Key Market Outlook(s) and Pick(s)

On Wednesday, I joined Brian Sozzi, Brooke DiPalma, and Ines Ferre on Yahoo! Finance to discuss markets, the economy, outlook, $AAP, $XRAY, $HRL, $PFE, and a lot more. Thanks to Justin Oliver, Brian, Brooke, and Ines for having me on:

Stanley Black & Decker Update

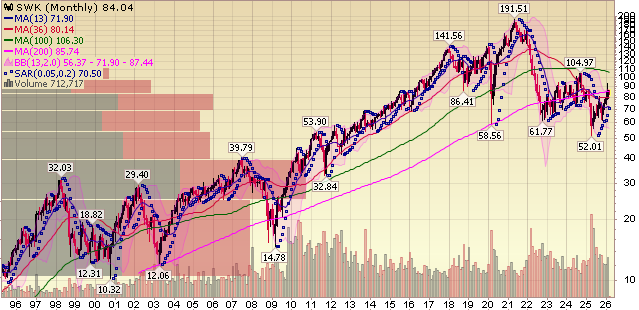

Stanley Black & Decker is one of our favorite pick-and-shovel ways to play the long-awaited housing market recovery.

The company is now turning the page on a multi-year restructuring journey that began in mid-2022 after getting caught offsides in the destock-restock cycle, leaving the company with a bloated balance sheet amid a rate-driven housing slowdown. The turnaround plan centered on a $2B cost reduction program built on supply chain improvements, inventory reductions, and rightsizing the corporate structure, all aimed at resuscitating gross margins that had been clobbered to just 19.5% in Q4 FY22 back toward their historical 35%+ range. At the same time, SWK found itself with an overleveraged balance sheet, with net leverage reaching 5.9x at the end of FY23 following an ill-timed acquisition just ahead of the slowdown.

The good news is that the latest Q4 earnings report largely closes the chapter on this restructuring effort.

