The December survey covered 371 managers with $1.1 trillion in assets under management.

OUTLOOK:

-Sees Crypto, Unprofitable Tech, Banks, EM Rallying If December Fomc Outcome Is Dovish.

-Only 36% Think Inflation Is Permanent And 55% Think It Is Transitory. A net 36% of those polled said inflation was permanent.

-Inflation jitters continued to wane in December, with a net 33% of investors looking for lower global CPI in the coming 12 months.

-Last month, a net 14% looked for lower global CPI and in October, a net 1% looked for lower global CPI. This remains in sharp contrast to April and March, when a record 93% of those polled looked for higher inflation.

-With regard to Fed rate hikes for 2022, in December 49% of managers looked for two increases, 23% said one increase, 17% said three increases, 6% said no increases and 2% said four increases. Last month, 39% of managers looked for two increases, 37% said one increase, 13% said no increases, 8% said three increases and 1% said four increases.

-Investors expected Fed tapering to finish by April 2022.

SENTIMENT:

-A net four percent of those polled in December looked for stronger world economic growth in the coming year, versus a net three percent with that view in November and compared to October, when a net six percent looked for weaker growth.

-In March 2021, a net 91% looked for stronger world growth.

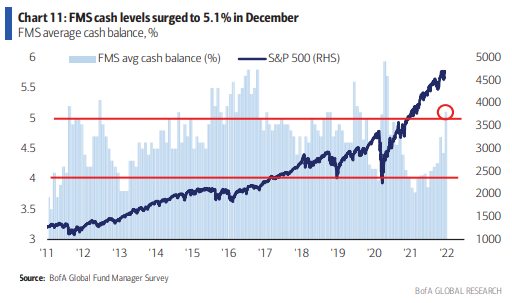

-“Investors [are] very cautious but few [are] outright bearish,” Bank of America said.

-Only six out of 100 investors believed that a recession would occur in the next 12 months.

POSITIONING:

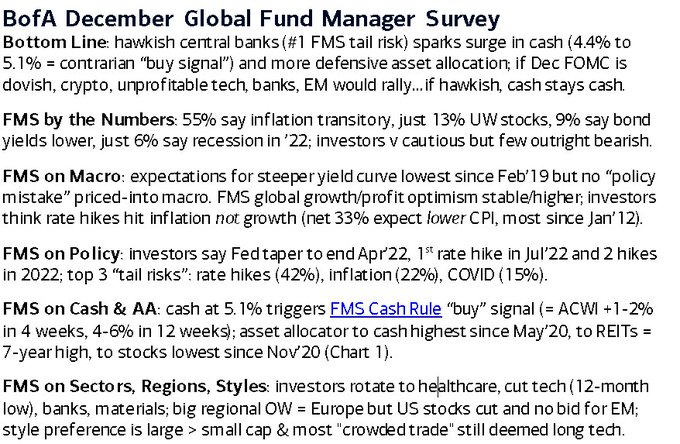

-Allocation to cash highest since May 2020.

-Fund managers were net 36% overweight cash.

-Holdings in real estate investment trusts reached a seven-year high.

-The rise in cash holdings triggered the “FMS Cash Rule tactical ‘Buy’ signal,” which suggests global equity returns of +1.3% in one month, +4.0% in 3 months and +6.5% in 6 months, the survey said.

-A net 46% of portfolio managers were overweight global equities in December, compared to a net 58% in November and a net 50% in October.

-This month, a net 63% of managers were underweight bonds, compared to a net 69% underweight in November and a net 80% underweight in October, which was the largest bond underweight ever.

-Global investor allocation to commodities fell to a net 19% overweight in December from a net 26% overweight in November and a net 28% overweight in October.

