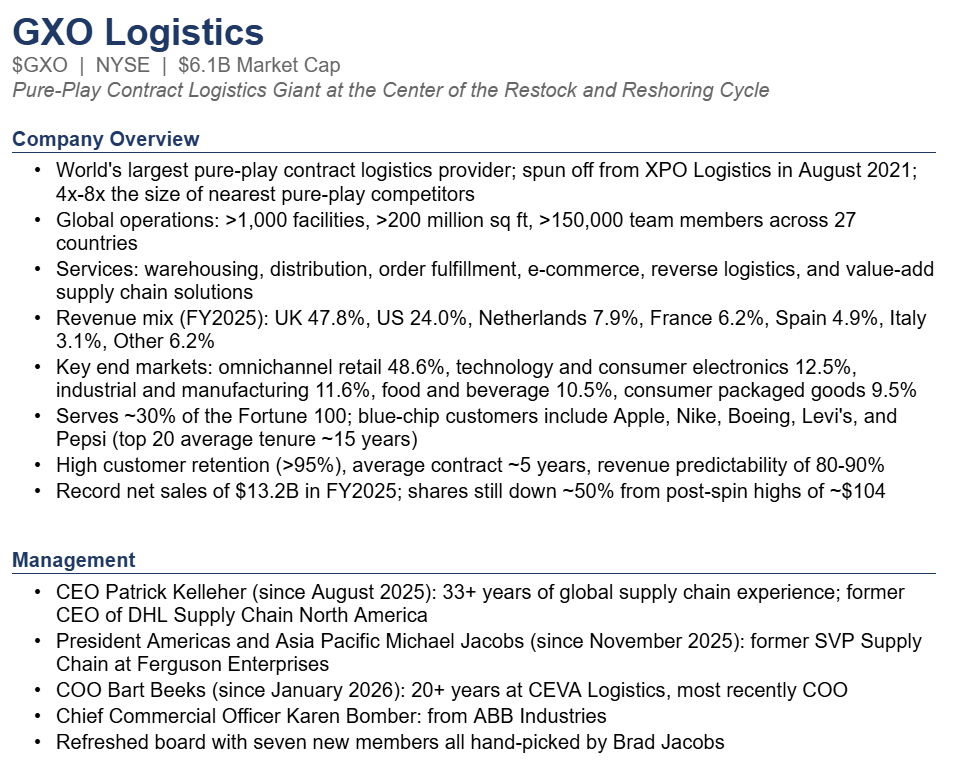

For newer readers, here’s a quick overview of the key drivers behind our thesis on GXO Logistics, the world’s largest pure-play contract logistics provider and one of the cleanest ways to play the restocking cycle against a backdrop of strong secular tailwinds:

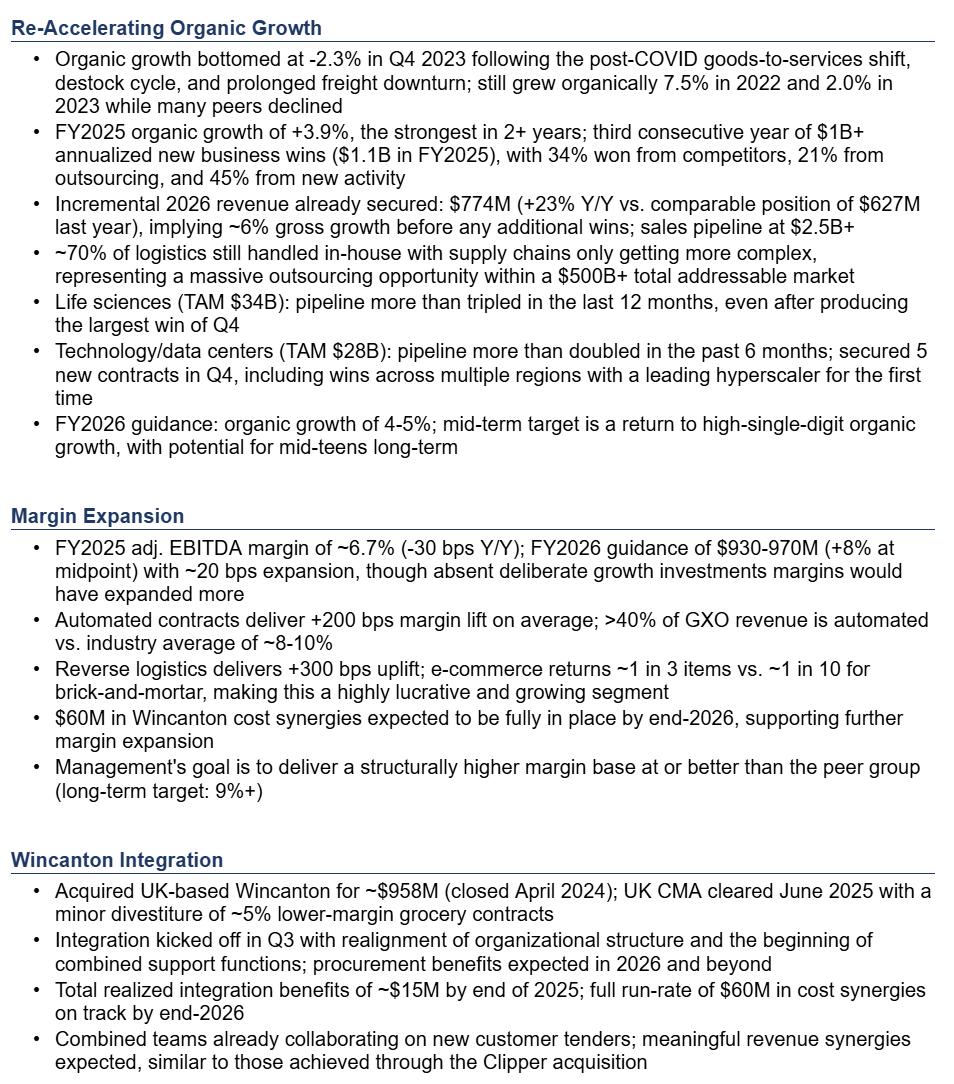

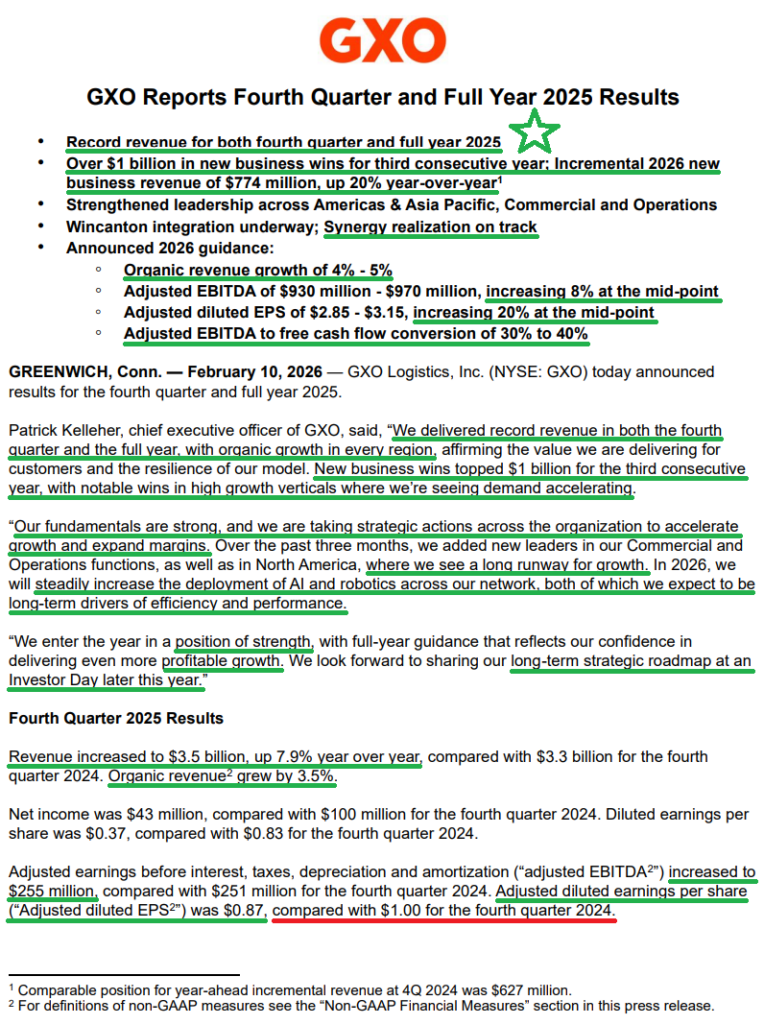

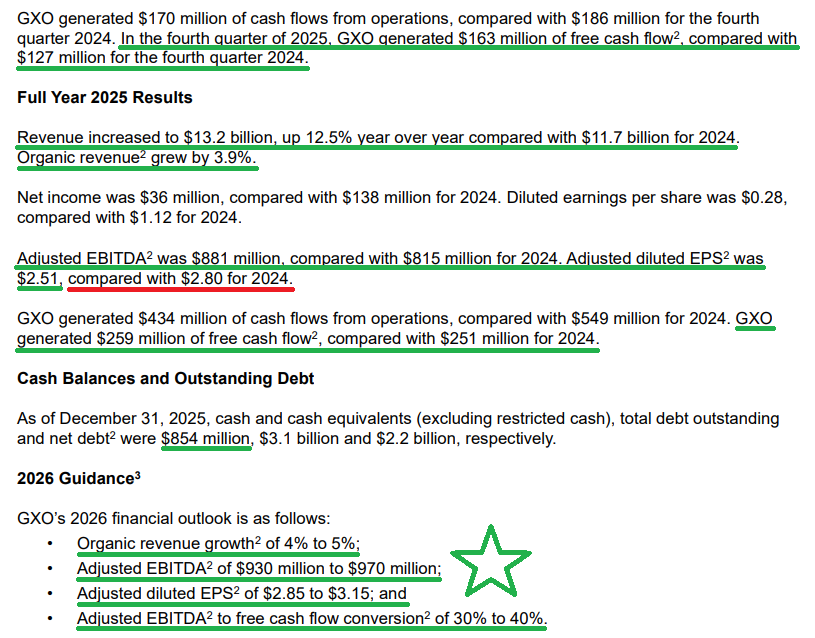

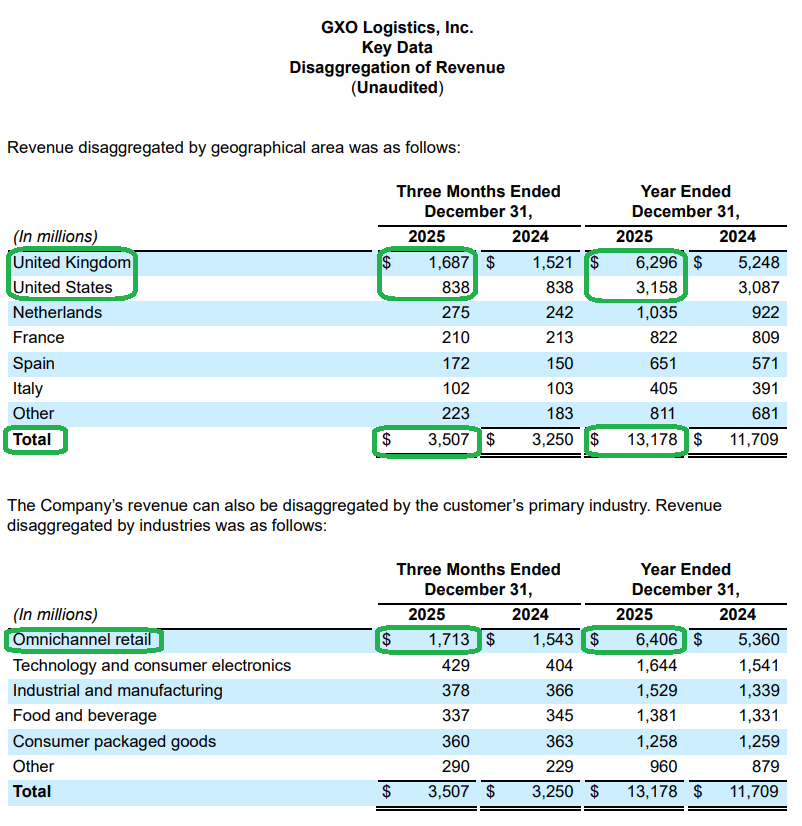

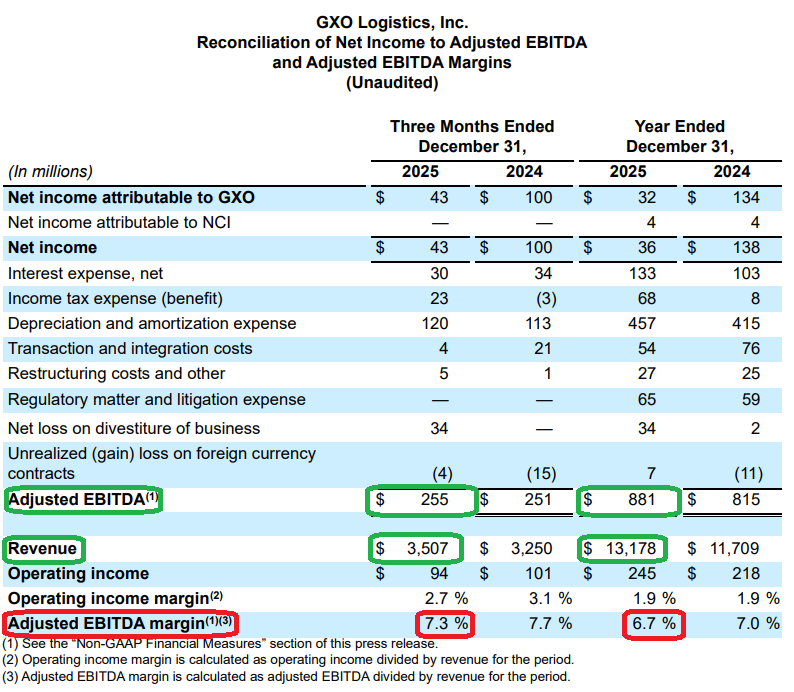

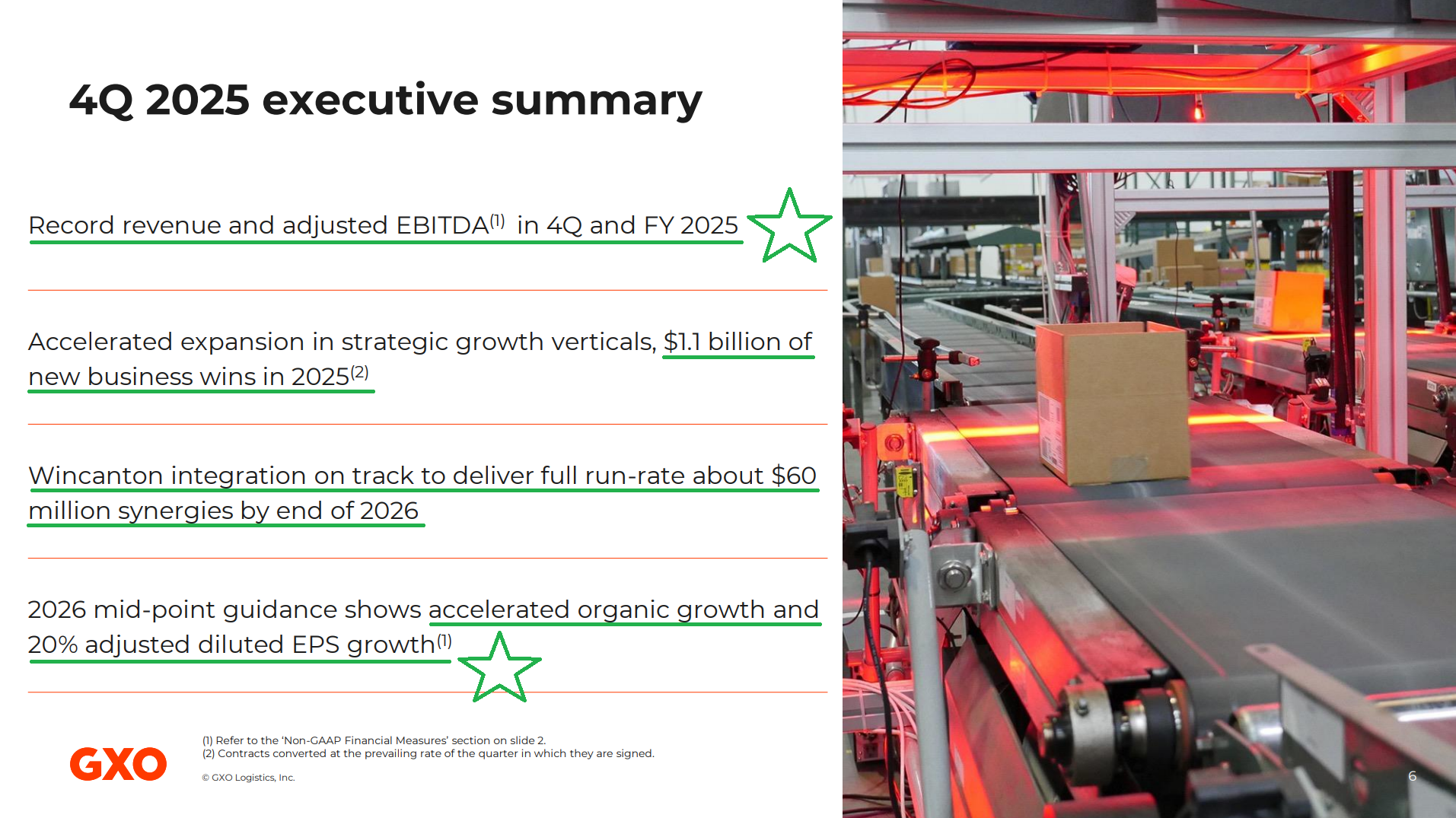

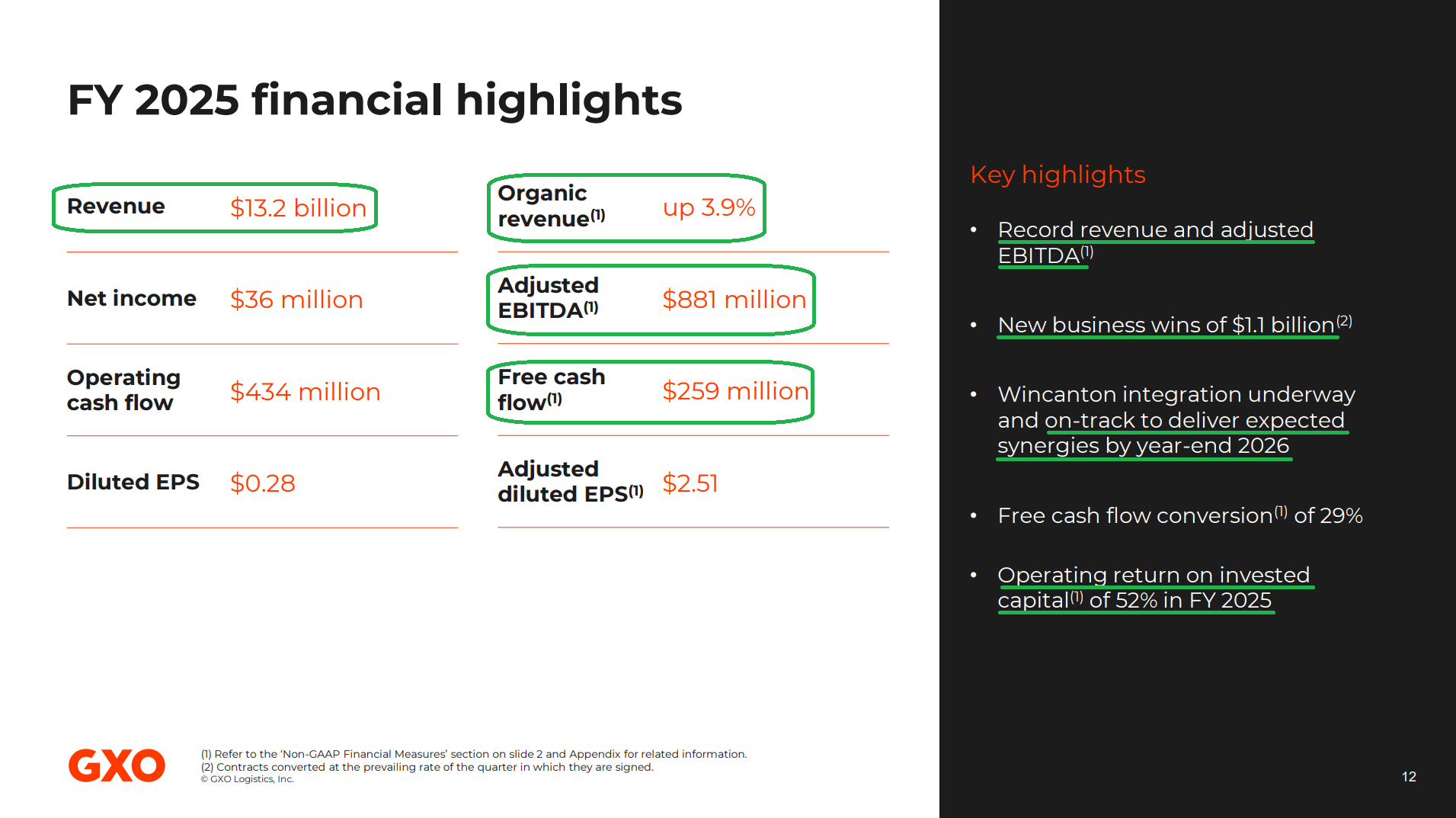

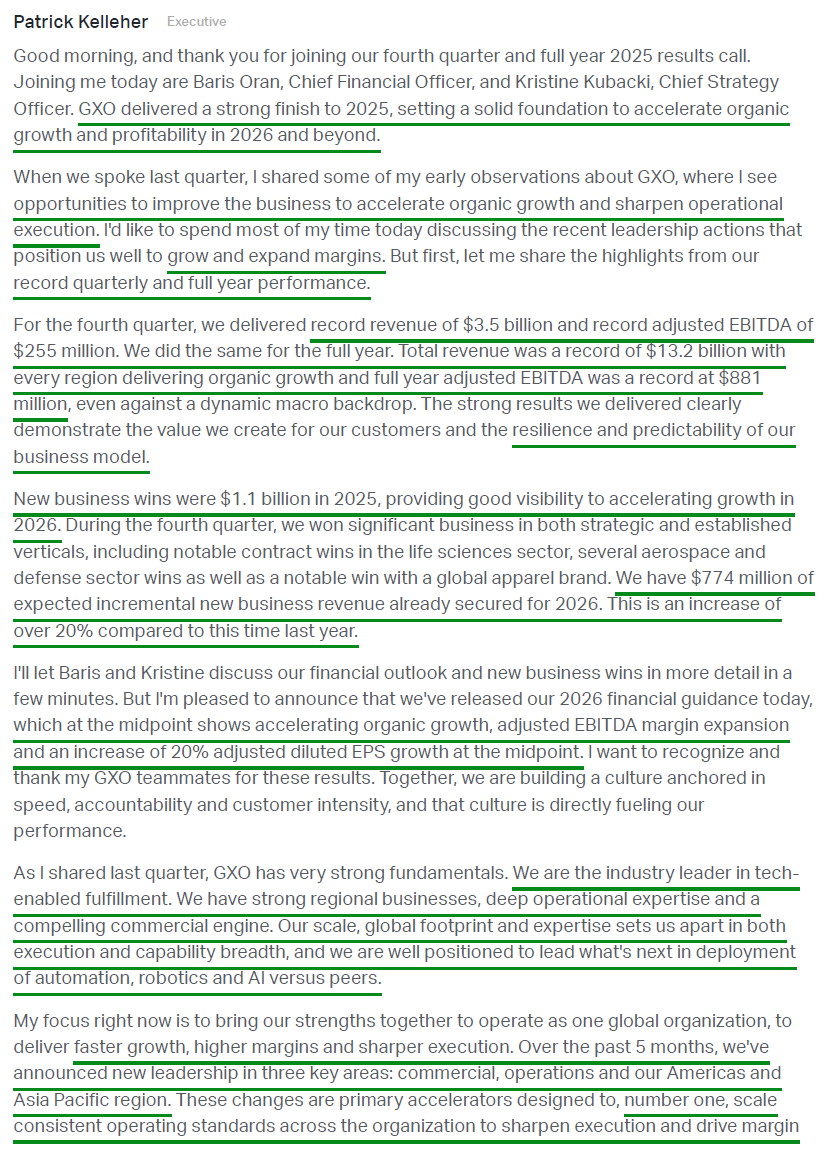

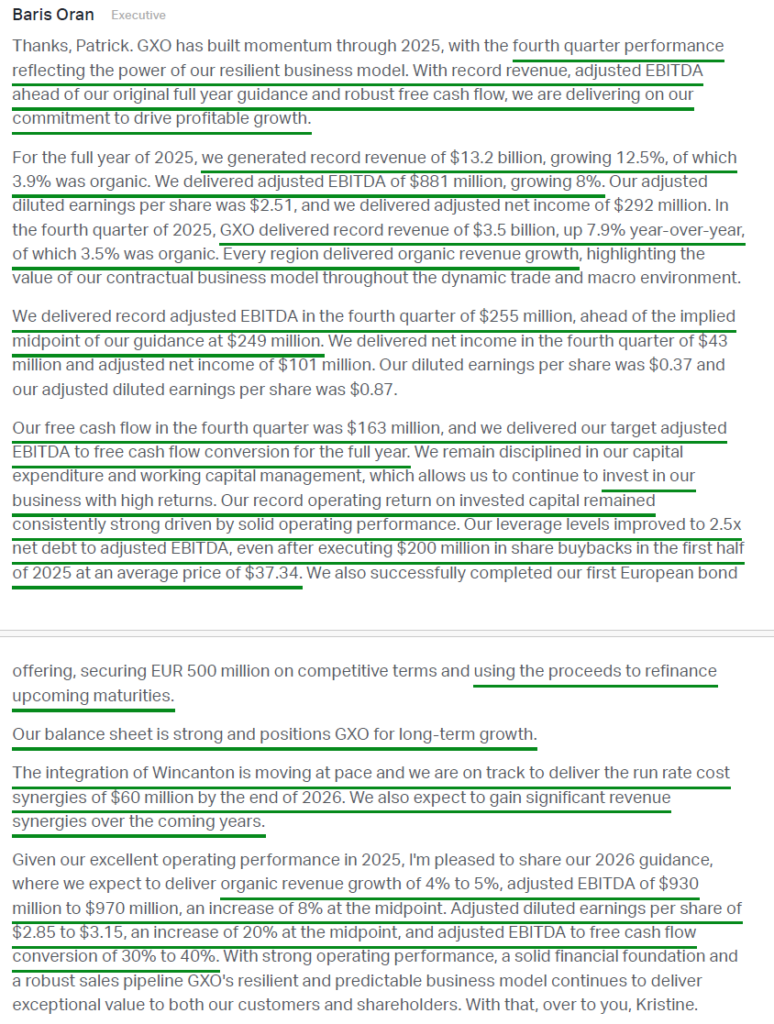

GXO closed out 2025 exactly the way you’d want a high-quality recovery story to finish the year. Revenue reached a record $13.18B (+12.5% Y/Y), organic growth