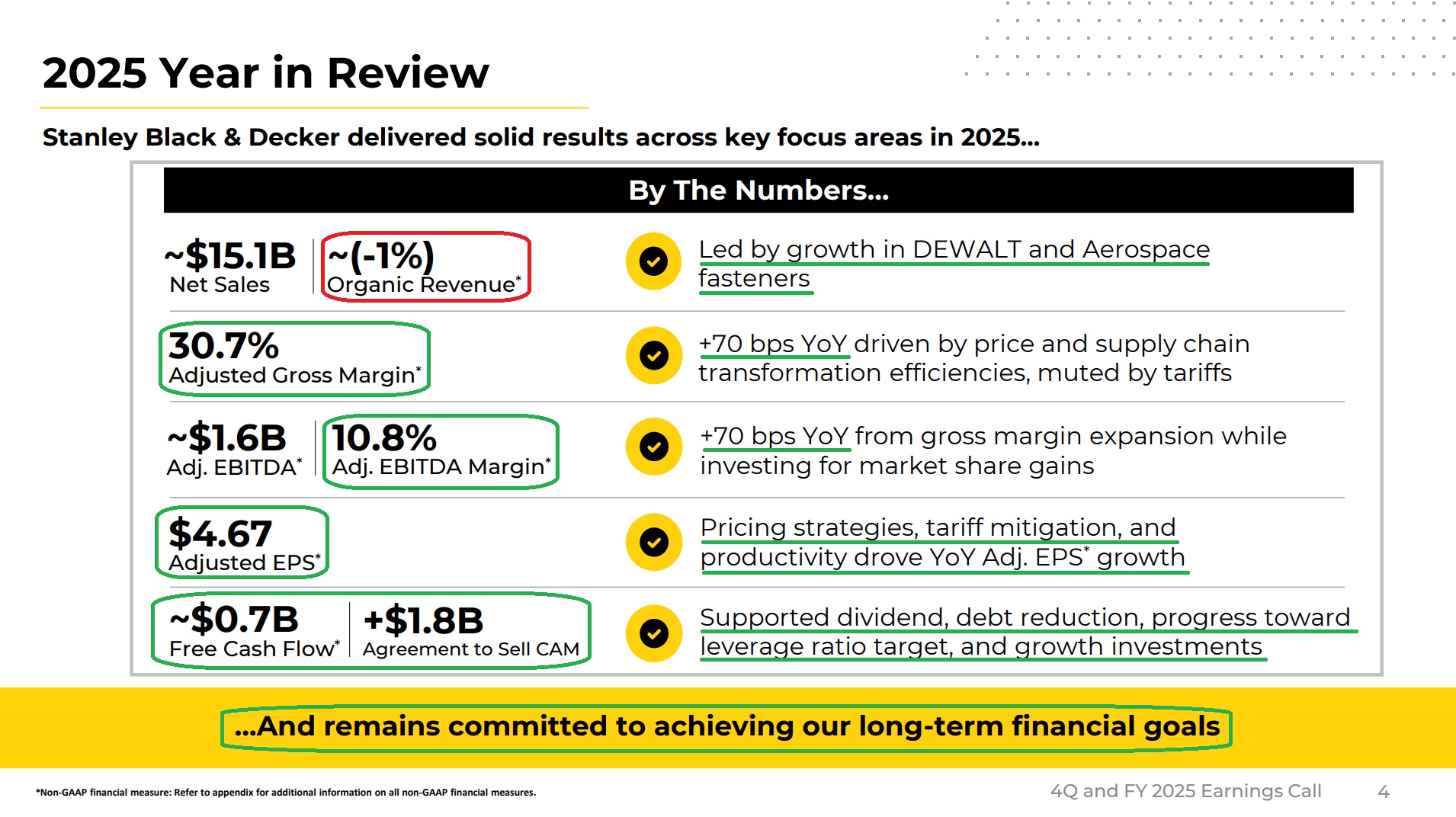

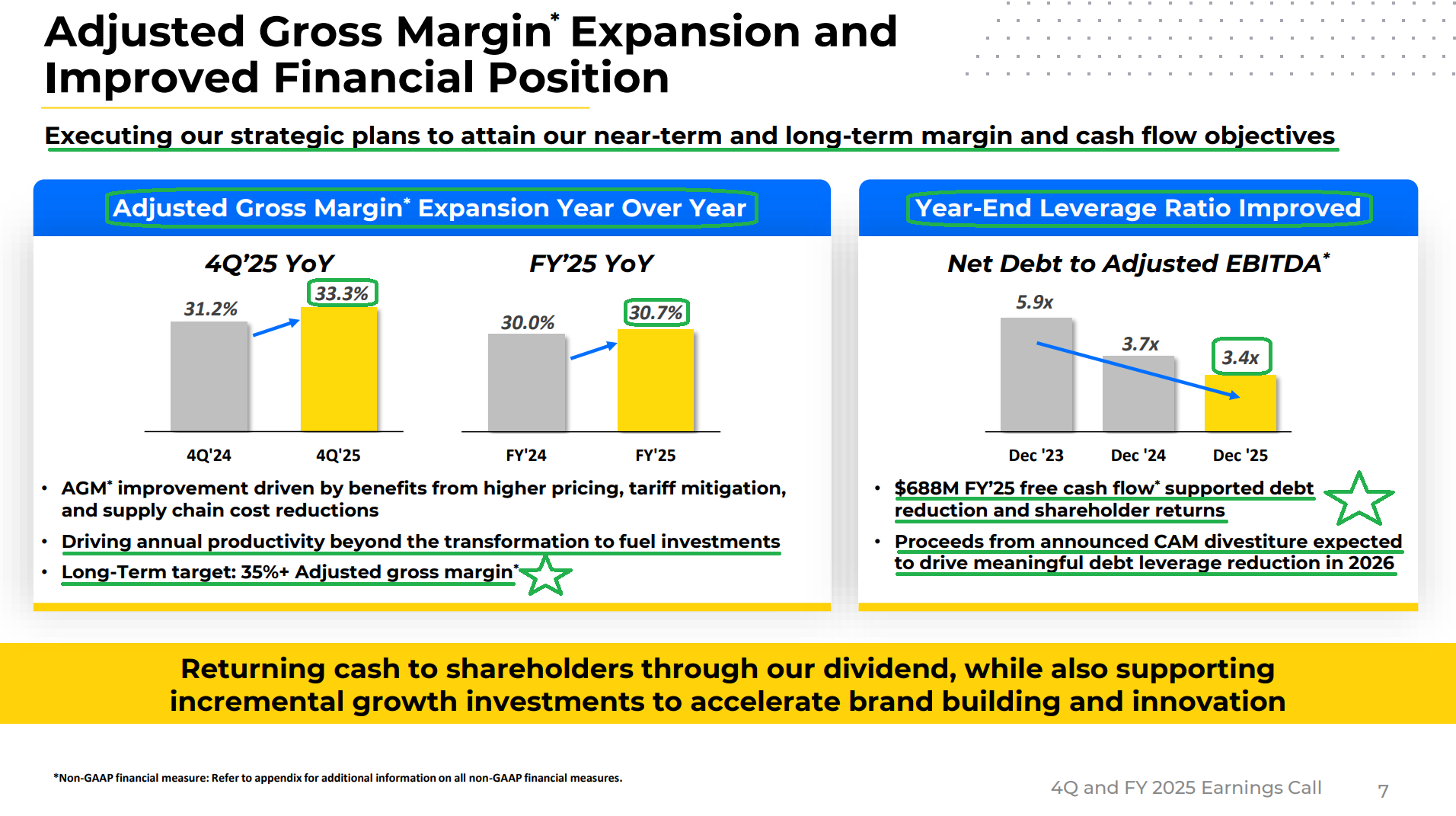

Management squeezed another $120M of cost savings out of the business in Q4, bringing cumulative pre-tax run-rate cost savings to $2.1B, ahead of the original $2.0B target and representing north of $13 per share in savings. Those savings have helped gross margins rebound from depressed levels to 33.3% in Q4 (+210 bps Y/Y), knocking on the door of the 35%+ target management expects to reach by the end of FY26. On the balance sheet, net leverage has improved by ~2.5 turns over the past two years to 3.4x, with debt reduced by $1.3B and adjusted EBITDA increasing by $500M (+44%) over the same period.

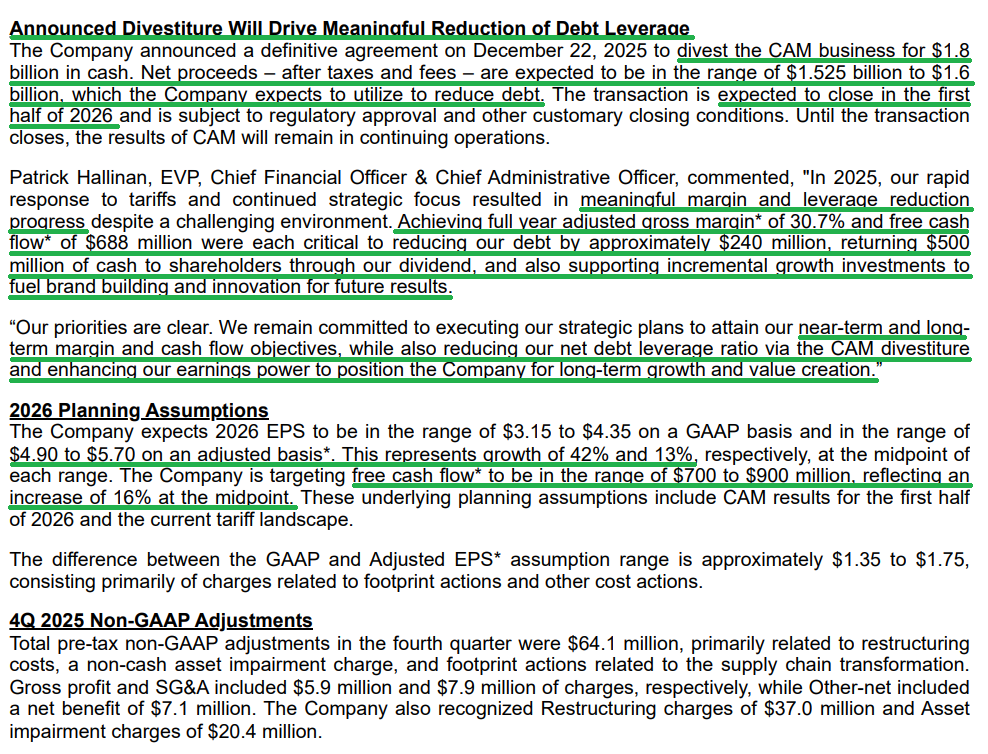

The final piece of the balance sheet cleanup came with the announcement of the pending sale of the CAM (Consolidated Aerospace Manufacturing) business to Howmet Aerospace in an all-cash transaction valued at $1.8B (~18x EBITDA), expected to close in the first half of 2026. With net proceeds of $1.525–$1.6B earmarked for debt repayment, the transaction supports another ~1.0–1.25 turns of deleveraging and puts SWK well on track to reach ~2x net leverage by year end.

With the heavy lifting now largely complete, SWK emerges as a leaner, stronger business with the focus shifting back to its core brands and a return to organic growth. On that front, management expects low-single-digit organic revenue growth in FY26, marking the first full year of positive organic growth since FY21. Growth will be led by DEWALT, the $7B+ pro-focused franchise that once again defied gravity in FY25 with low-single-digit growth, along with a long-awaited sales inflection in the DIY-oriented CRAFTSMAN and STANLEY brands driven by some of their largest new product launches in recent history.

What’s even more exciting is that this return to growth is expected in a market that remains flat and under pressure throughout the year. In other words, when the cycle finally turns and the beachball of pent-up demand breaks free thanks to all the secular drivers we often discuss (~4M unit housing shortage, 70M+ millennials in prime family formation years, lower rates, significantly aged housing stock >40 years, etc.), SWK will find itself better positioned than ever before to capitalize.

And while we wait, we sit back and are paid handsomely with a 4%+ (and growing) dividend yield, a payout the company has maintained for 149 consecutive years with 58 straight years of increases.

All the signs we want to see with a name like SWK are now in place. Growth is inflecting, margins are expanding, and FCF is accelerating (~$800M expected in FY26, +16% Y/Y). With the balance sheet cleaned up, share repurchases are back on the table as well. With shares still down more than 60% from their prior highs, we continue to view this recovery as just getting started, as the world’s #1 leader in tools since 1843 reminds the market what it’s all about.