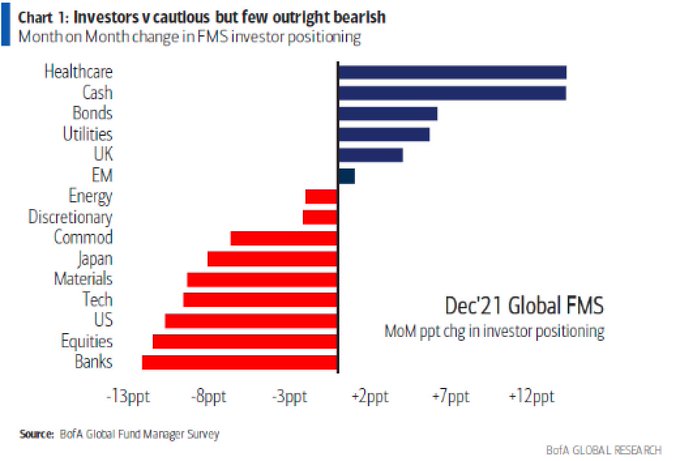

-Allocation to U.S. stocks fell to a net 18% overweight from a net 29% overweight in November, which was the highest level since August 2013. Allocation stood at a net 16% overweight in October.

-This month, a net 31% of managers were overweight eurozone stocks, compared to a net 33% overweight in November and a net 34% overweight in October.

-Fund managers added to their global emerging market (GEM) stock holdings, with investors having a net one percent underweight in December, little changed from a net two percent underweight in November and compared to a net five percent underweight in October. Current levels are well down from the record net 62% overweight seen in January 2021.

-Portfolio managers had a net two percent underweight to Japanese equity markets this month, compared to a net seven percent overweight in November and October.

-UK equity allocations showed managers with a net 11% underweight in December, compared to a net 15% underweight in November and a net 12% underweight in October.

MOST CROWDED TRADES:

1. Long Tech Stocks (39%)

2. Long Bitcoin (18%)

3. Long ESG (17%)

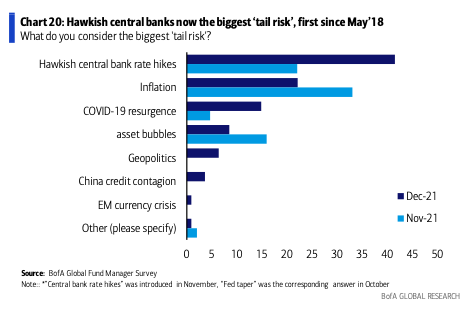

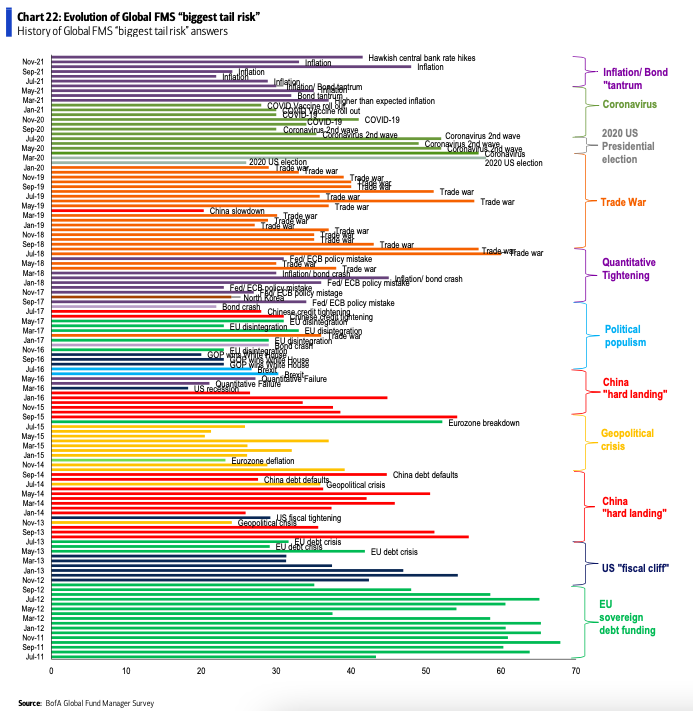

BIGGEST TAIL RISKS:

1. Hawkish Central Bamk Rate Hikes (42%).

2. Inflation (22%).

3. COVID-19 resurgence (15%).

BANK OF AMERICA COMMENTARY: