I never thought I would utter the four words from this title, but as the saying goes, “if you live long enough…”

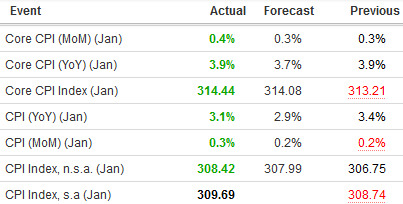

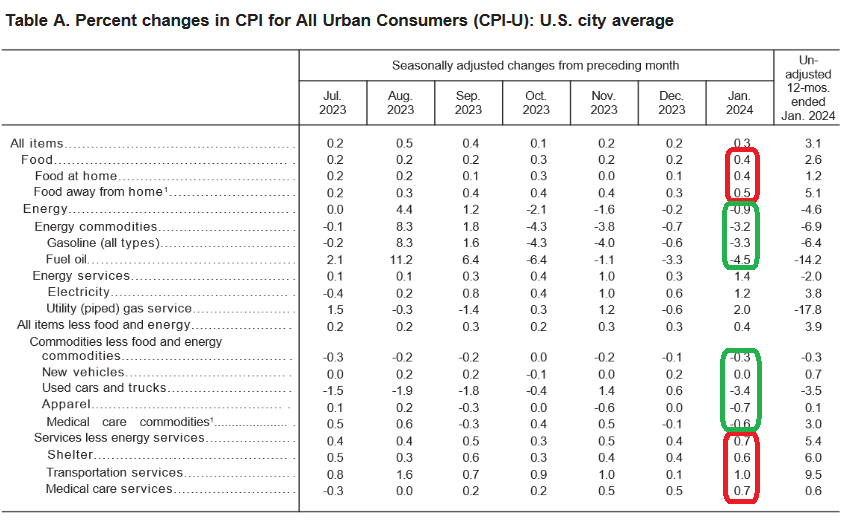

We came into the CPI report with expectations of a beat (inflation coming in lower than expected). Our view was predicated on a big step-up in non-seasonally adjusted CPI index basis from Dec 2022 (296.80 to 299.17) to Jan 2023. Energy and used cars dropped as anticipated, but food and shelter remained stubborn (or did it)?

The average monthly price change of the last 12 months (unadjusted) was ~0.23%. If this persists through March, we could see headline below 2.5%.

The average monthly price change of the last 12 months (unadjusted) was ~0.23%. If this persists through March, we could see headline below 2.5%.

While this did not prove to play out as anticipated (this month) there were a few reasons why – which the market ultimately re-calibrated to understand on Wednesday:

The Chicago Reserve Bank President Austan Goolsbee came out with this dovish take/clarification for markets:

Core Inflation 12-month change was 3.88% – which was the lowest of this cycle and 10th consecutive decline. Headline was 3.09% (the lowest of the last 7 months).

As Goolsbee so eloquently stated at his CFR appearance on Wednesday morning, “don’t get flipped out over yesterday!”

As I’ve emphasized every week in the podcast|videocast, real rates (FFR – inflation) are excessively restrictive. Goolsbee called real rates “very high” in his speech. He also acknowledged that if this situation persists (Fed’s restrictive posture), the current “problem” of inflation can quickly pivot to a “serious problem” of unemployment. I’ve gone further to state “deflation” is a greater risk than inflation if this level of restriction persists. When it turns, it can turn on a dime. It is comforting to see there is a member fully cognizant and vocal of this risk and publicly holding the FOMC accountable if they miss it/mess it up.

For clarification, he brought up the FOMC summary of economic projections from December – which stated that they believed inflation would be at 2.4% in 2024 and they would cut 3x. He then was explicit that their favored measure PCE inflation was already LOWER than that target of 2.4% both on a 3 and 6 month annualized rate. Uber-dovish…

To close it out and put market participants at ease, Goolsbee emphasized the importance of productivity gains we are now seeing by stating that “nothing is more important.” Furthermore, “it will definitely change the way we think about the economy.” In other words, when you have productivity growth, wages can rise to the level of prices yielding above-trend growth (while simultaneously low inflation).

“I don’t support waiting until inflation, on a 12-month basis, has already achieved 2% to begin to cut rates,” he said.