Q4 Earnings Breakdown

10 Key Points

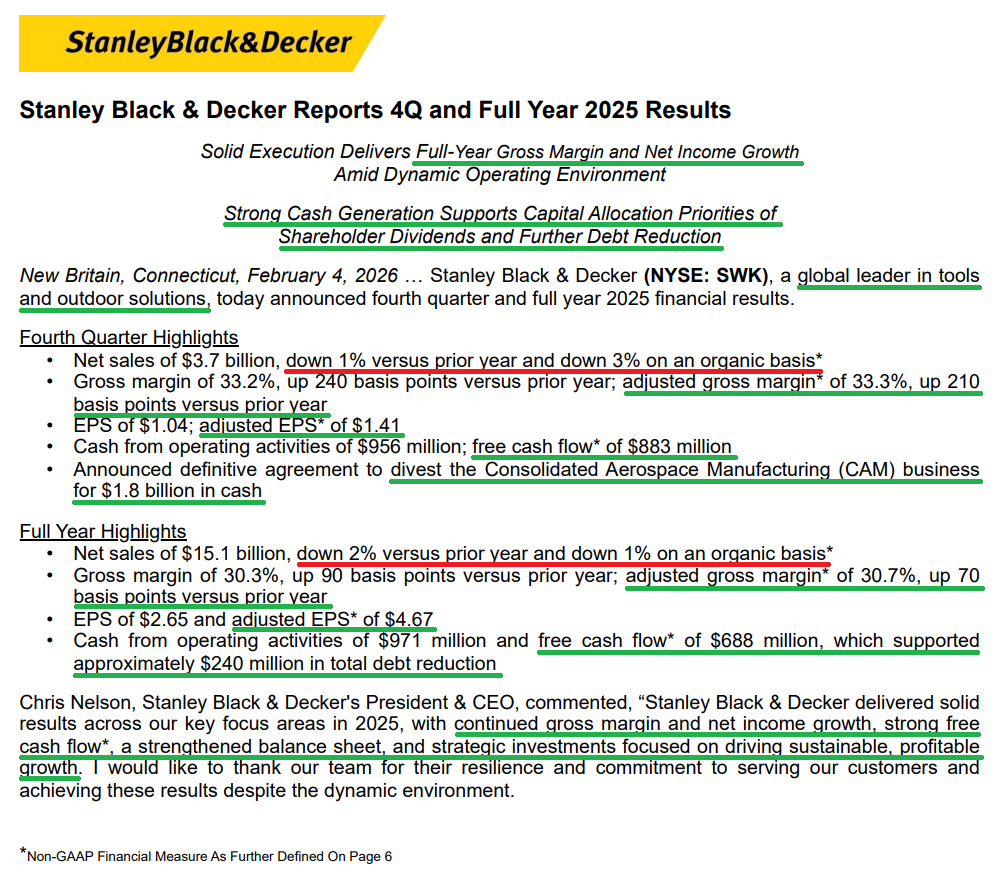

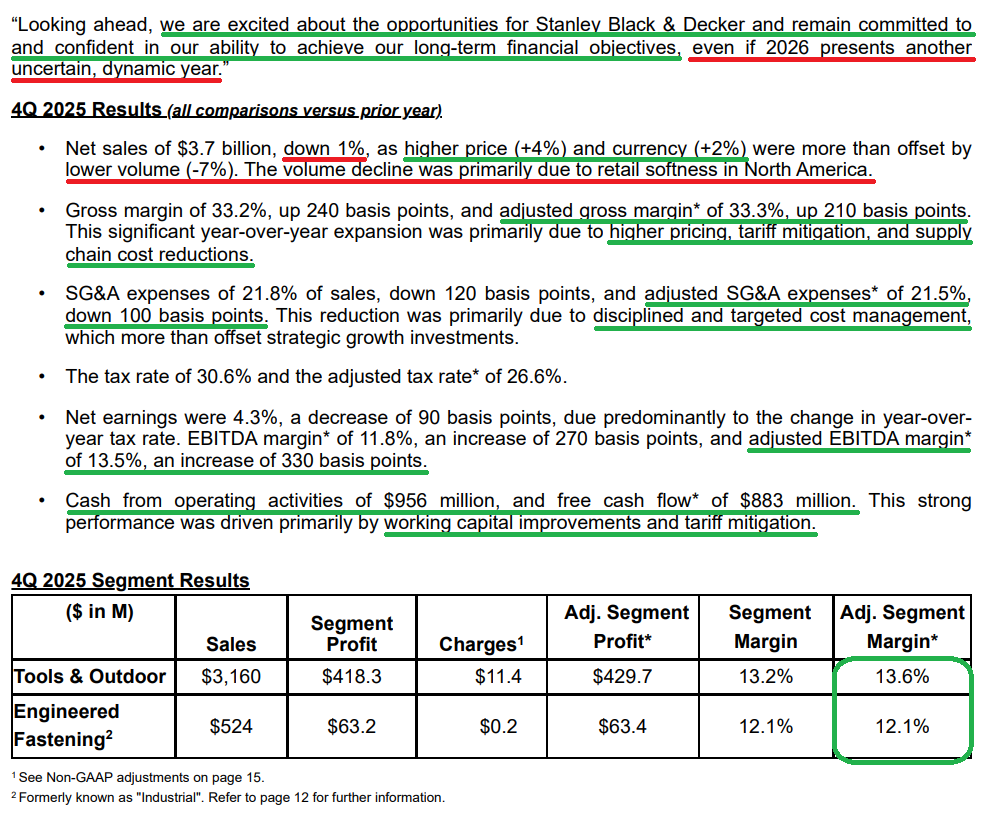

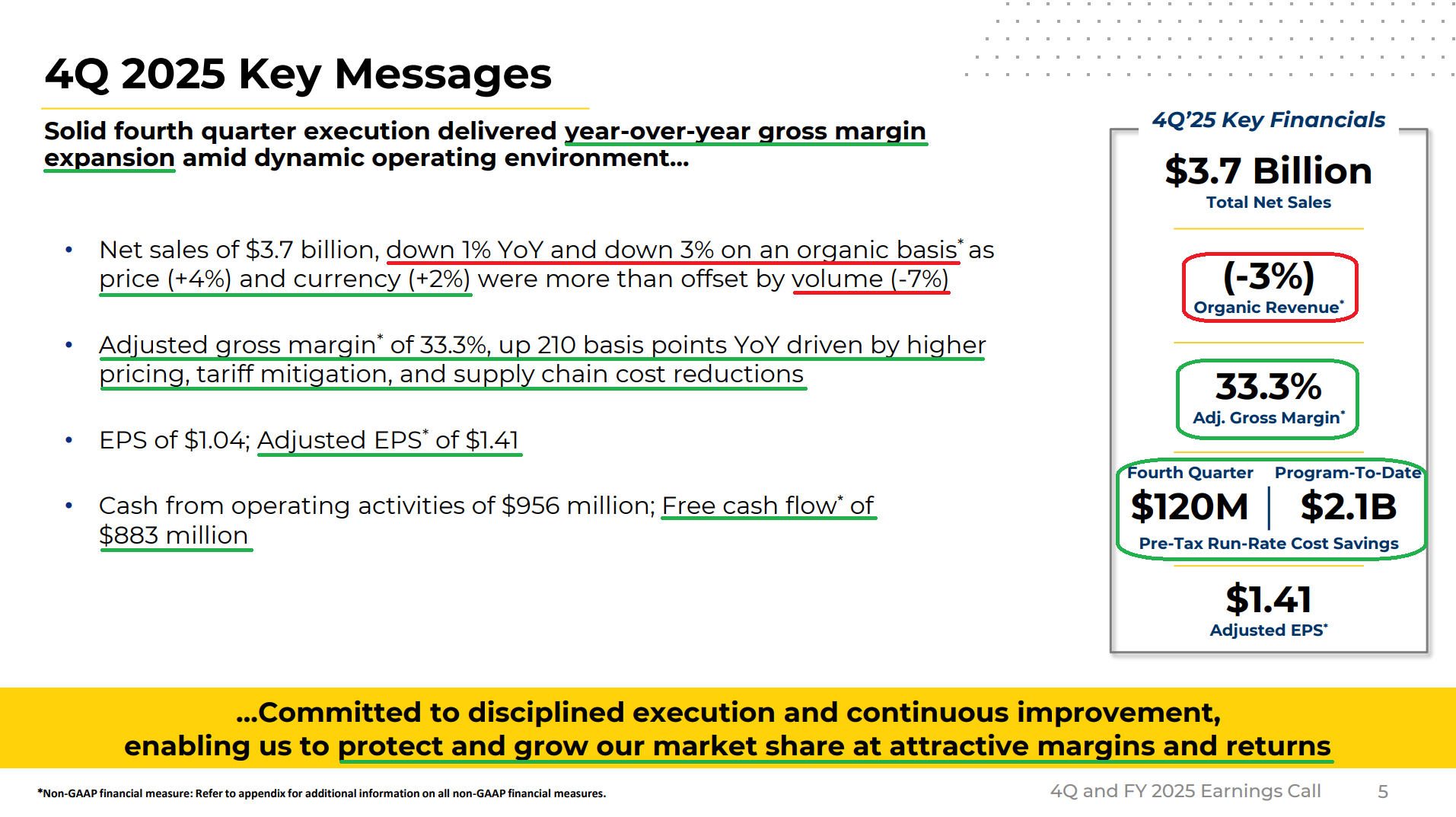

1) SWK reported Q4 revenue of $3.7B (-1% reported, -3% organic), slightly missing consensus of $3.78B, and bringing FY25 net sales to $15.1B (-2% reported, -1% organic). Adjusted EPS of $1.41 in Q4 (-5% Y/Y) came in well ahead of consensus of $1.28, bringing FY25 EPS to $4.67 (+7% Y/Y), ahead of both prior guidance and consensus of $4.55.

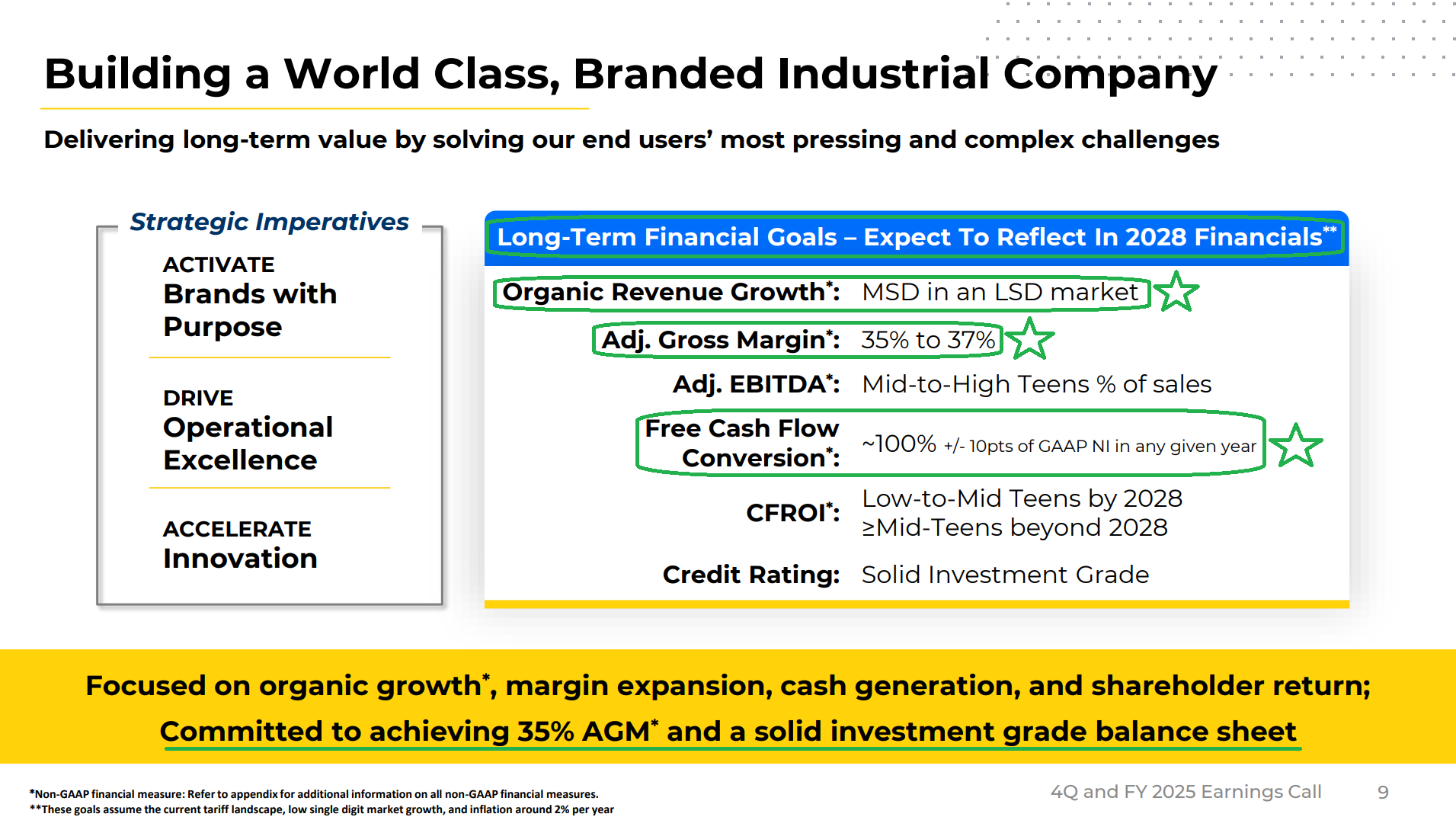

2) Adjusted gross margin (the #1 metric in the SWK turnaround) reached 33.3% in Q4 (+210 bps Y/Y), bringing FY25 adjusted gross margin to 30.7% (+70 bps Y/Y). Management reiterated the path back to the long-awaited 35%+ target by Q4 2026, with FY26 expected to deliver at least 150 bps of expansion (implying ~32.2%). The last time SWK generated a full year above the 35% threshold was 2018 (35.2%), when EPS reached $8.15 and the stock traded well north of $150.

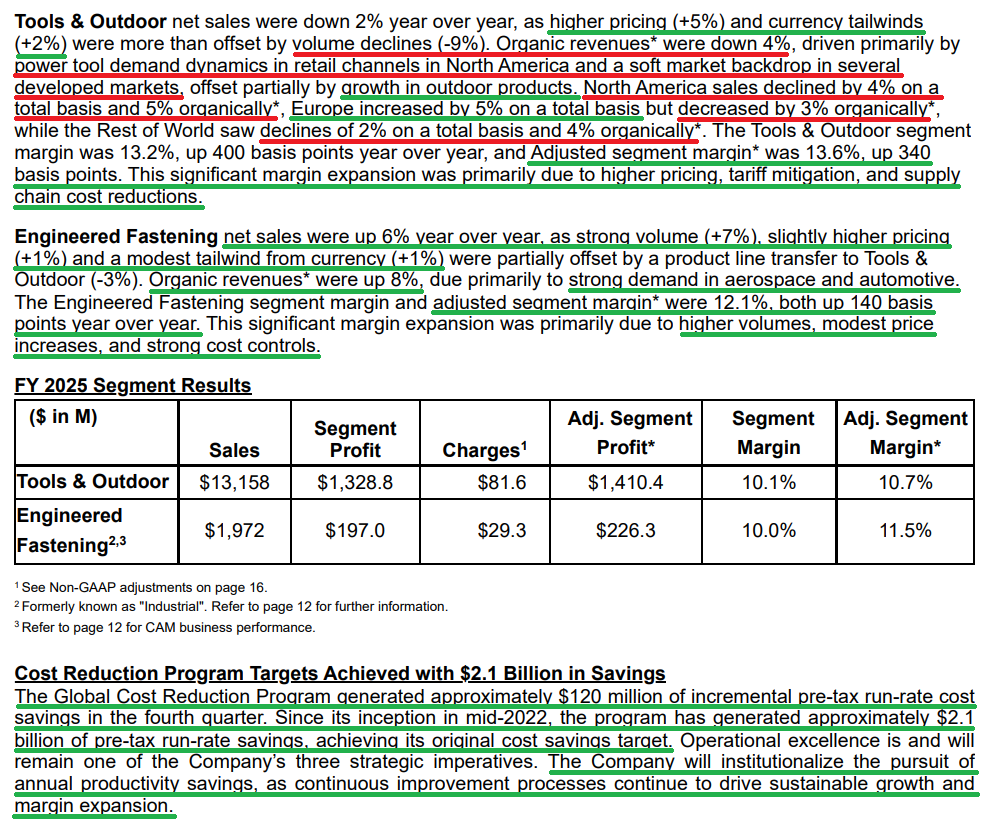

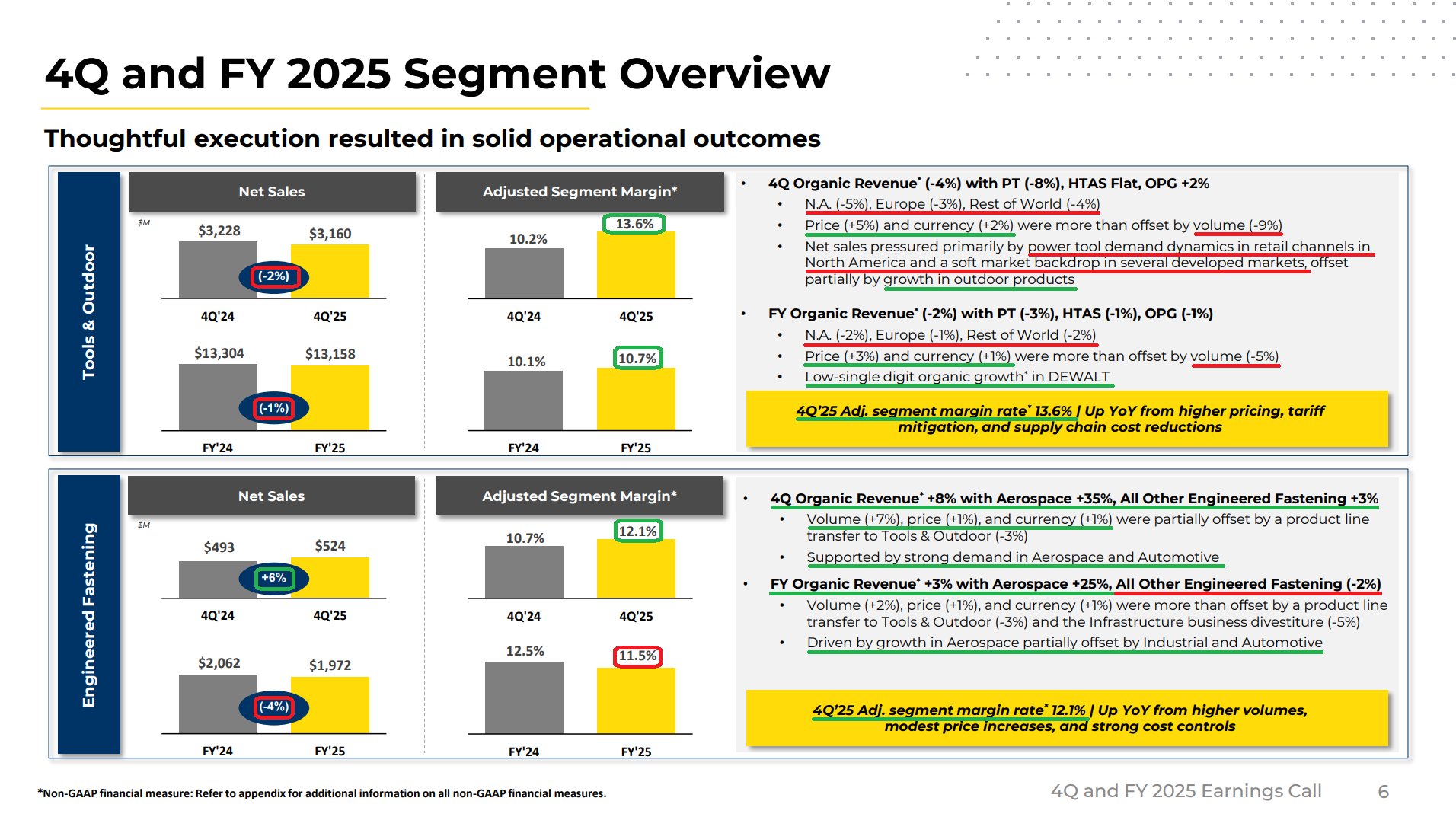

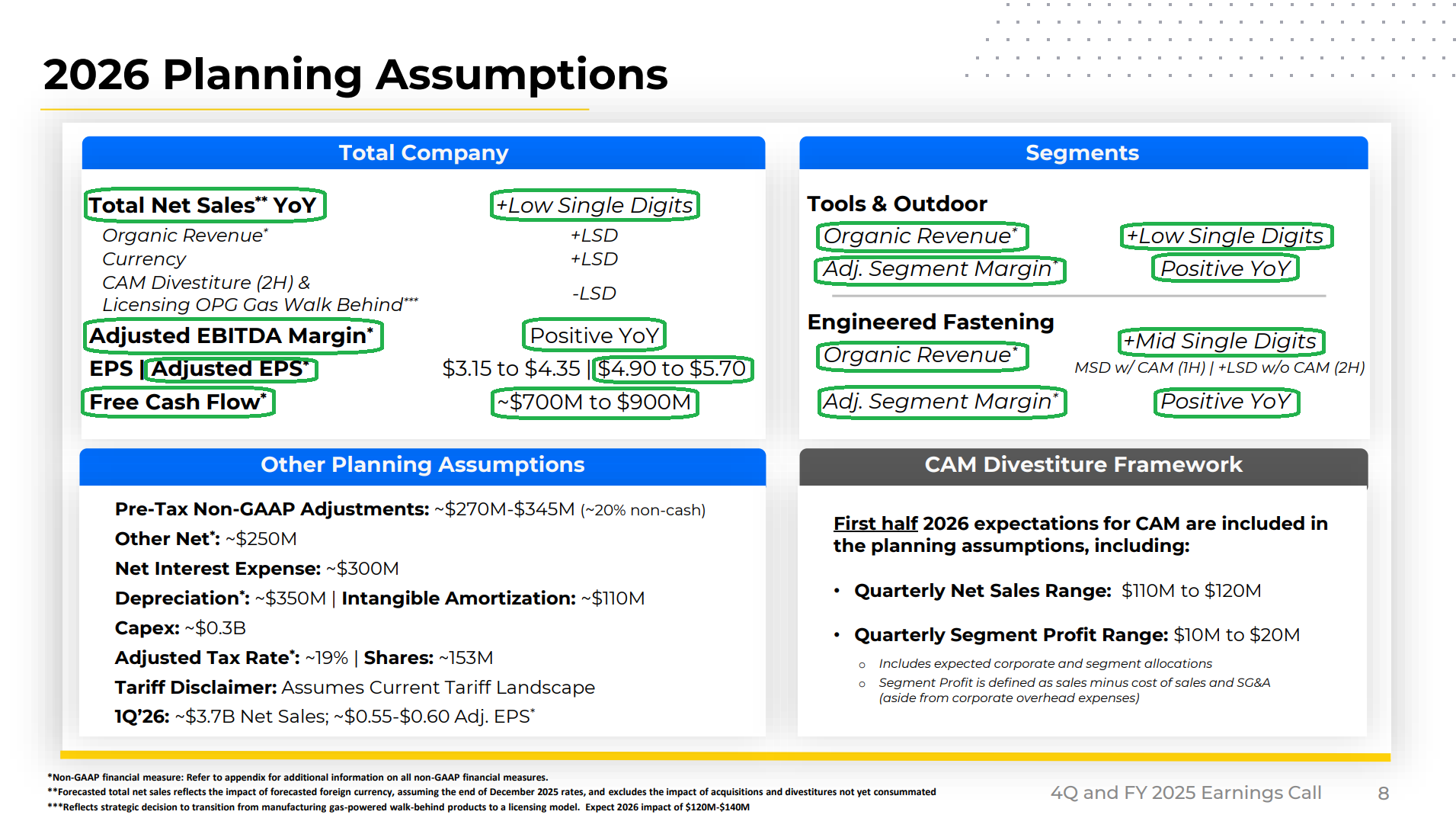

3) The Tools & Outdoor segment (87% of total sales) posted Q4 net sales down 2% (-4% organic), as higher pricing (+5%) and currency tailwinds (+2%) were more than offset by volume declines (-9%), bringing FY25 Tools & Outdoor net sales to -1% (-2% organic). Q4 weakness was driven by a softer market backdrop, partially offset by +2% organic growth in the Outdoor segment on strong preseason orders. For FY26, management expects low-single-digit growth and positive Y/Y segment margins in a flat overall market, led by continued strong growth at DEWALT (up low single digits in FY25) and a sales inflection in core brands STANLEY and CRAFTSMAN.