accelerated to its highest rate in over two years at 3.9%, and adjusted EBITDA came in at a record $881M (+8.1% Y/Y). Every region contributed, with North America picking up the slack from softer volumes in Continental Europe and the UK, with 2025 also marking the third straight year of $1B+ in new contract wins. Most importantly, that momentum is carrying into 2026, with $774M of incremental new business revenue (+23% Y/Y) already secured before a single additional win is added to the board.

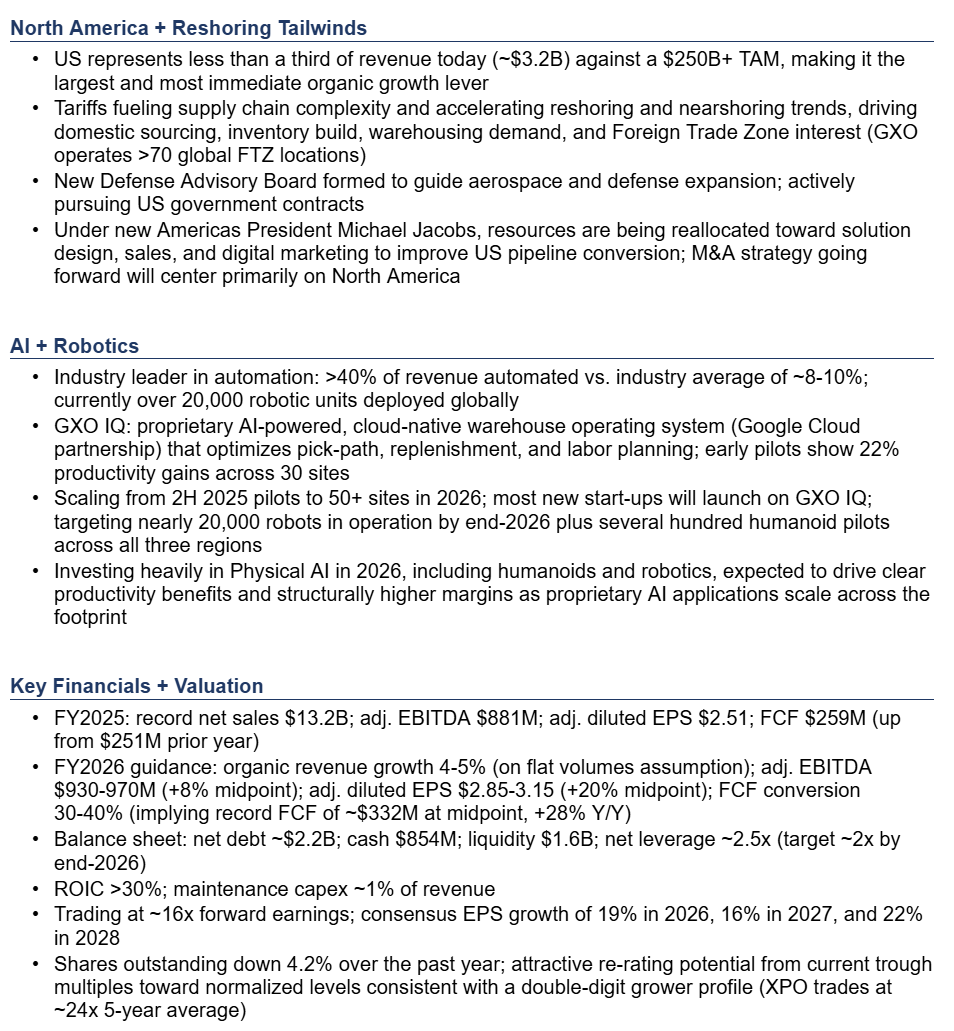

This was only Kelleher’s second full quarter in the seat, and we continue to be impressed by what we see. A 33-year supply chain veteran who ran DHL Supply Chain North America, he knows the U.S. opportunity better than anyone and is already moving aggressively to capture it, reallocating key resources and recruiting industry veteran Michael Jacobs to lead the region. With the U.S. representing less than a quarter of revenue ($3.2B) against a $250B+ TAM, the runway for expansion remains wide open and is still in the early innings.

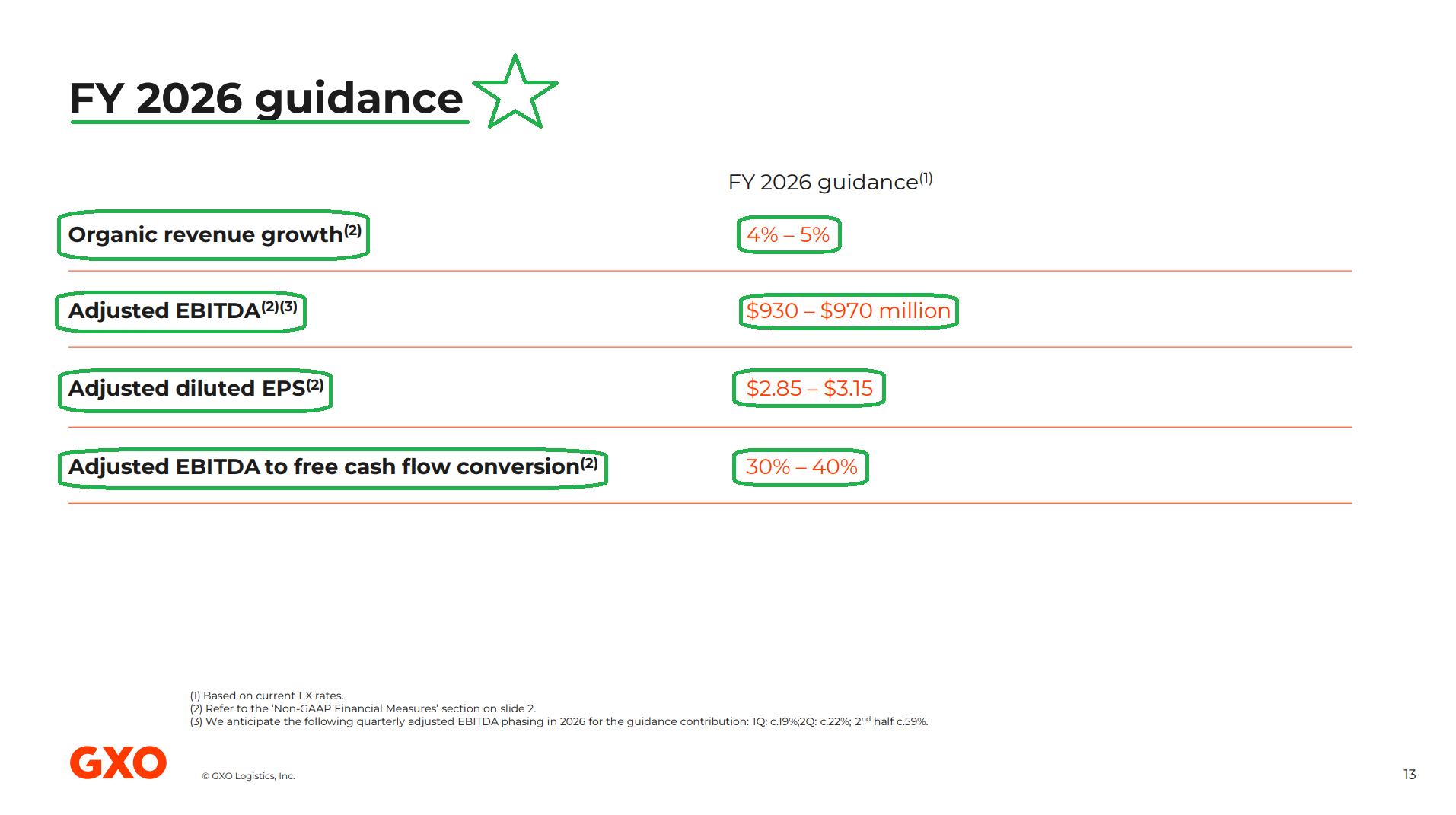

Pulling the North America organic growth lever sits at the center of 2026 guidance, which calls for 4-5% organic growth, implying a ~60 bps acceleration at the midpoint. While some may have hoped for a more aggressive step toward the long-awaited return to high single-digit organic growth, this was Kelleher’s first time setting guidance, and he kept a lid on expectations with numbers we view as highly conservative. With $774M of incremental revenue already booked, implying ~6% gross growth, and historical retention running at 95%+, GXO is effectively already tracking at the top end of its guidance range before a single additional win is factored in. On top of that, management’s explicit assumption bakes in flat customer volumes for the full year, an assumption Kelleher himself called conservative and nothing more than prudence. Any volume recovery from here is pure upside.

We see several catalysts that could drive that upside. Customer inventories in the U.S. remain depleted and are likely to normalize. Reshoring activity continues to accelerate, supporting incremental demand for warehouse capacity. At the same time, the pipeline across life sciences, defense, and technology is expanding rapidly. Together, these tailwinds signal the early stages of a volume recovery and inventory upcycle that remains largely underappreciated by the market.

Even against today’s muted assumptions, GXO is set to deliver 20% EPS growth and record free cash flow of $333M (+28% Y/Y), with a low bar for upside surprises.

A defensive growth compounder with an embedded option in automation, AI, and robotics, growing earnings 20%+ while still trading at a meaningful discount to the broader market. This is a setup we’re happy to own any day of the week. The next major catalyst is the investor day later this year, where Kelleher is expected to lay out the long-term strategic roadmap, the path to a structurally higher margin base, and what a return to strong organic growth truly looks like.

The upcycle is just getting started.

Q4 Earnings Breakdown

10 Key Points

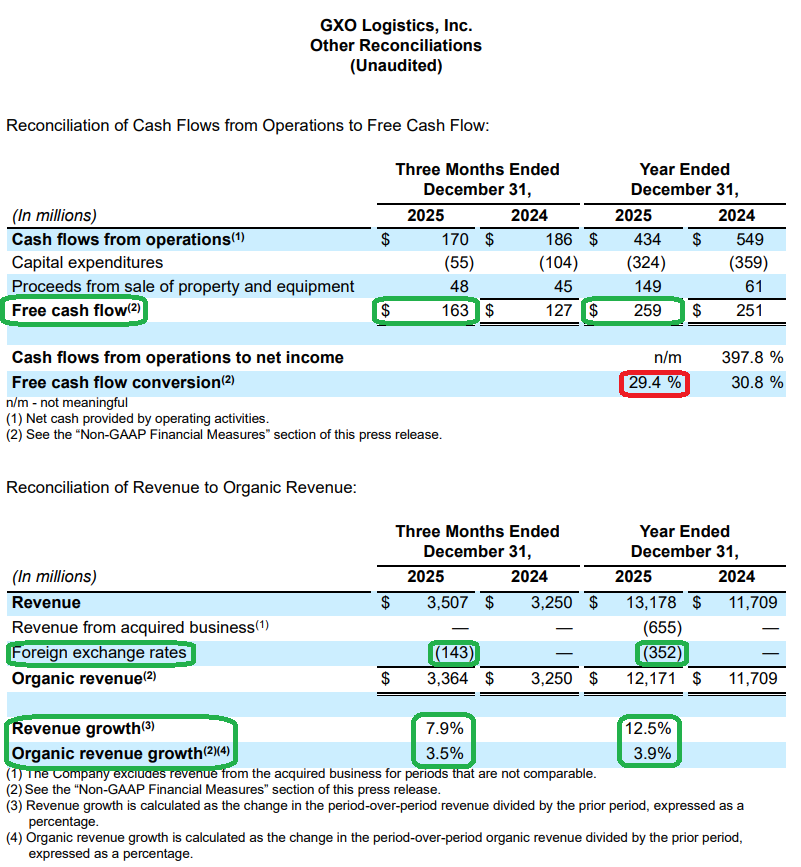

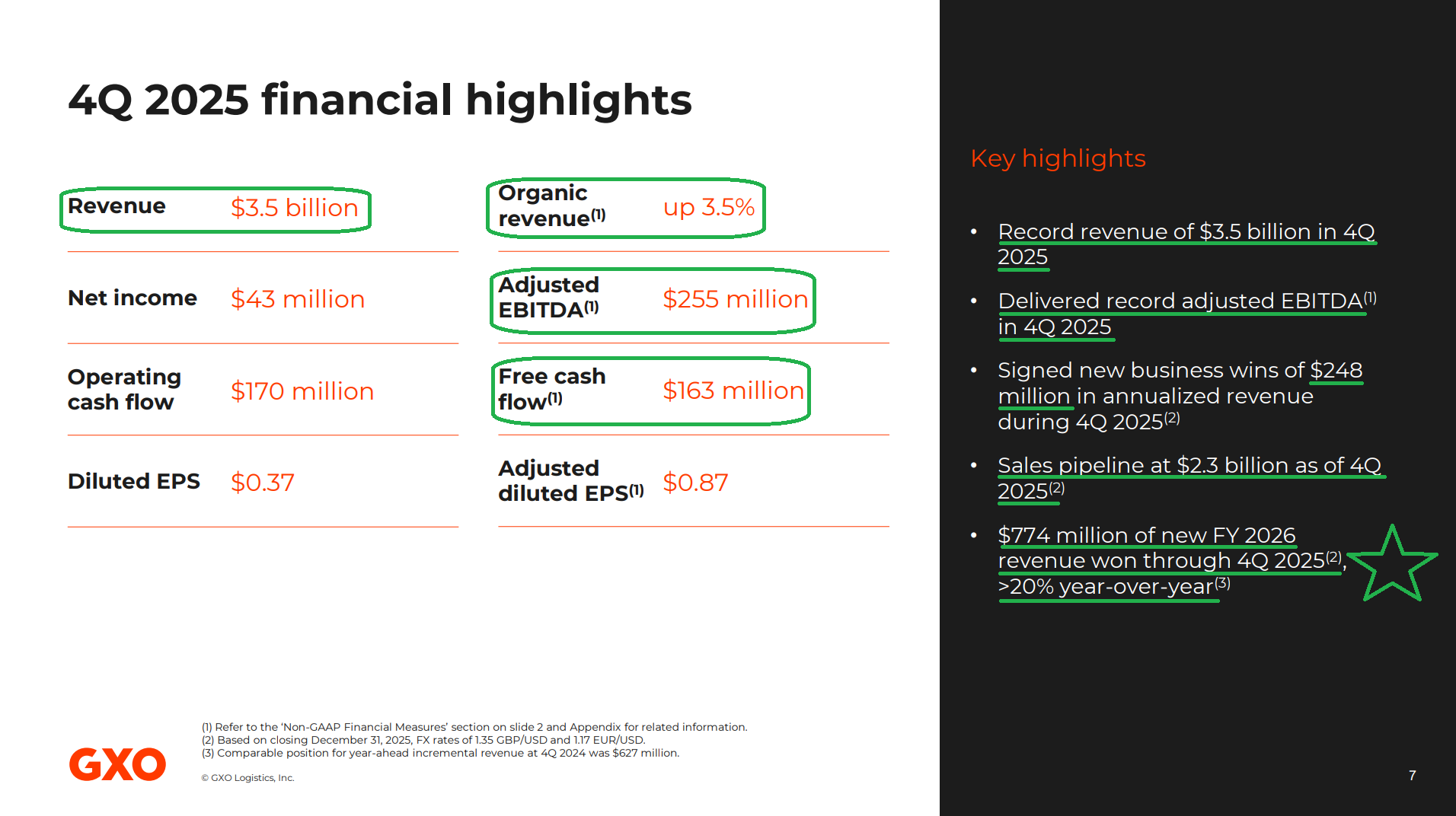

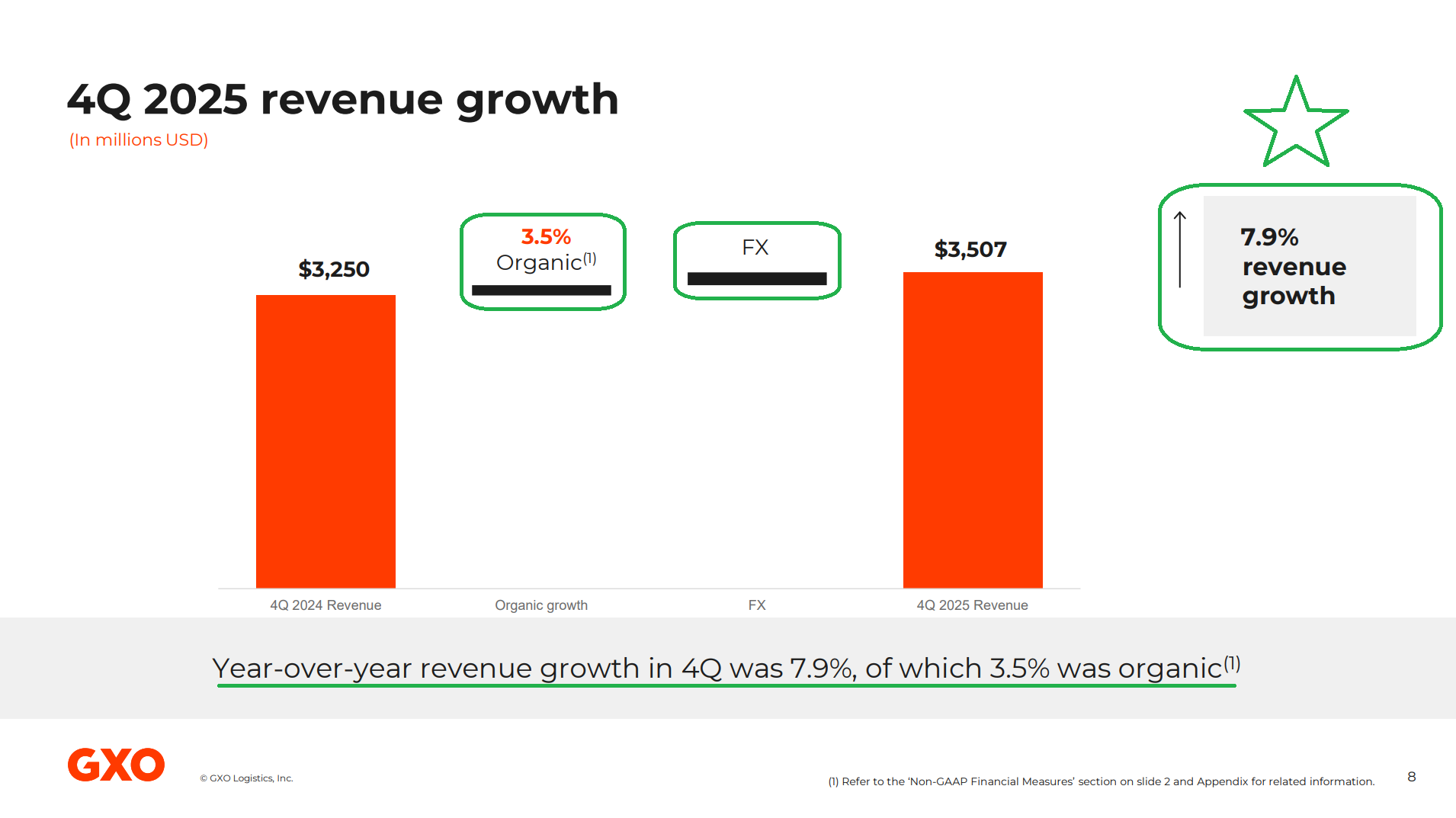

1) GXO posted record Q4 revenue of $3.51B (+7.9% Y/Y), beating consensus of $3.48B, with organic growth of +3.5% in the quarter. This brings full-year revenue to a record $13.18B (+12.5% Y/Y), of which 3.9% was organic, accelerating from FY24’s +2.5% and marking the highest organic growth rate in over two years. Q4 adjusted EPS came in at $0.87, beating consensus of $0.83 (-13% Y/Y), bringing full-year adjusted EPS to $2.51 (-10.4% Y/Y).

