In 1985 Motley Crue released one of its major all-time hits, “Home Sweet Home.” Last night, when I was thinking about the journey of Alibaba over the last few months, this song came to mind. The journey has had a few detours, but now it’s on finally on its way back “home” to intrinsic value.

Seeing Alibaba jump ~35% in one day is evidence that the objective business/fundamental analysis was always accurate, it was simply a mercurial government leadership holding the stock back. With the government now stepping out of the way and letting business flourish once again, we expect this marvelous business to work its way back to intrinsic value over time. We may hit a few more potholes and speed bumps, but we’re on our way…

Just one more night

And I’m coming off this long and winding road

I’m on my way

I’m on my way

Home sweet home

Tonight, tonight I’m on my way

I’m on my way

Home sweet home…

I was invited on Yahoo! Finance on Wednesday afternoon to discuss the developments. Thanks to Rachelle Akuffo and Taylor Clothier for having me on:

Watch in HD directly on Yahoo! Finance

Here’s a caption they took out of the interview:

Here were my show notes ahead of the segment:

Sea Change

-The Underlying China Tech Businesses which have been hit the hardest are STILL GROWING despite an historic regulatory crackdown that began last year.

-Only 2 things that held them back: 1) Government Regulatory Crackdown 2) De-listing risk. BOTH were addressed overnight by Vice Premier Liu He when he said, “actively introduce policies that benefit markets.”

-He offered investors re-assurance that a sweeping crackdown on internet companies was nearing its end.

-China’s banking regulator said after the meeting that it would support insurance companies to increase investment in stock markets.

-The Financial Stability and Development Committee meeting concluded there is a need to “boost the economy,” in the first quarter and promised investors relief on several regulatory fronts.

–Monetary policy will be proactive in this quarter and new loans will grow appropriately, it added.

-Working with SEC to resolve HFCAA and continue listings on US Exchanges.

Example: Alibaba

-The fact that I can buy one of the greatest large cap growth stocks in history at ~6x Earnings (as of Tuesday) when you back out cash and ST investments. Alibaba will grow:

-Revenues will grow by ~32% in next 2 years.

-Earnings will grow by 30.7% in next 2 years.

-And I can buy it at a multiple that is 1/3 the S&P with at least 3x the growth.

–Reminds me of Microsoft in 2013 before it took off on an historic run.

From 2006-2013 (7 years), Microsoft grew –

- Revenues (per share) by 112.14%

- Cash Flow (per share) by 193.05%

- Earnings (per share) by 120.83%

Next 9 years up ~1,500.

From 2014-2021 (7 years), Alibaba grew –

- Revenues (per share) by 894.93%

- Cash Flow (per share) by 559.46%

- Earnings (per share) by 601.92%

Alibaba’s stock has done nothing. You can buy at 2014 prices.

STORY OF JOB:

The holders of Alibaba in recent months have gone through a massive biblical test of faith as the government has cracked down on the sector. It brings to mind the story of Job – whose faith was tested. During this test, Job lost his 10 children, his wealth and his health. Through the turmoil he kept his faith and was ultimately rewarded. The story ends with Job receiving his wealth back several fold, having another 10 children and living for another 140 years. We believe that patient and faithful shareholders of Alibaba – who understand the long term intrinsic value of the underlying businesses – will likewise be restored and multiply their wealth several fold in coming years.

Hang Seng trading at a discount to book value. Did this 4x in past before REBOUNDS:

1998: 156.46% in 17 months

2008: 110.77% in 21 months

2016: 82.52% in 23 months

2020: 35.99% in 11 months

Alibaba more than doubled index returns during these periods:

–234% in 2016-2017

–70% in 2020

China Tech has been the least loved sector globally for months. That’s about to change. “The last shall be first.” As always, opinion follows trend. No one wanted BABA at $75. EVERYONE will want it again at $250.