4) The Engineered Fastening segment (13% of total sales) saw Q4 net sales grow 6% Y/Y (+8% organic), driven by strong demand in aerospace fasteners (+35% Y/Y) and mid-single-digit growth in automotive on strong sales to auto OEMs. For the full year, the segment posted 3% organic revenue growth, which management expects to accelerate to mid-single-digit organic growth in FY26 with positive Y/Y segment margins.

5) Prior to the Q4 earnings release, SWK announced the pending sale of its CAM (Consolidated Aerospace Manufacturing) business to Howmet Aerospace in an all-cash transaction valued at $1.8B. Management expects net proceeds of $1.525-$1.6B, with the deal on track to close in H1 2026. The price came in well above the $1.0-$1.5B consensus expectation, implying ~18x expected 2026 EBITDA for the segment. Proceeds will be used for further debt reduction, supporting incremental leverage reduction of ~1.0-1.25 turns and putting SWK well on track to reach its leverage target of 2.5x or below.

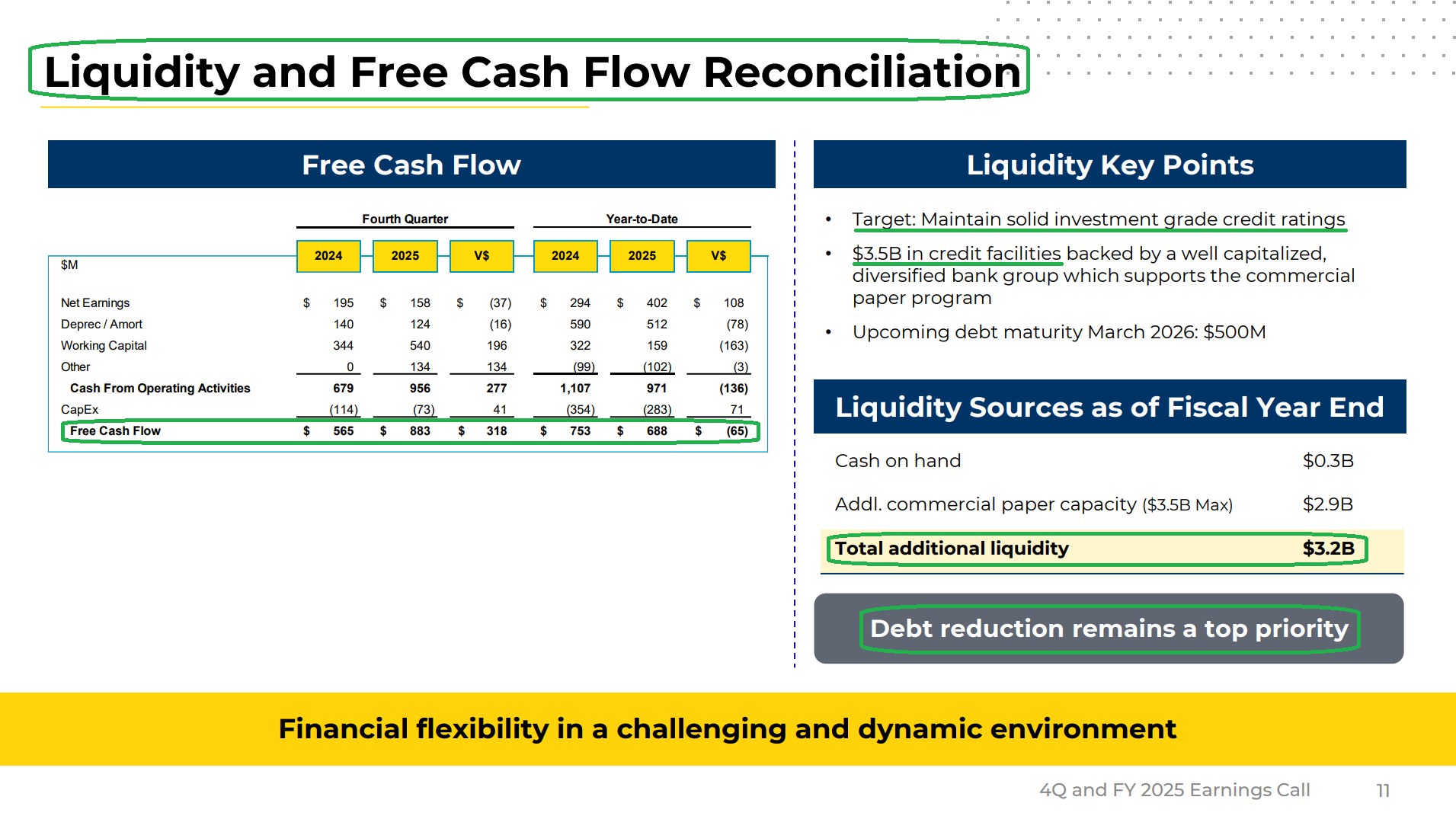

6) Management continues to make progress on the balance sheet, with net leverage improving to 3.4x at the end of Q4, down 2.5x turns from two years ago as debt was reduced by $1.3B and adjusted EBITDA grew by $500M (+44%) over the same period. SWK ended the quarter with $0.3B in cash and total available liquidity of $3.2B against $4.7B in long-term debt. Debt reduction and maintaining a solid investment grade rating remains a top priority, with CAM proceeds expected to push net leverage to or below 2x, opening the door for opportunistic share repurchases.

7) Management delivered another $120M of incremental pre-tax run rate cost savings in Q4, marking the completion of the global cost reduction program initiated in mid-2022 with cumulative savings of $2.1B (vs. the original $2.0B target). Going forward, management remains committed to pursuing annual productivity gains of ~3% of net spend (~$300M gross annual savings), expected to drive net savings of ~$100M annually and allow for incremental margin expansion alongside reinvestment in the brands.

8) Free cash flow jumped to $883M in Q4, up from $565M a year ago, bringing FY25 FCF to $688M and ahead of prior guidance of ~$600M. For FY26, management expects $700M-$900M of free cash flow, with the midpoint implying +16% growth and a 6.4% FCF yield.

9) Tariff mitigation strategies have been highly successful and are running ahead of schedule, with SWK experiencing only one quarter of adjusted gross margin pressure before resuming expansion in FY25. SWK was originally importing ~20% of North American volume from China, a figure expected to fall below 5% by end of FY26 and currently pacing ahead of schedule. Additionally, the original 18-24 month target of reaching industry-average USMCA-qualified import mix is now tracking well ahead of plan, with SWK eyeing a position slightly above industry average.

10) SWK expects to deliver both reported and organic sales growth of low single digits in FY26, which would mark the first full year of positive organic growth since FY21. Adjusted EPS is expected in the range of $4.90-$5.70, with the midpoint implying +13% Y/Y earnings growth. Management also reiterated its FY28 medium-term targets presented at its 2024 Capital Markets Day, eyeing mid-single-digit organic growth in a low-single-digit market, adjusted gross margins of 35-37%, FCF conversion of ~100% (+/- 10 pts), and CFROI in the low-to-mid teens.