And with that, markets bounced off the danger zone yet again:

Sentiment and Positioning

This Tuesday, Bank of America published its monthly “Fund Manager Survey.” I posted a summary here:

February 2024 Bank of America Global Fund Manager Survey Results (Summary)

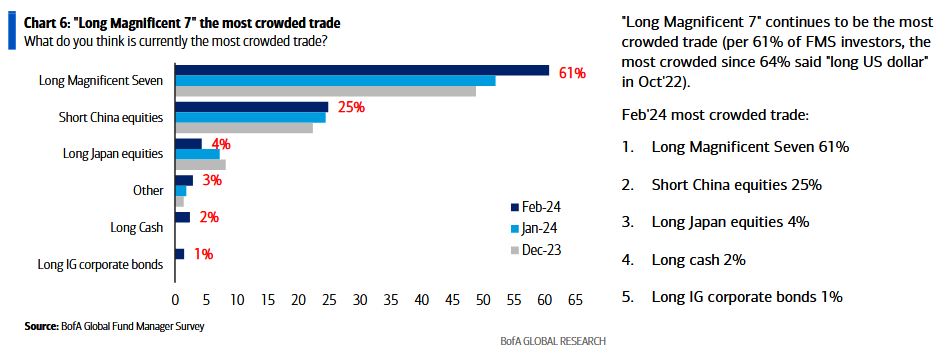

Here were the 3 key points:

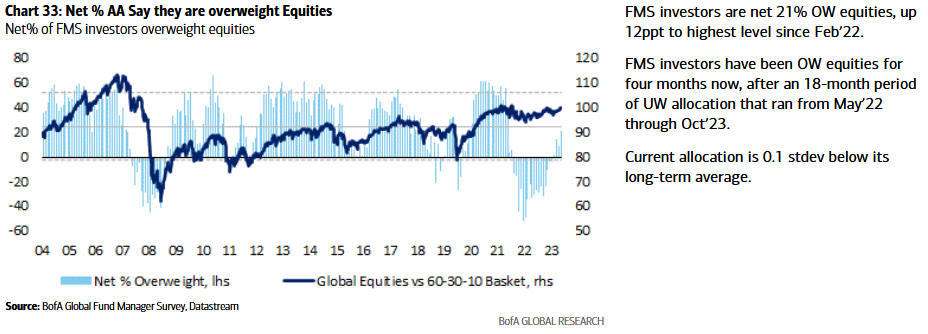

1) Fund managers are still 0.1 stdev BELOW their long-term average allocation to equities:

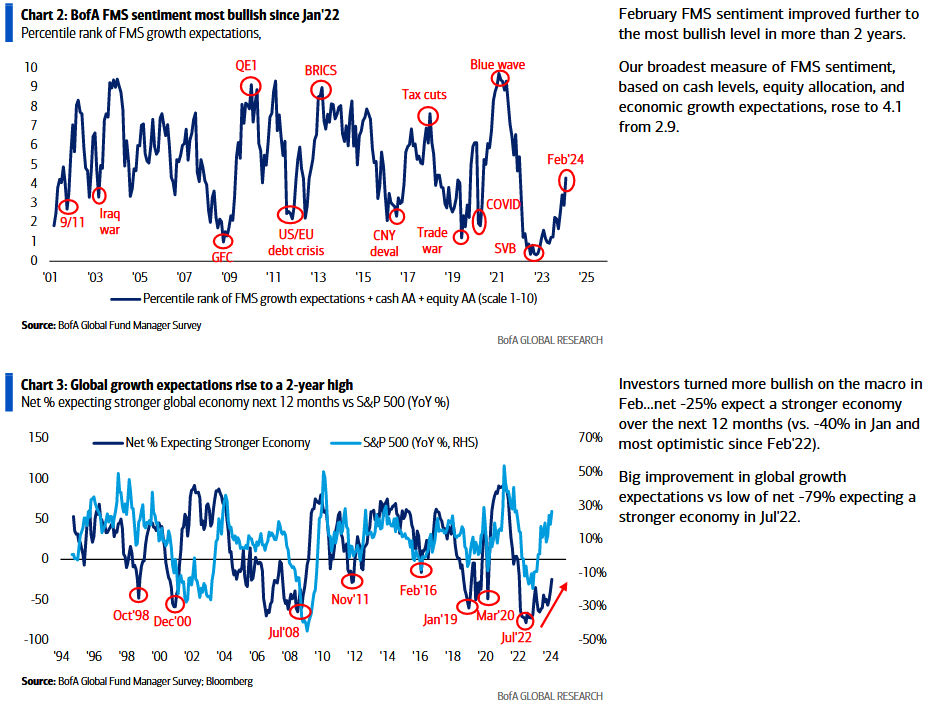

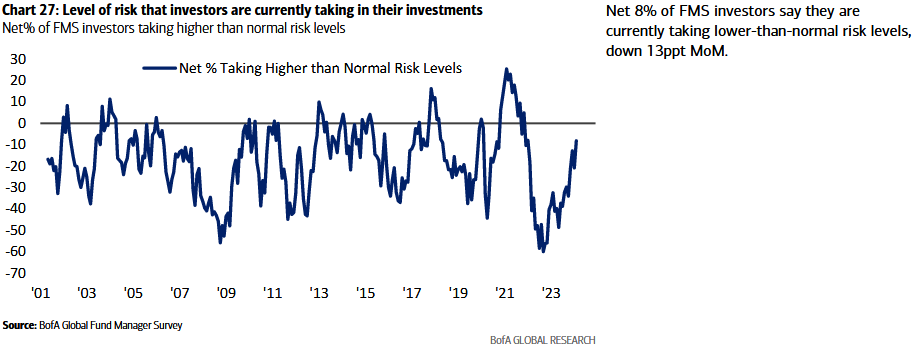

2) Managers sentiment and risk propensity (while improving) is not at/near an extreme:

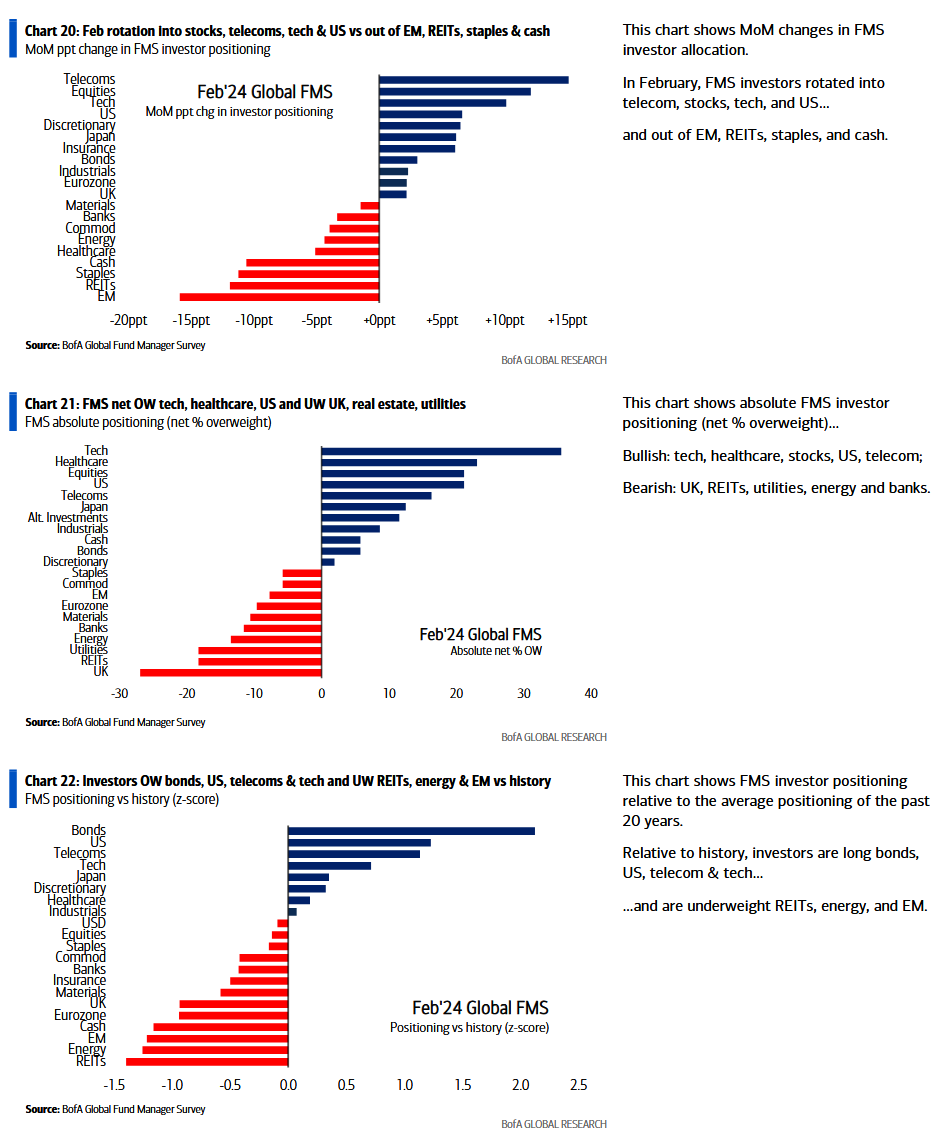

3) No one wants Energy, REITS or Emerging Markets/China (YET!):

Other Important Positioning Trends:

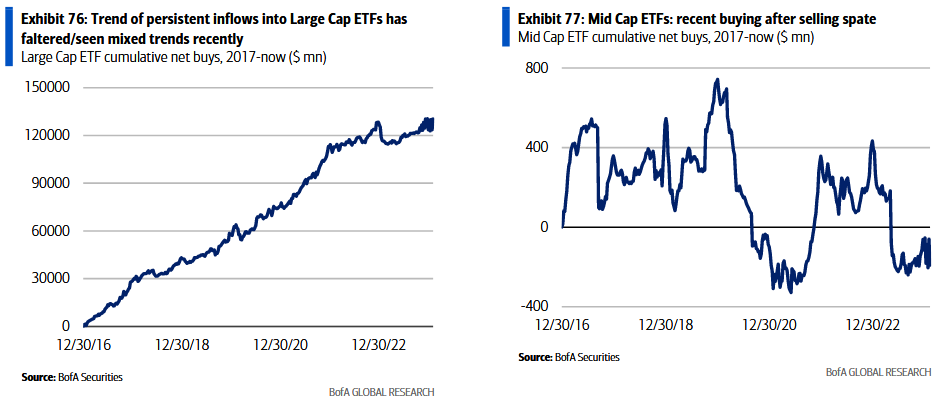

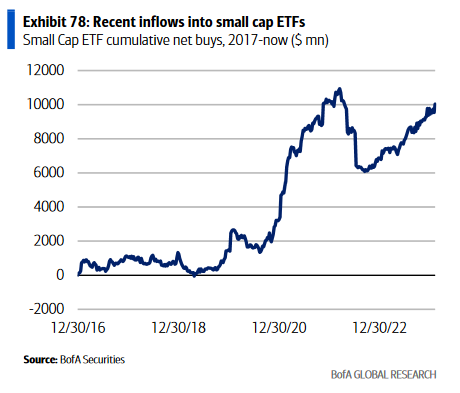

1. New (early move) from Large Cap to Mid and Small:

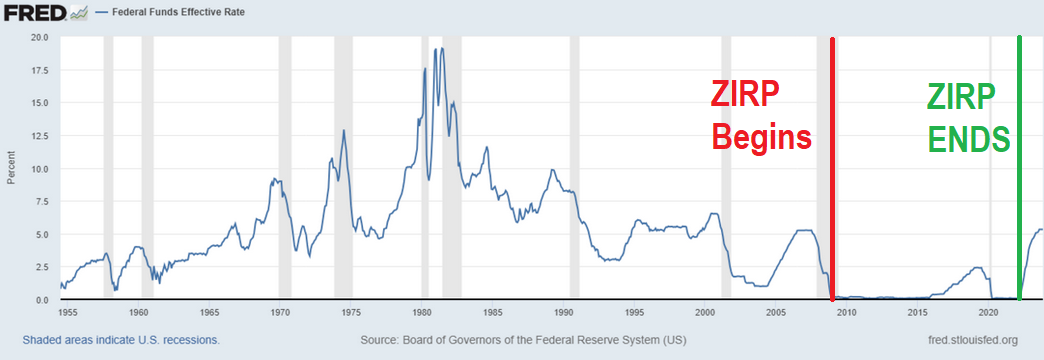

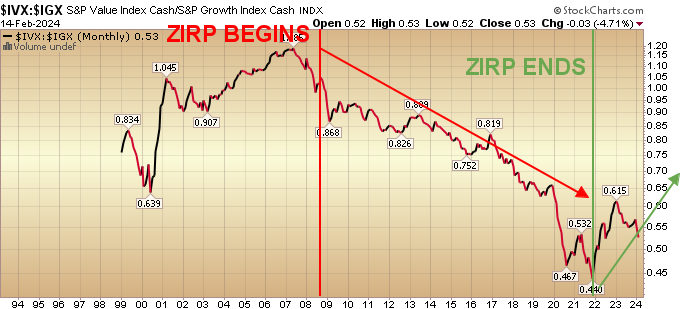

2. Now that ZIRP (zero interest rate policy) is in the rear-view mirror, Value is showing signs of a turn relative to Growth. Small Caps starting to show (possible) signs of life relative to Large Caps:

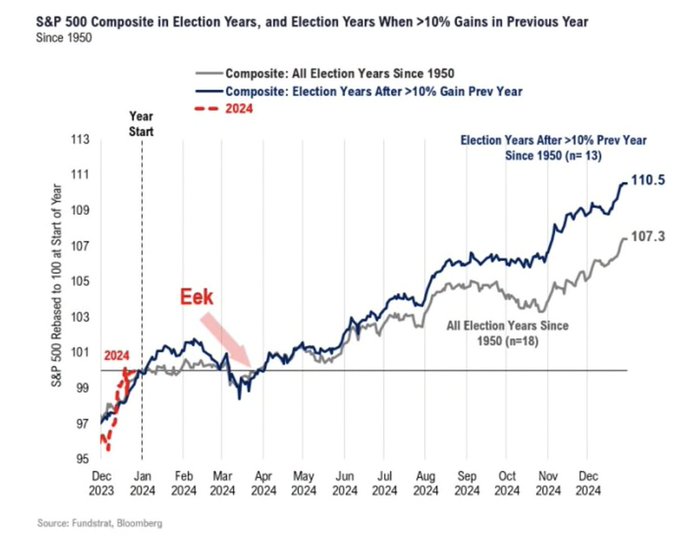

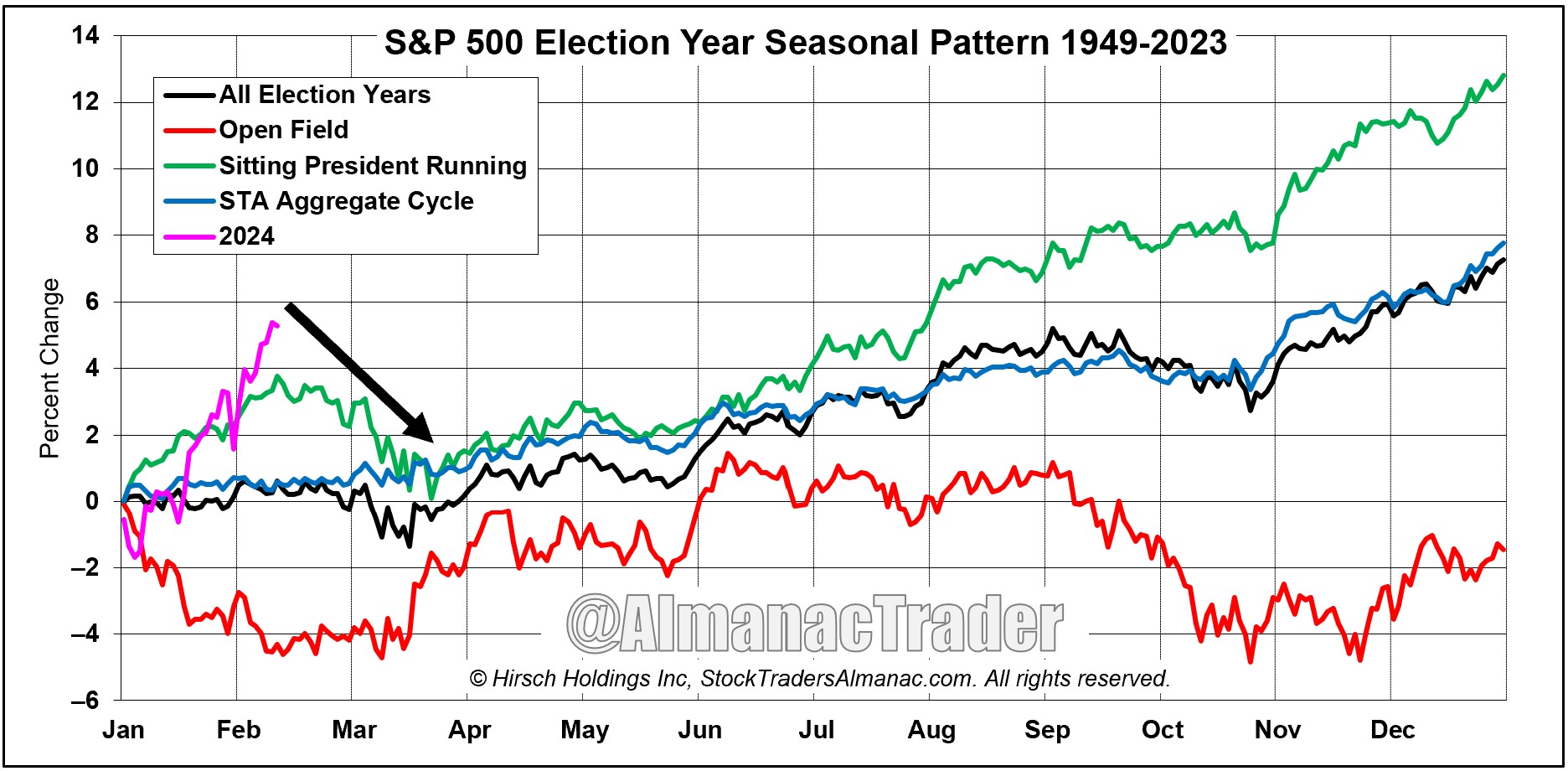

Seasonality Reminder

Seasonality Reminder

Fundstrat

Stock Traders Almanac

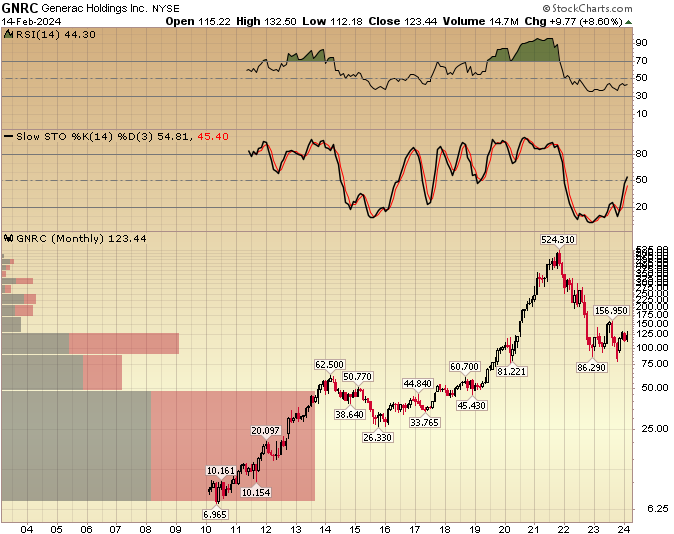

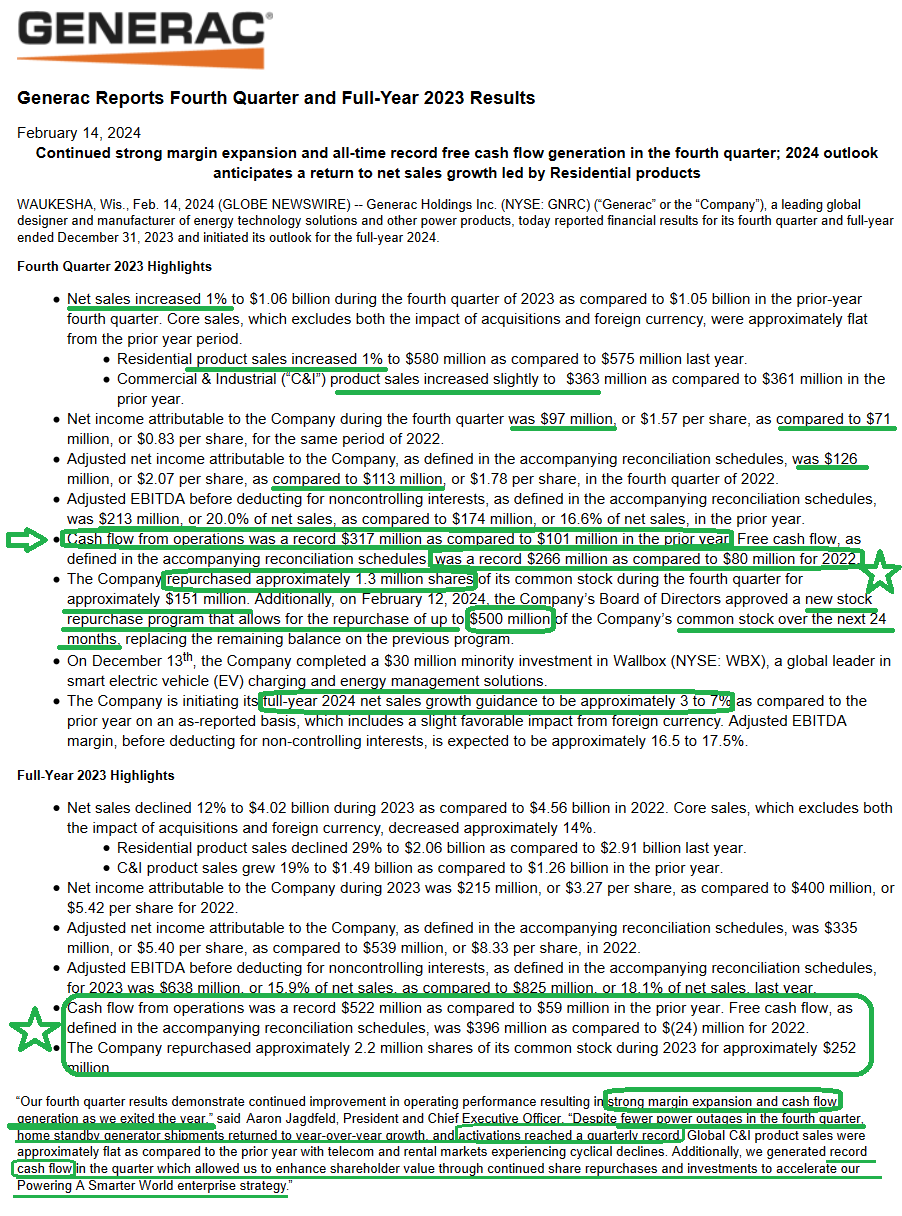

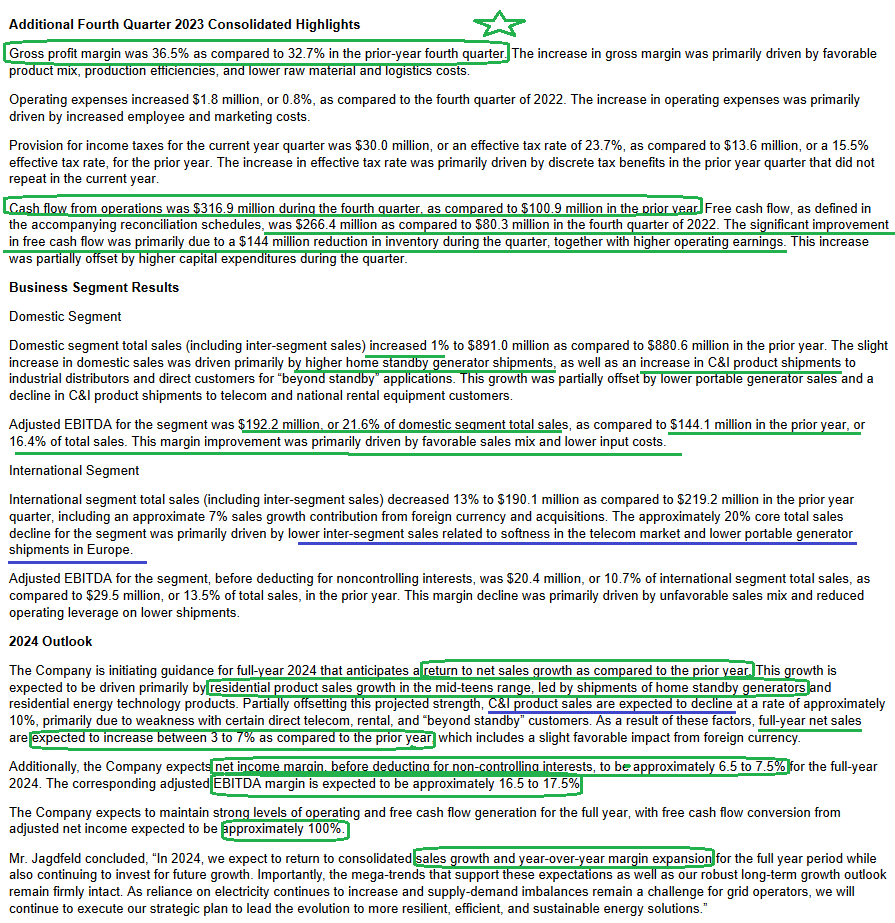

Generac

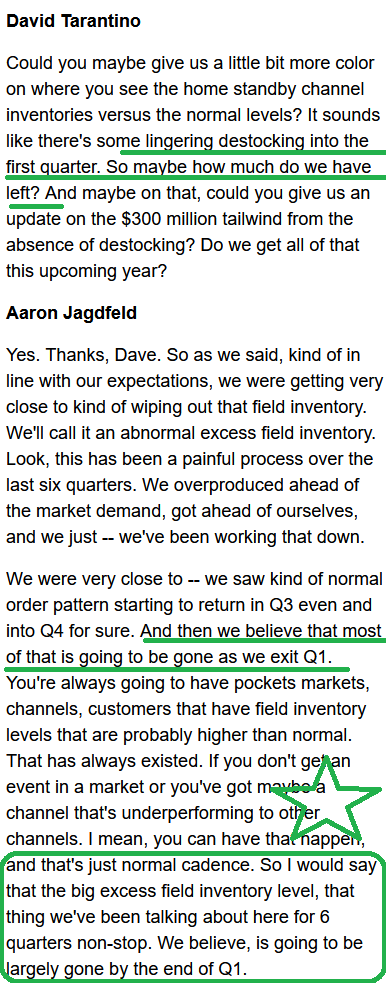

I try to highlight the results from 1-2 companies per week that we have talked about on our weekly podcast|videocast(s). Today we’ll do a deep dive on GNRC’s results:

This was my appearance on Fox Business – The Claman Countdown – from September 27, 2023 when the stock was trading at just ~$110:

Last night – after earnings – Generac’s CEO Aaron Jagdfeld appeared on CNBC to discuss earnings at his outlook. Watch this one to the very end of the interview:

Earnings Call Highlights:

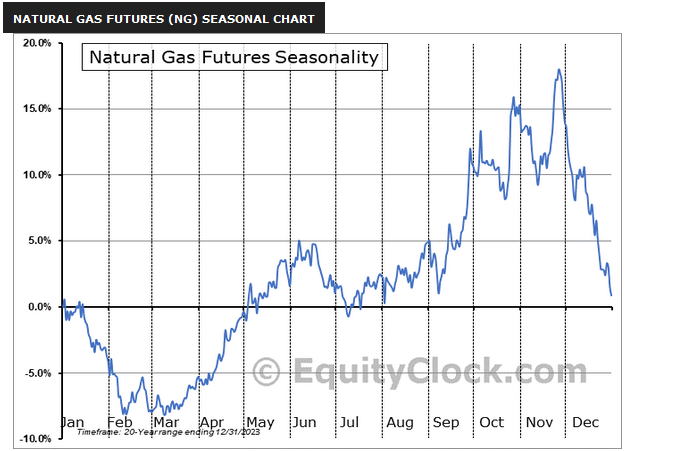

Comstock Resources

Our new Nat Gas play reported earnings. We’ll touch on them in the podcast|videocast. But earnings results are less useful for a company like this – which is simply a leveraged play on Nat Gas prices. The focus is: 1) are you paying significantly less than liquidation value (proved and unproved reserves less liabilities), and 2) Do they have satisfactory cash flow and liquidity/balance sheet to wait for the turn in prices? Quarterly earnings noise doesn’t solve for either answer. This gives a hint:

Now onto the shorter term view for the General Market:

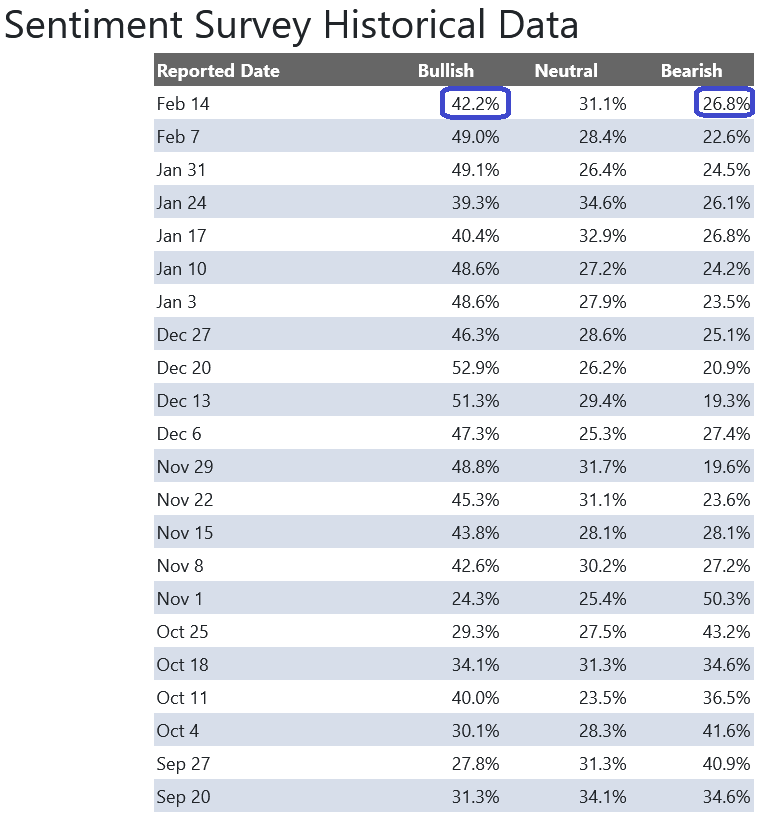

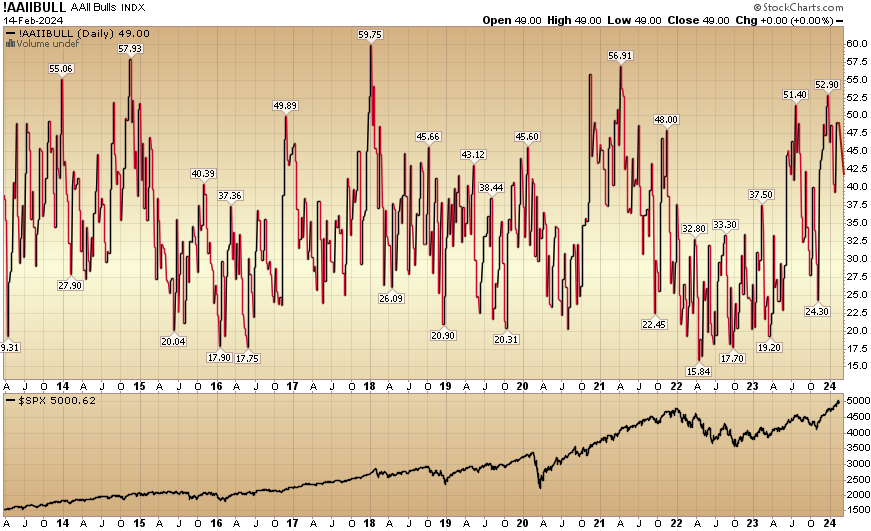

In this week’s AAII Sentiment Survey result, Bullish Percent (Video Explanation) dropped to 42.2% from 49% the previous week. Bearish Percent moved up to 26.8% from 22.6%. Retail investors are coming off the boil a bit.

The CNN “Fear and Greed” ticked down from 75 last week to 73 this week. You can learn how this indicator is calculated and how it works here: (Video Explanation)

The CNN “Fear and Greed” ticked down from 75 last week to 73 this week. You can learn how this indicator is calculated and how it works here: (Video Explanation)

The NAAIM (National Association of Active Investment Managers Index) (Video Explanation) rose to 93.77% this week from 87.36% equity exposure last week.

The NAAIM (National Association of Active Investment Managers Index) (Video Explanation) rose to 93.77% this week from 87.36% equity exposure last week.

Our podcast|videocast will be out late today or tomorrow. Each week, we have a segment called “Ask Me Anything (AMA)” where we answer questions sent in by our audience. If you have a question for this week’s episode, please send it in at the contact form here.

Congratulations to all of the new clients that came in from our Q1 raise. We will re-open to smaller accounts $1M+ again sometime in Q2. Larger accounts $5-10M+ can access bespoke service beforehand at their preference here.

*Opinion, Not Advice. See Terms