Earlier in the afternoon I joined Liz Claman on Fox Business – The Claman Countdown – to discuss the Fed announcement and moves going forward. Thanks to Liz and Ellie Terrett for having me on:

Watch in HD directly on Fox Business

These were my show notes ahead of the segment, but you’ll see that we gave 2 new ideas that weren’t planned. In the unplanned suggestions we referenced this data set from Strategas:

FED/INFLATION/YIELD CURVE: Following the Fed announcement, Fed Fund Futures priced in a 63% chance of 7 hikes in 2022. The 2/10 spread on the yield curve dropped to 23bps from 30bps.

-The Fed will continue to be “data dependent.” I expect rate hikes will come in lower than anticipated (4-5 vs 7 this year) as they can use the balance sheet wind down to drain liquidity this cycle. The plot will change once they announce balance sheet reduction in May – as they do not want to invert the yield curve. The dot plot is intended to jawbone inflation and buy time. The balance sheet runoff is what will sop up excess liquidity.

-As the Fed comes out of the market as a buyer of bonds this month, it will help to re-steepen the yield curve and potentially extend the cycle for another couple of years. Foreign buyers will sop up the supply as relative yields on the 10yr become attractive again.

-PPI was a bit better than expected this week, but inflation still a concern. Chinese lockdowns and ongoing Iran talks have helped moderate oil prices in the near term, but a negotiated settlement between Russia/Ukraine will be necessary to have a longer term impact. When you look at inflation it’s all energy and used cars. Used car prices came down in the last report, now we wait for Energy.

-We are seeing spending shift from goods to services as the world opens up. This will continue to alleviate some supply chain concerns.

MARKET IMPACT

Last time I was on I said despite all of the short term risks the “risk in the market was to the UPSIDE, not to the downside.” Since that time, we have held the February 24 lows.

*Never bet on the end of the world because even if you’re right you won’t get paid.

Sentiment was completely washed out:

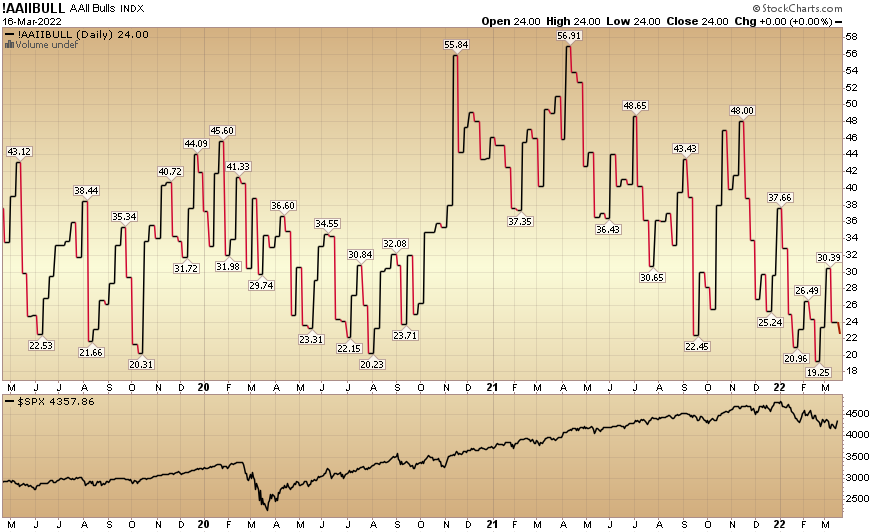

AAII Bullish Percent – Got down to 19.2% bullish. (pandemic low levels)