Earnings Call Highlights

Generac Update

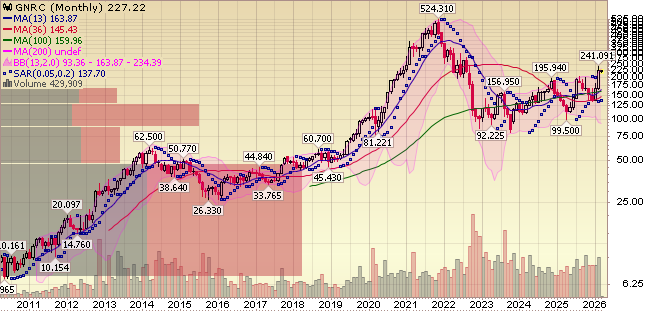

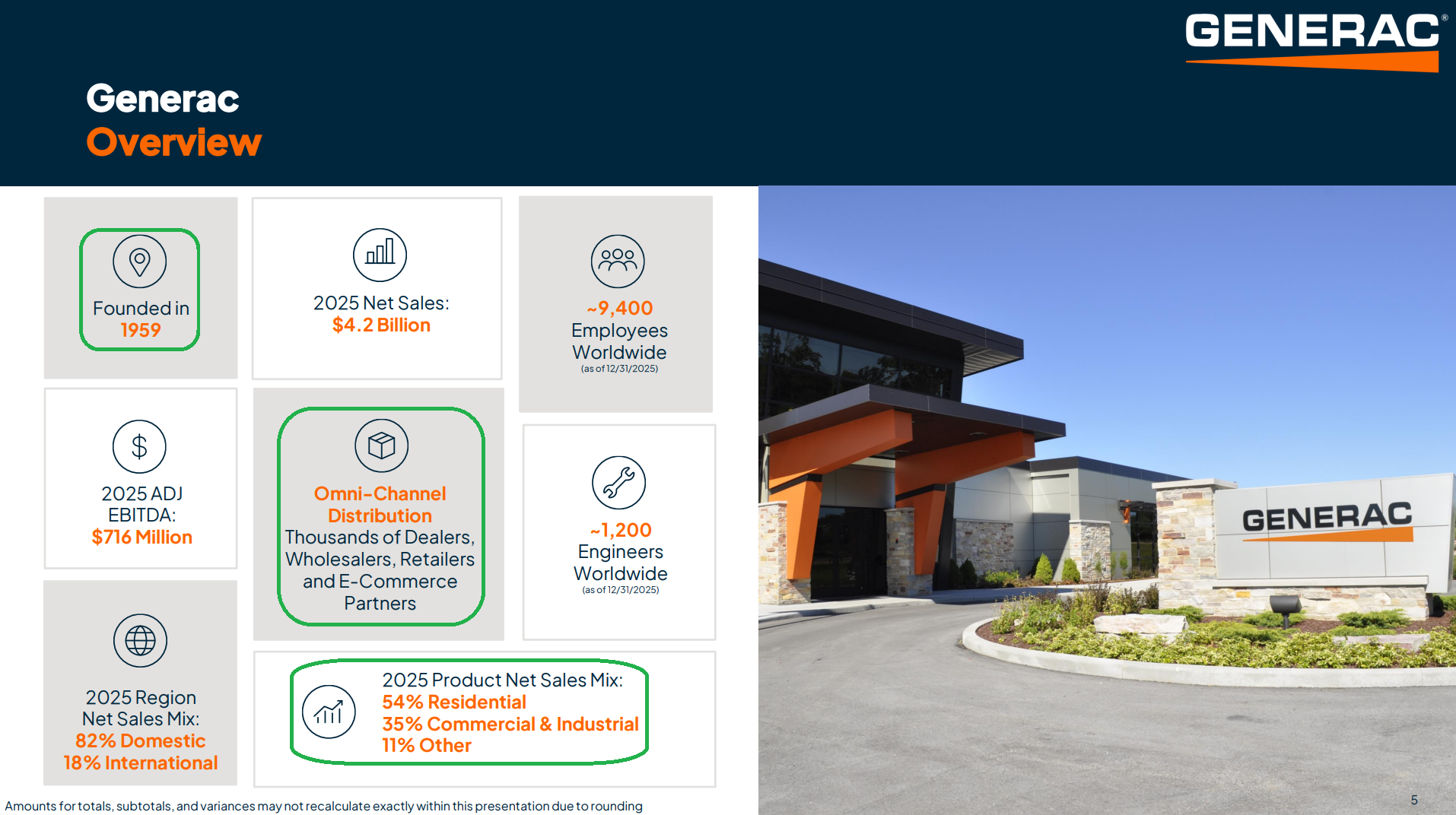

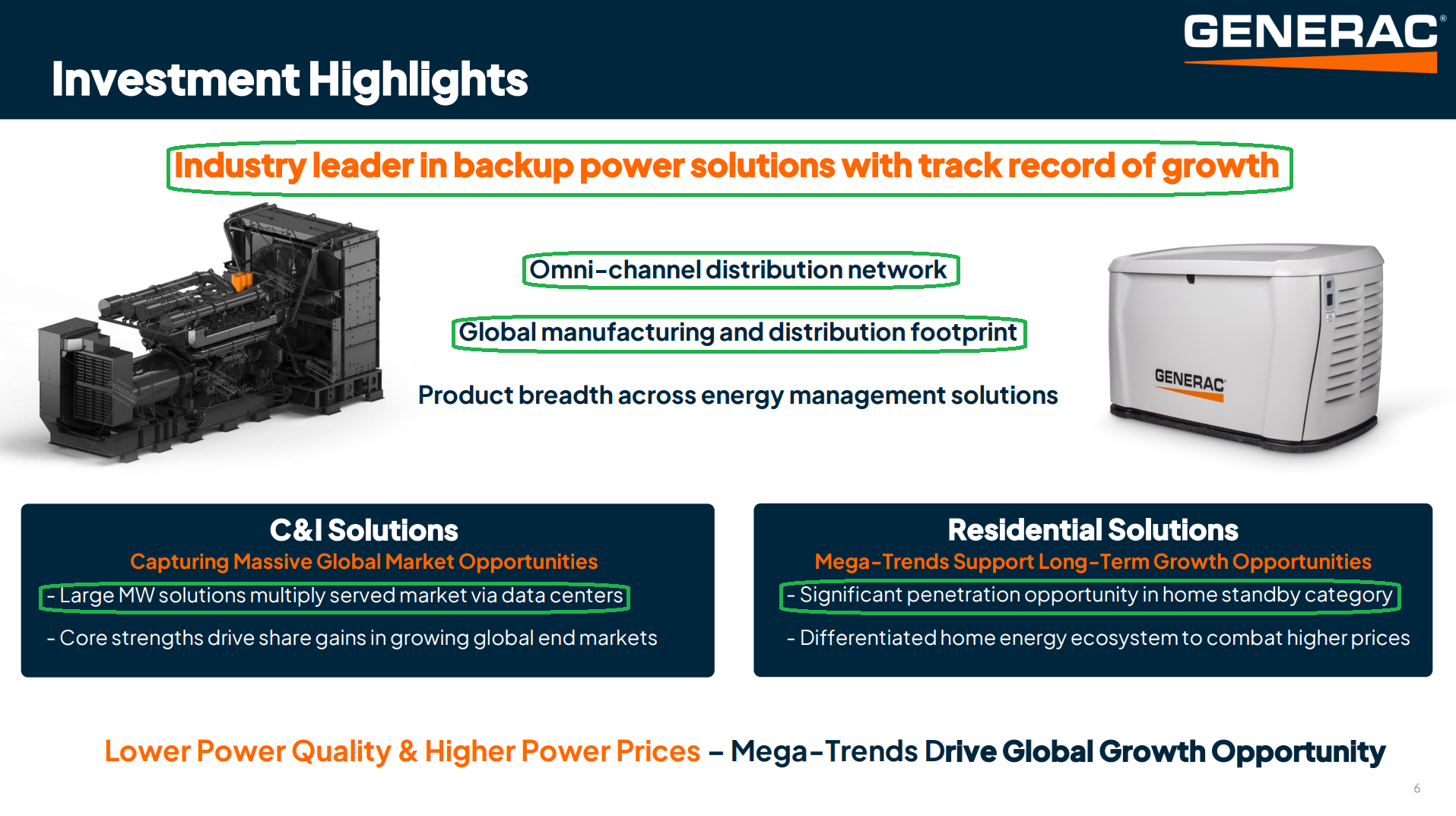

Generac, the Kleenex of generators that was once a sleepy name, has quietly turned into a massive winner for us as the market begins to recognize that the company has become a key pick-and-shovel beneficiary of the AI data center buildout.

Even better, it offers that exposure at a reasonable valuation, a textbook example of what we mean when we say buy AI BENEFICIARIES, not the AI COST CENTERS.