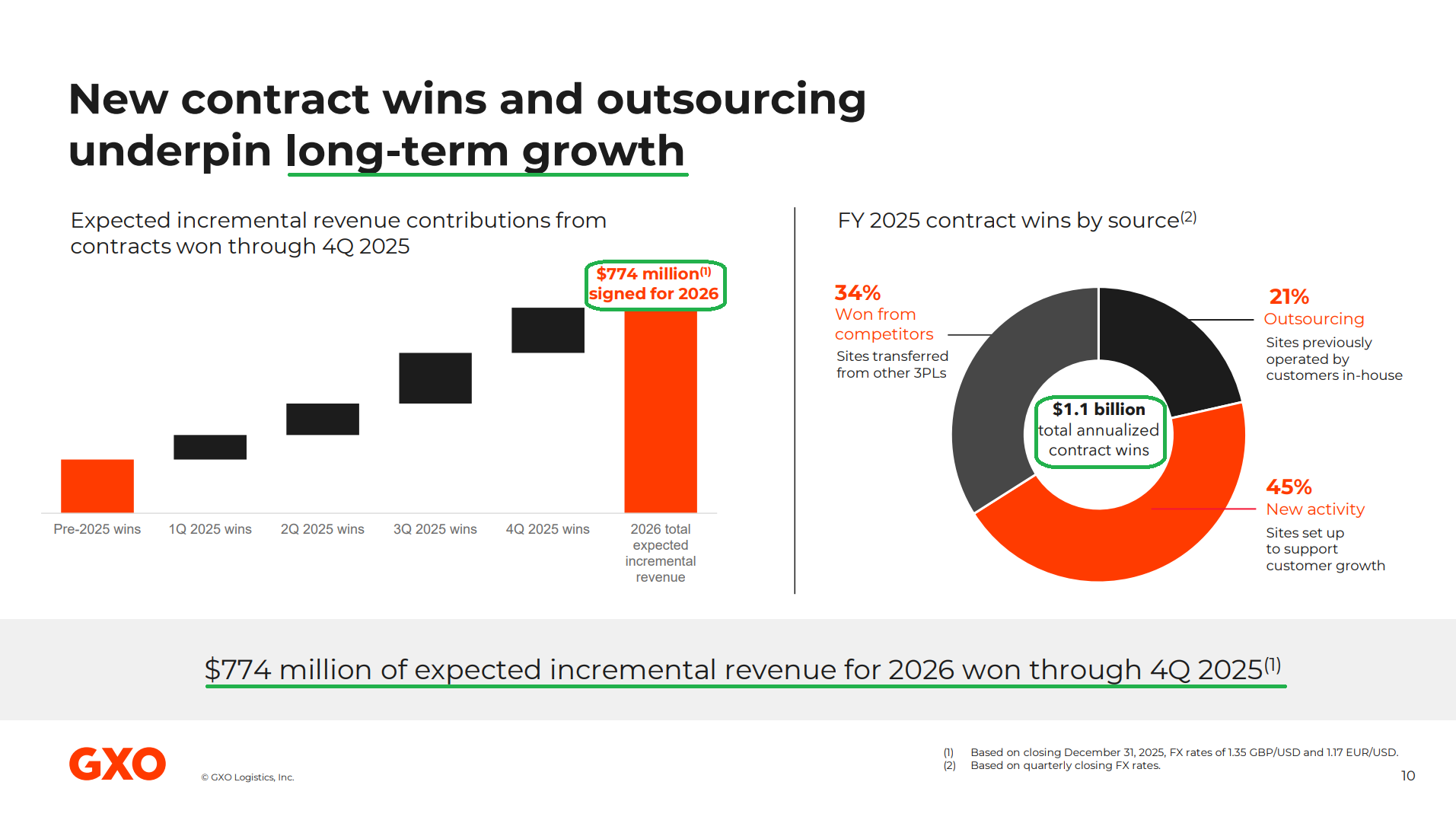

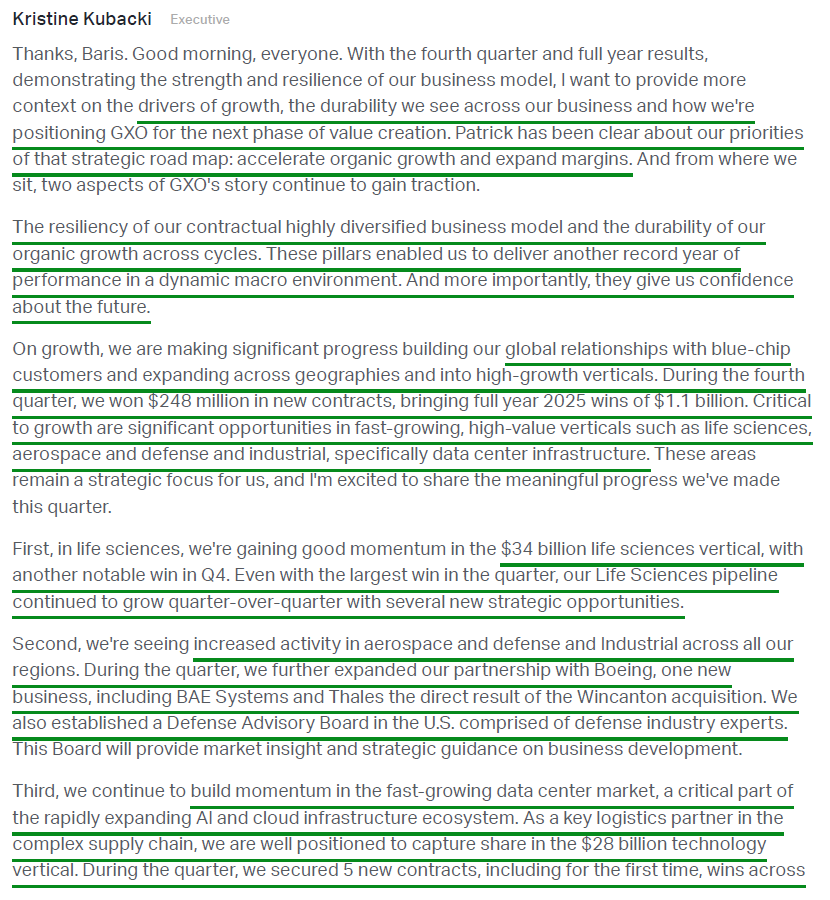

2) GXO won $248M in new contracts in Q4, bringing total annualized contract wins for FY25 to $1.1B and marking the third consecutive year of $1B+ wins. Of the $1.1B in total wins, 34% came from competitors, 21% from outsourcing, and 45% from new activity. Looking ahead, GXO has already secured $774M of expected incremental new business revenue for 2026, up 23% Y/Y versus the comparable position last year of $627M, implying ~6% gross growth before any additional wins.

3) The sales pipeline stood at $2.3B at the end of Q4 2025 and expanded to $2.5B by the time of the earnings call, with key verticals continuing to accelerate. Life sciences, a $34B TAM, has more than tripled over the past 12 months, even after delivering the largest win of the quarter. The technology vertical, a $28B TAM, has seen its pipeline more than double in the past six months, with GXO securing five new contracts in Q4, including multi-region wins with a leading hyperscaler for the first time. Aerospace and defense activity is accelerating across all regions, with GXO establishing a dedicated Defense Advisory Board in the U.S. to strengthen its business development efforts.

4) The Wincanton integration remains on track, having begun in Q3 with a realignment of the organizational structure and the integration of support functions, with procurement benefits expected in 2026 and beyond. Total realized integration benefits reached ~$15M by year-end 2025, with the full run-rate of $60M in cost synergies expected by the end of 2026. The combined GXO and Wincanton teams are already collaborating on new customer tenders, accelerating growth into target verticals. Management continues to expect meaningful revenue synergies over time, similar to those achieved through the Clipper acquisition, which drove the landmark NHS contract and GXO’s expansion into healthcare.

5) North America remains GXO’s largest and most immediate organic growth lever, representing less than a quarter of revenue today against a $250B contract logistics market with significant runway. Newly appointed North America leader Michael Jacobs, now three months into the role, is reallocating investments toward solution design, sales, and digital marketing to improve pipeline conversion and capitalize on the opportunity. Key growth drivers include reshoring activity, tariff-driven supply chain redesign, accelerating automation adoption, and above-GDP growth verticals such as aerospace and defense, technology, and life sciences. Going forward, M&A is expected to focus primarily on North America.

6) GXO is investing heavily in GXO IQ, its proprietary AI-powered warehouse operating system, which is already improving labor planning, inventory movement, forecasting, and workflow management across several of its largest sites. Early pilots in 2H 2025 showed measurable gains in proactive replenishment and slotting, with GXO IQ expected to scale to over 50 sites in 2026, covering ~4% of its 1,200 operations. GXO expects to have 20,000+ robots deployed globally by the end of 2026 and is piloting humanoid robots in live warehouse environments, with plans for several hundred pilots across all three regions. Management views physical AI, including humanoids and robotics, as a key driver of productivity gains and structurally higher margins over time.