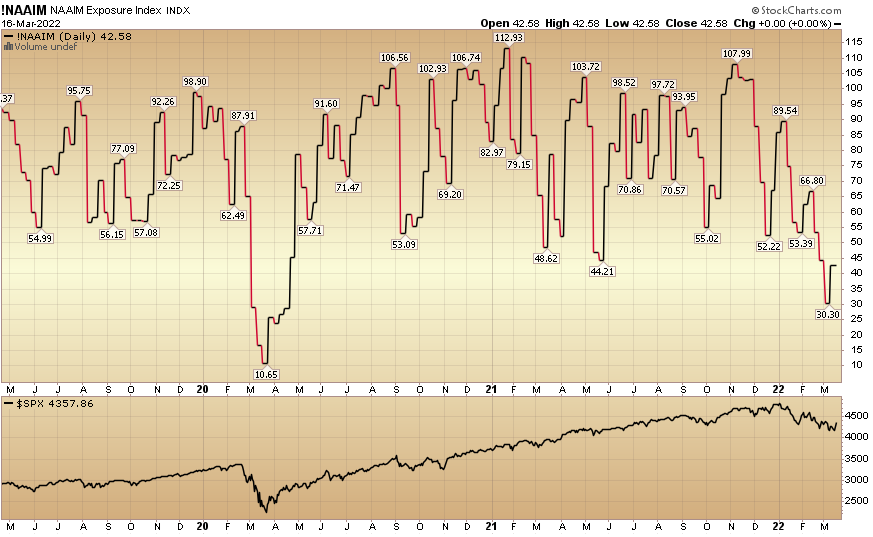

NAAIM (active manager equity exposure): Got down to 30% (lowest since 2020 pandemic lows)

Fear & Greed Index: Got down to 16 (pandemic low levels)

BET ON AMERICA

On The Claman Countdown on Friday Liz said “stay positive on good US businesses even if they are going through bad times.”

That comment was spot on, and what could be a better American business that Disney?!

As “revenge travel” comes back, one of the top destinations is going to be taking the kids to Disney after 2 years of no travel. Target said on their earnings calls that suitcases and bathing suits were top sellers!

You can buy DIS on sale at 32% off it’s 52 week highs.

Earnings are going to grow at 29% next year and could double over the next 4 years.

Disney+ added 11.8 million subscribers worldwide in its most recent quarter to reach 129.8 million.

Hulu and ESPN+ pushed its portfolio toward 200 million total subscribers.

We remain bullish on America (and Mickey Mouse!).

Over the past week I participated in two podcasts. The first one was with Justin Jarmin on Harvest Exchange. I have received a number of emails on this one with people finding it very helpful. You too will find it’s worth a listen:

Watch Directly on Harvest

And finally, I had a great conversation with Andrew Hepburn and The Pitchboard. This was the most detailed thorough interview I have ever participated in. Andrew drilled into my investment process and how I value businesses and adjust with the data. If you ever wanted a clear look under the hood, this is it. Have a listen, you’ll be grad you did. This was a special one…

Listen Directly on The Pitchboard

Sentiment

On Tuesday we published a full summary of the Bank of America Global Fund Manager Survey. When you read the contents you are going to understand why I’ve been saying for the past two weeks’ notes and podcast|videocast that that “risk in the market is to the UPSIDE, not the downside.”

March 2022 Bank of America Global Fund Manager Survey Results (Summary)

When everyone is on one side of the boat, it’s time to take the other side of the trade:

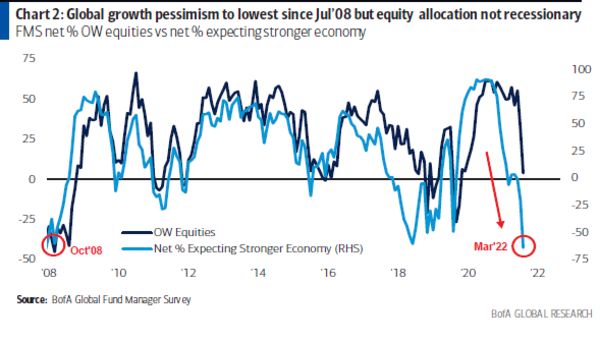

1) Global Growth expectations are the lowest since the summer of 2008 and Profit Expectations are the lowest since the Covid lows in 2020:

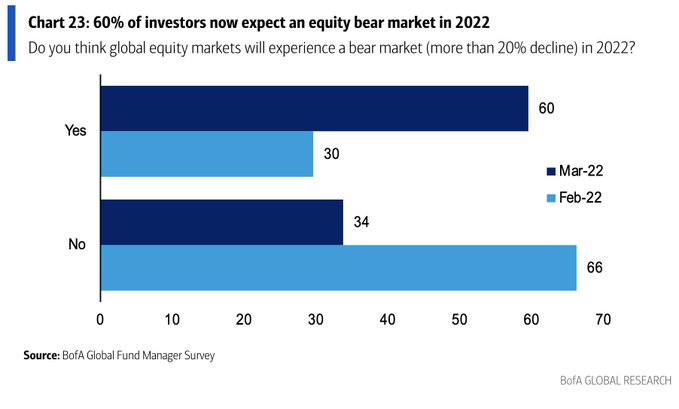

2. 60% now expect a bear market in 2022 (and the yield curve has not even inverted yet):

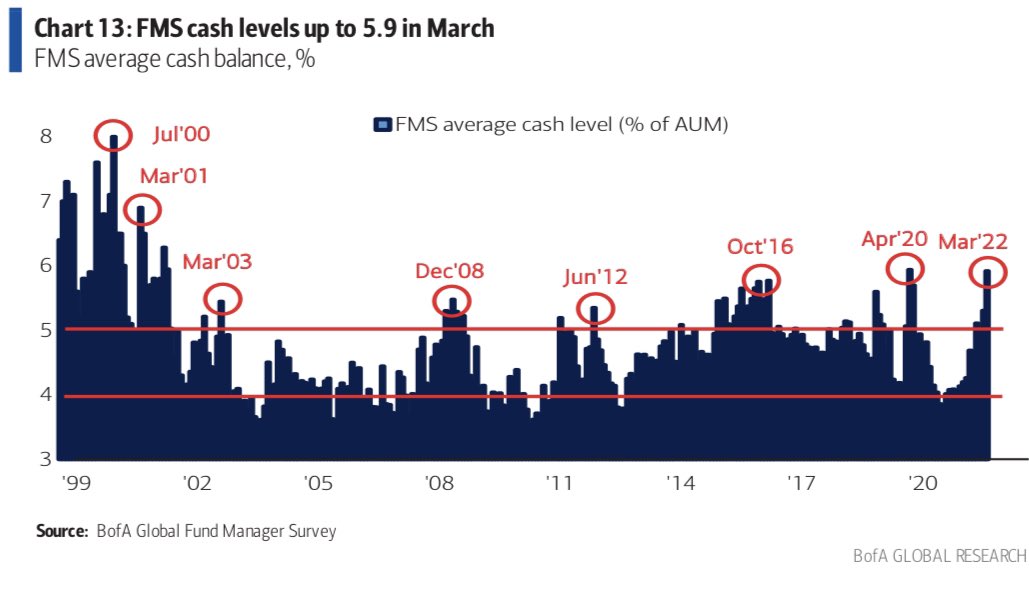

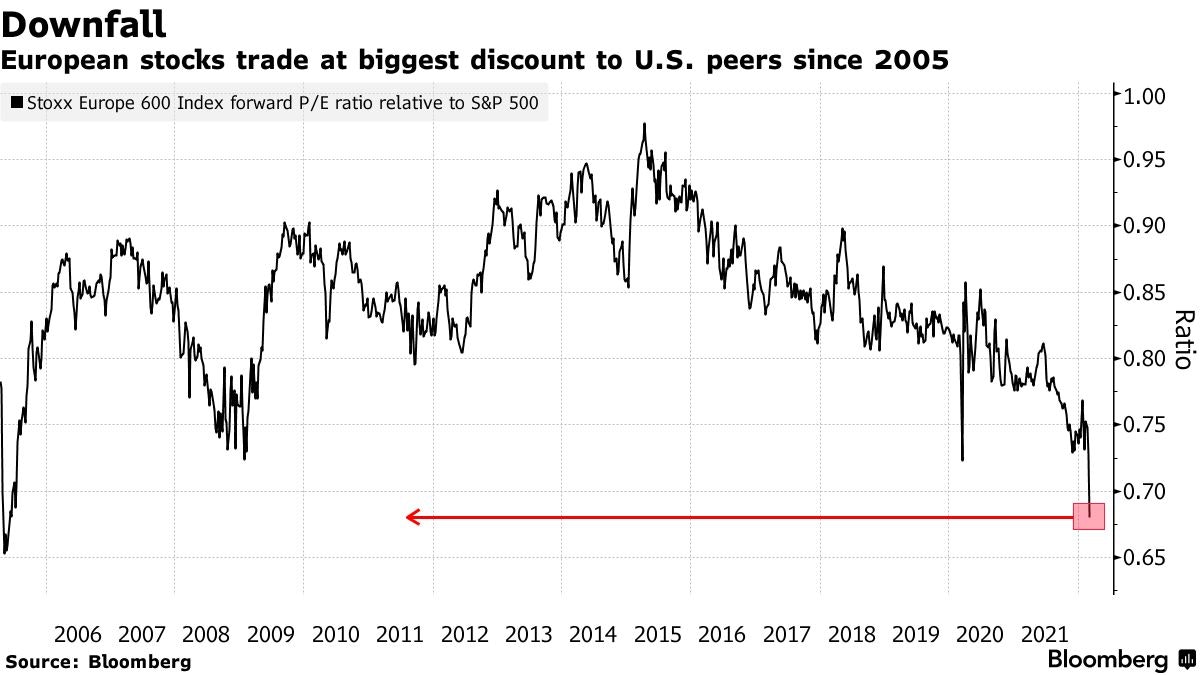

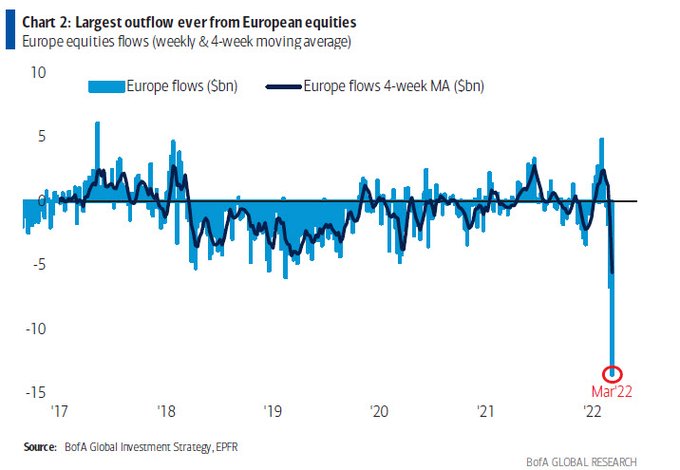

3. Cash Levels are the highest since the pandemic lows: 4. European equities are setting up for a rally given this level of pessimism as well:

4. European equities are setting up for a rally given this level of pessimism as well:

5. A net 4% of portfolio managers were overweight global equities in March, down from a net 31% overweight in February and a net 55% overweight in January.

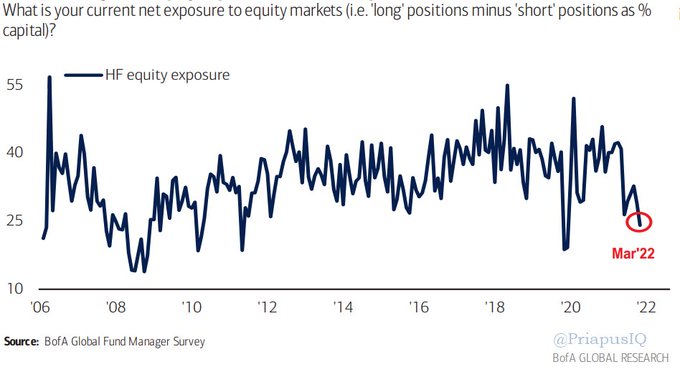

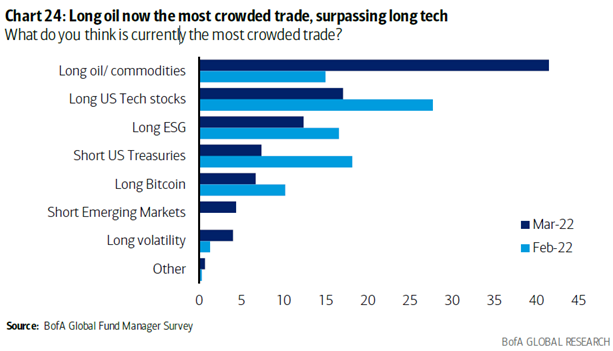

6. Hedge funds net exposure to stock markets is at its lowest level since April 2020. 7. The most crowded trade is now long commodities:

7. The most crowded trade is now long commodities:

8. Sentiment is worst than the pandemic lows and nearing GHC and European Debt crisis lows:

12.

The Nasdaq Composite fell to a 52-week low, then surged at least 2.5% on back-to-back days.

This happened 5 other times in its history.

4 of those marked multi-year lows. pic.twitter.com/lGYoHxUmom

— SentimenTrader (@sentimentrader) March 16, 2022

13.

The VIX closed beneath 30 after 11 consecutive days above this level.

This could be a good sign, as when previous streaks ended it brought some solid returns.

A year later higher 11 of 12 times and up nearly 22% on average. pic.twitter.com/MQRyoPLaCD

— Ryan Detrick, CMT (@RyanDetrick) March 16, 2022

13.

Tech is near the most oversold levels in history.

Bears see the big Bear Markets.

Bulls see the historic rallies – some even in Bear Markets.

Traders only react – they Buy strength (a turn UP), set Stops, and follow the market.

Be prepared. pic.twitter.com/a9nE9HgoRO

— Macro Charts (@MacroCharts) March 12, 2022

14.

$SPX We are currently in a Secular Bull Market. It sure doesn’t feel that way but we are. History tells us that these periods last roughly 18-ish years but not a lot of data. The current Secular Bull is ~ 9yrs. Still a baby. Will it be different this time? No idea. pic.twitter.com/orZdx3Gms8

— Alan Cohen (@al_xdpg) March 13, 2022

15. The “Pain Trade” is UP. The market is designed to inflict the most pain to the most amount of people at any one point in time (i.e. it is designed to fool most of the people, most of the time). Based on how people are currently positioned, we believe “max pain” is higher, not lower. Click on image to enlarge:

If this is true 👇, what is the “max pain” for the market? That is, what move would cause the most pain to the most participants based on how they are currently positioned? pic.twitter.com/3SPH2kGzAS

— Thomas J. Hayes (@HedgeFundTips) March 13, 2022

China

I sent these two charts to a friend who was questioning his positions in China Tech on Tuesday. I told him I was frustrated too, but not worried. Nothing had changed in the underlying businesses and eventually the intrinsic value would be realized. I also pointed to the fact that these were likely levels that institutions would come in to defend the stock as that is where the long-term holders were concentrated:

We posted this tweet over the weekend when sentiment was despondent:

“History doesn’t repeat itself, but it often rhymes.”

The last few times Hong Kong was trading below book value, sharp rebounds followed. $BABA

More of this in my @MoneyShow presentation: https://t.co/xaLBwDWP4o pic.twitter.com/nmXW1K0hGR

— Thomas J. Hayes (@HedgeFundTips) March 11, 2022

We posted this the next day regarding Alibaba when someone was whining about the stock on Twitter (click on image to enlarge):

Thoughts on $BABA pic.twitter.com/EeMd6PFjF7

— Thomas J. Hayes (@HedgeFundTips) March 12, 2022

I recorded this podcast last week and we posted it on Twitter this week:

Just yesterday, Chinese internet stocks were deemed “uninvestable.” Suddenly, after a significant gap up, everyone’s going bargain hunting. $BABA

Great convo with @JustinJarman @HVST

Link to full VideoCast: https://t.co/UUxGQZvnkd pic.twitter.com/paFotr0A0J

— Thomas J. Hayes (@HedgeFundTips) March 16, 2022

*Of note, the major sell-side analyst (who shall remain nameless) that downgraded Alibaba to a sell with PT $65 on Monday, is the same analyst to put an “Overweight” on the stock in early January – after the $30 bounce off December lows. He also had an “Overweight” $320 price target on BABA on OPINION FOLLOWS TREND…