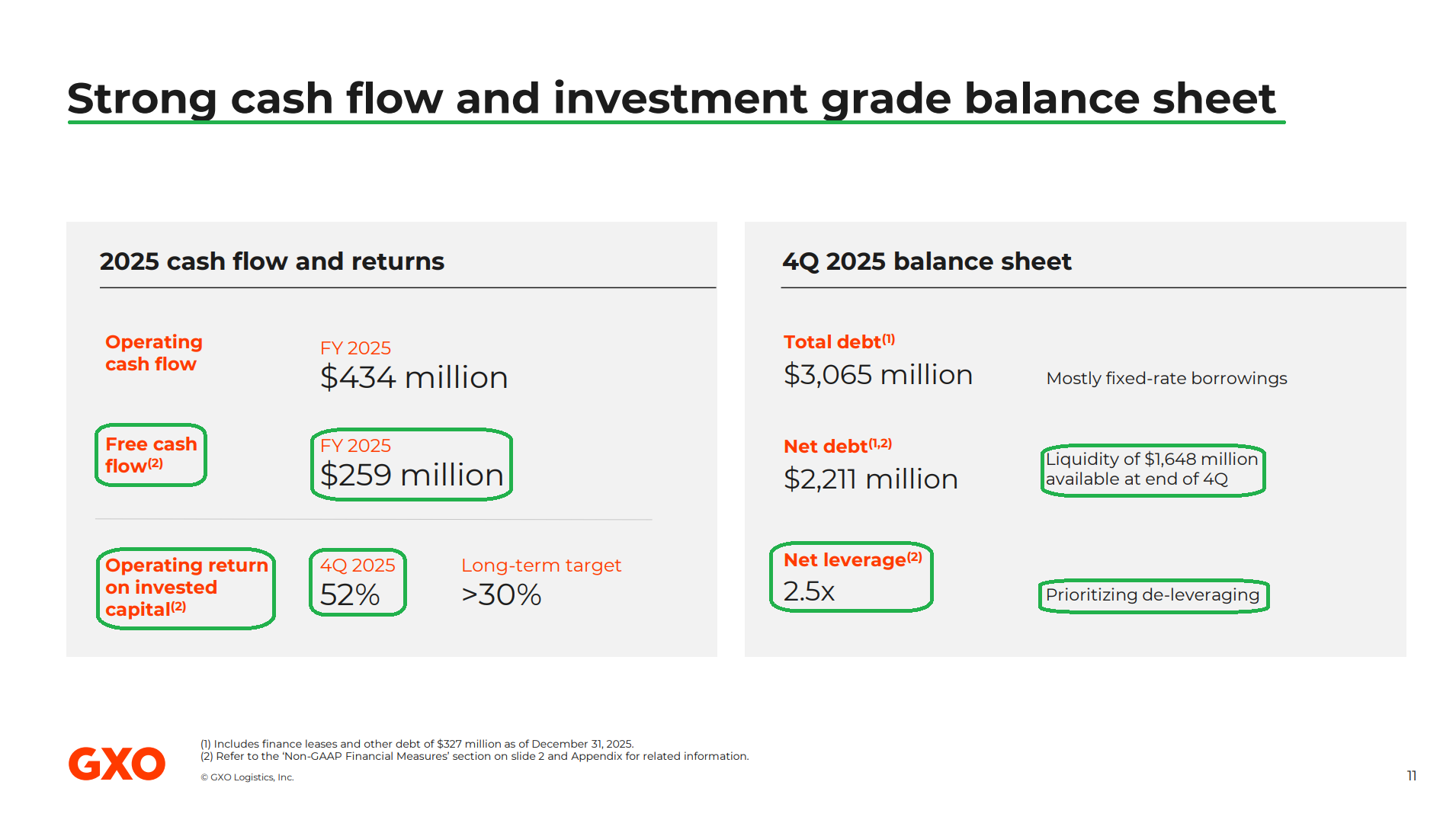

7) Q4 adjusted EBITDA came in at $255M versus $251M in the prior-year period, with margins of 7.3% versus 7.7%. This brings full-year adjusted EBITDA to a record $881M, ahead of both consensus (~$878M) and the prior guidance midpoint of $875M, with full-year margins of 6.7% versus 7.0% in FY24. Management expects ~20 bps of margin expansion in 2026, which would be higher absent deliberate growth investments. The goal remains a structurally higher margin base at or above the peer group, supported by Wincanton synergies, reverse logistics growth, and continued automation adoption.

8) Q4 free cash flow came in at $163M versus $127M in the prior-year period, bringing full-year FCF to $259M versus $251M last year. FCF conversion was 29.4% versus 30.8% in FY24. Looking ahead to 2026, management guided FCF conversion of 30–40%, implying record FCF of ~$332.5M at the midpoint, a 28.4% increase Y/Y.

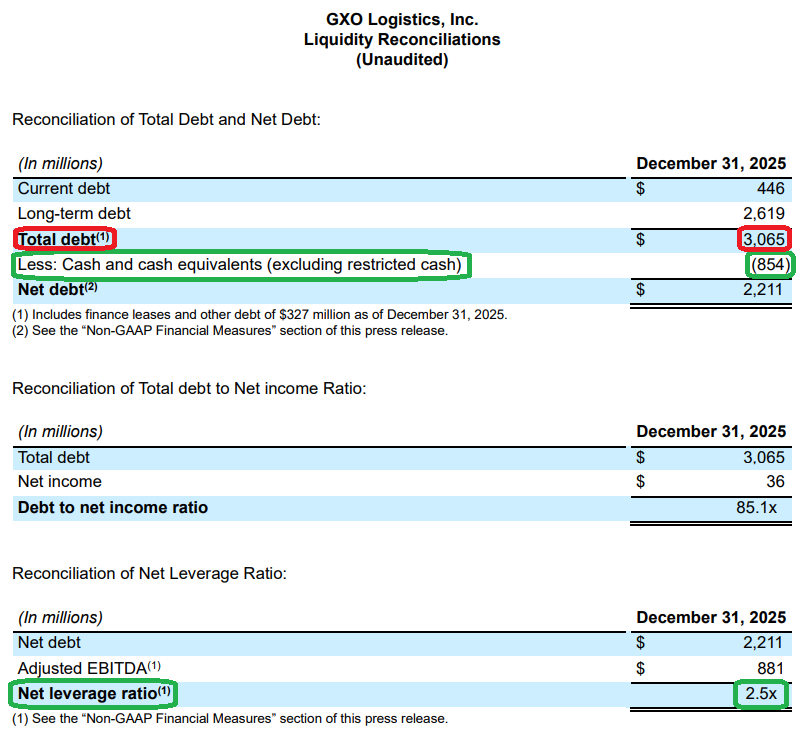

9) Net leverage improved to 2.5x, even after executing $200M in share buybacks during the first half of 2025 at an average price of $37.34. Cash stands at $854M, with total debt of $3.1B and total liquidity of $1.65B at quarter end. GXO completed its first European bond offering of EUR 500M, using proceeds to refinance upcoming maturities, and is targeting further deleveraging toward 2x by year end.

10) Management guided FY26 organic revenue growth of 4–5% (+60 bps acceleration at the midpoint versus FY25), adjusted EBITDA of $930–970M (+8% at midpoint), and adjusted diluted EPS of $2.85–$3.15 (+20% at midpoint), all in line with or ahead of consensus. Guidance assumes flat customer volumes in 2026, which management characterized as prudent and likely conservative given current inventory levels and activity.

Earnings Call Highlights

General Market

The CNN “Fear and Greed Index” ticked up to 28 this week from 14 last week. You can learn how this indicator is calculated and how it works here: (Video Explanation)

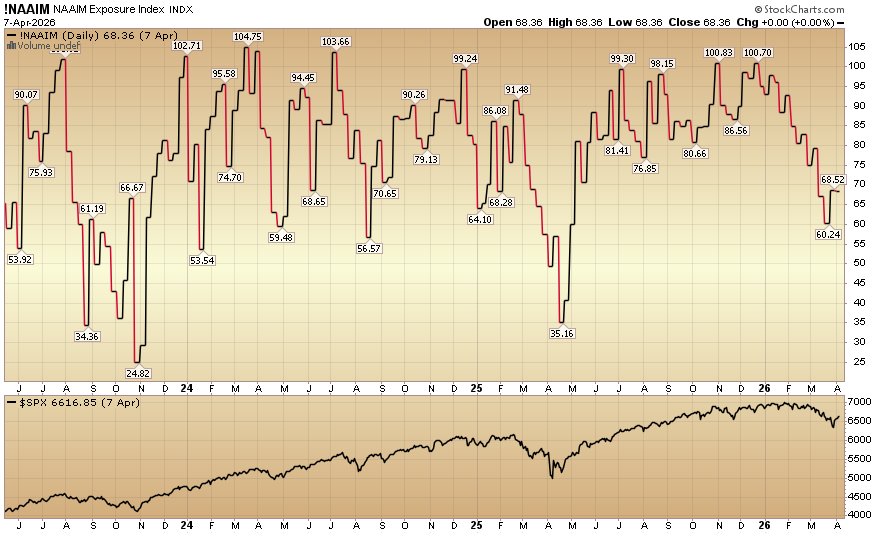

The NAAIM (National Association of Active Investment Managers Index) (Video Explanation) fell to 68.36% equity exposure this week from last week’s 68.52%.

Our podcast|videocast will be out sometime today. We have a lot of great data to cover this week. Each week, we have a segment called “Ask Me Anything (AMA)” where we answer questions sent in by our audience. If you have a question for this week’s episode, please send it in at the contact form here.

Congratulations to all of the new clients that came in intra-quarter (Q1) with larger sized accounts, and to those existing clients who upsized their contributions to their accounts.

We are officially open to smaller accounts $1M+. The opening will close on April 10th at 5PM Eastern.

To see if you qualify and to take advantage of this opening click here, or go to GreatHillCapital.com for more details.

Larger accounts $5-10M+ can access bespoke service anytime here.

Not a solicitation.

*Opinion, Not Advice. See Terms