Now onto the shorter term view for the General Market:

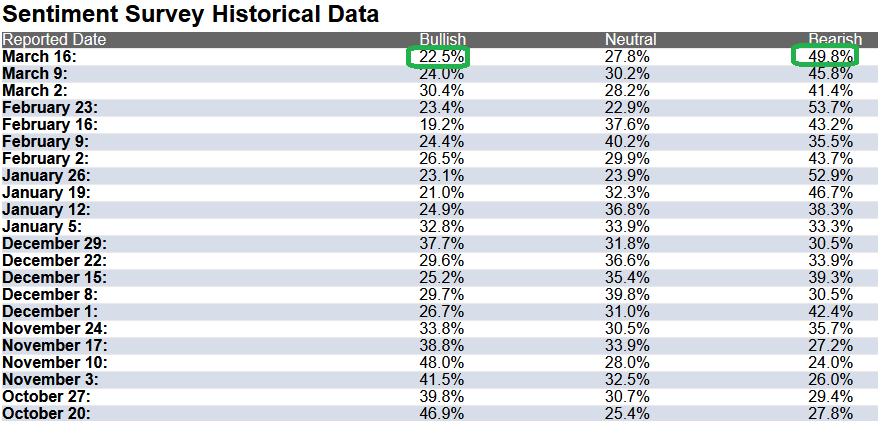

In this week’s AAII Sentiment Survey result, Bullish Percent (Video Explanation) fell to 22.5% this week from 24% last week. Bearish Percent rose to 49.8% from 45.8%. Retail trader/investor fear is back to 2020 pandemic low levels.

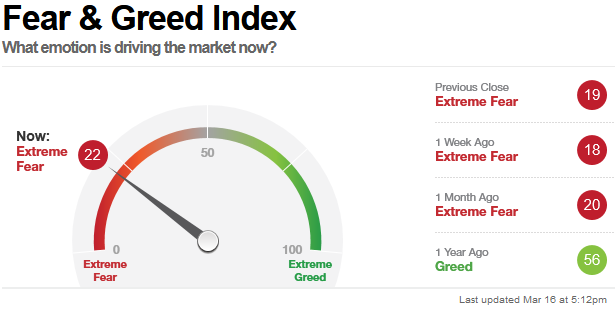

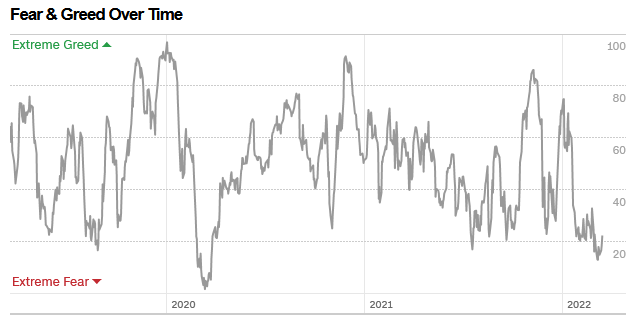

The CNN “Fear and Greed” Index rose from 16 last week to 22 this week. Fear is still near its highest level since the pandemic lows in 2020. You can learn how this indicator is calculated and how it works here: (Video Explanation)

The CNN “Fear and Greed” Index rose from 16 last week to 22 this week. Fear is still near its highest level since the pandemic lows in 2020. You can learn how this indicator is calculated and how it works here: (Video Explanation)

And finally, this week the NAAIM (National Association of Active Investment Managers Index) (Video Explanation) moved up to 42.50% this week from 30.30% equity exposure last week. Managers still have their lowest exposure to equities since the 2020 pandemic lows. Managers will have to chase any strength in coming weeks.

Our podcast podcast|videocast will be out tonight or tomorrow. Each week, we have a segment called “Ask Me Anything (AMA)” where we answer questions sent in by our audience. If you have a question for this week’s episode, please send it in at the contact form here.