Naturally, there is plenty of excitement around this name right now as the company rides the newfound wave of what management has made clear is the biggest needle-moving opportunity in company history.

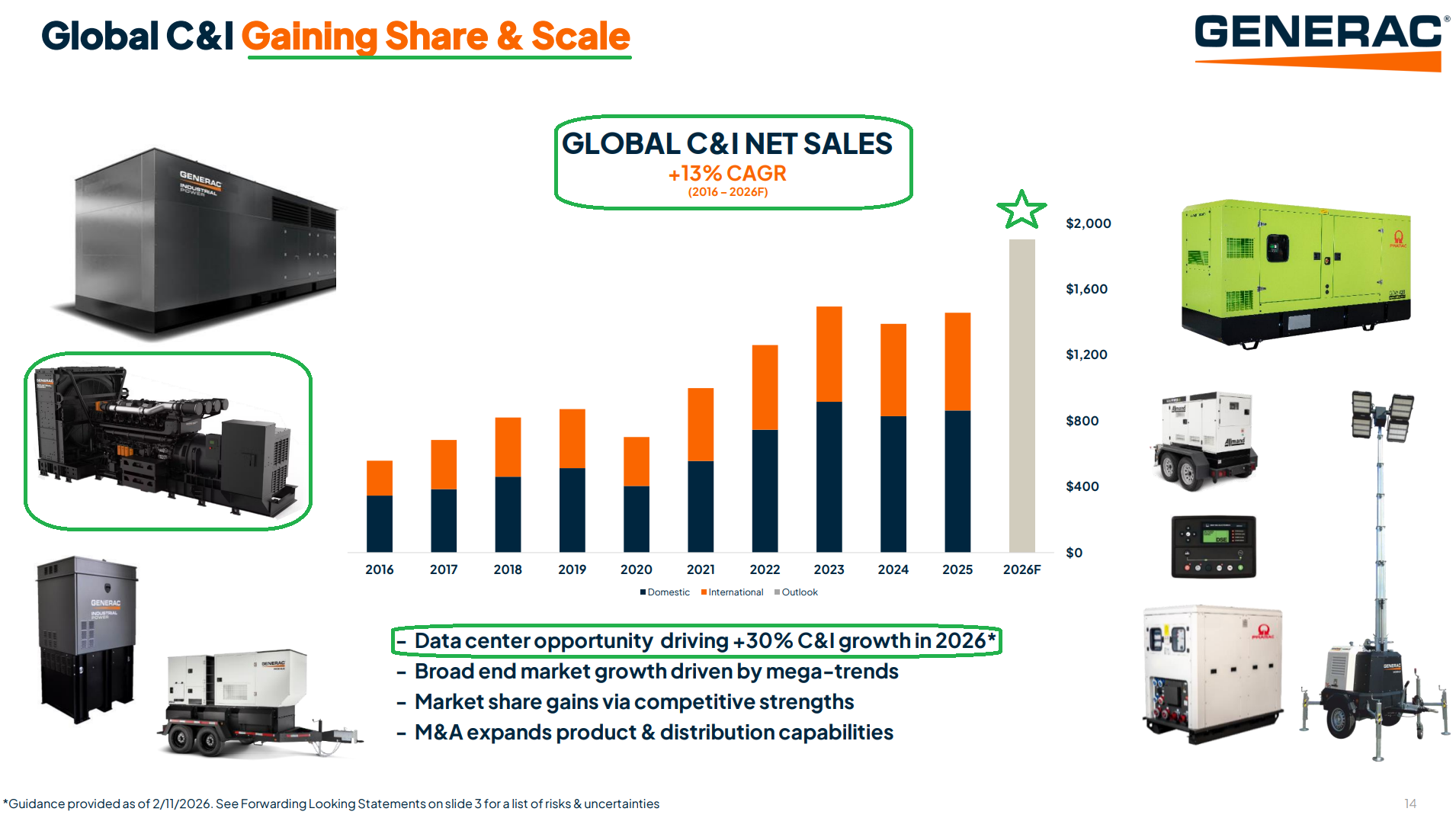

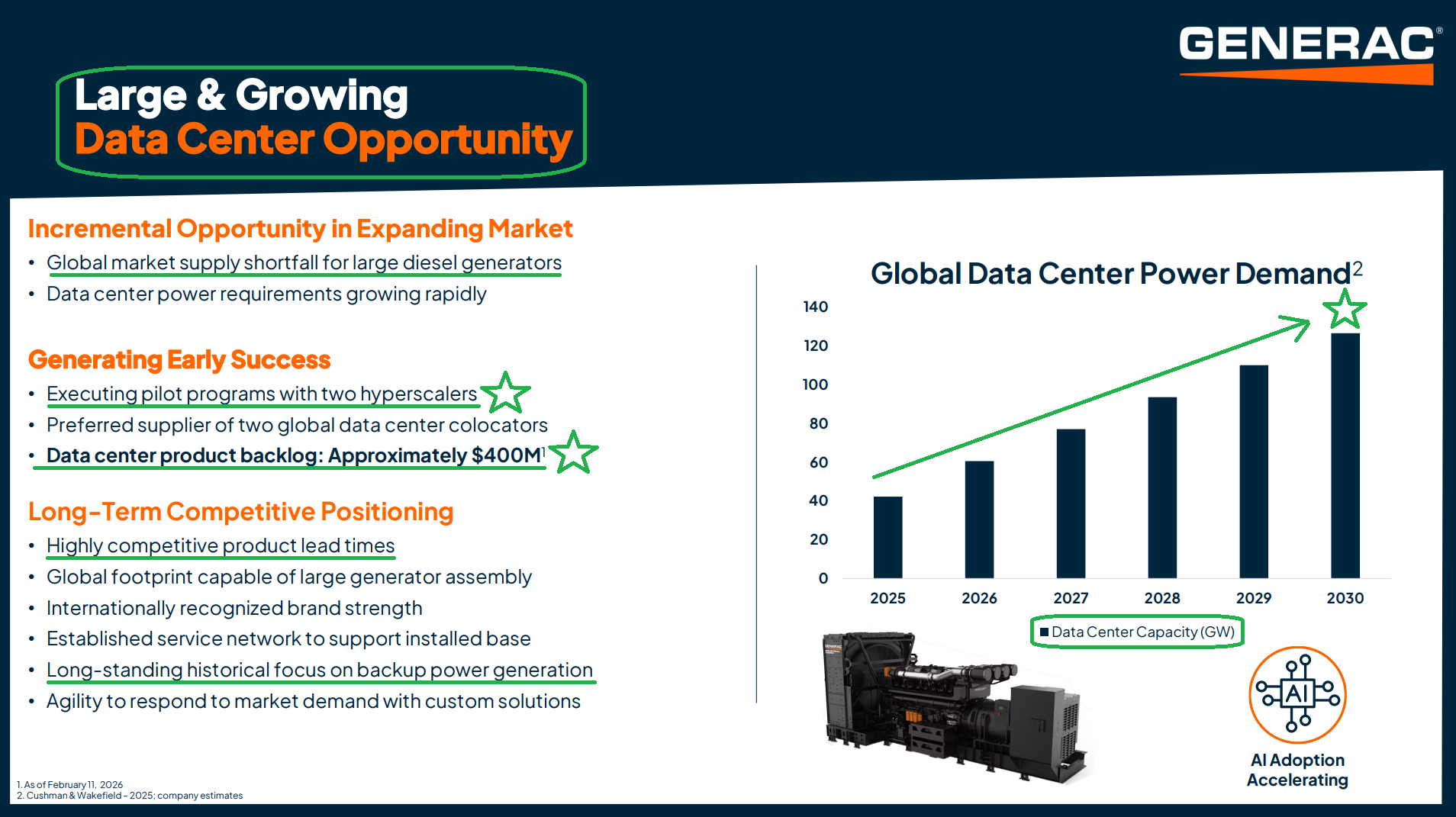

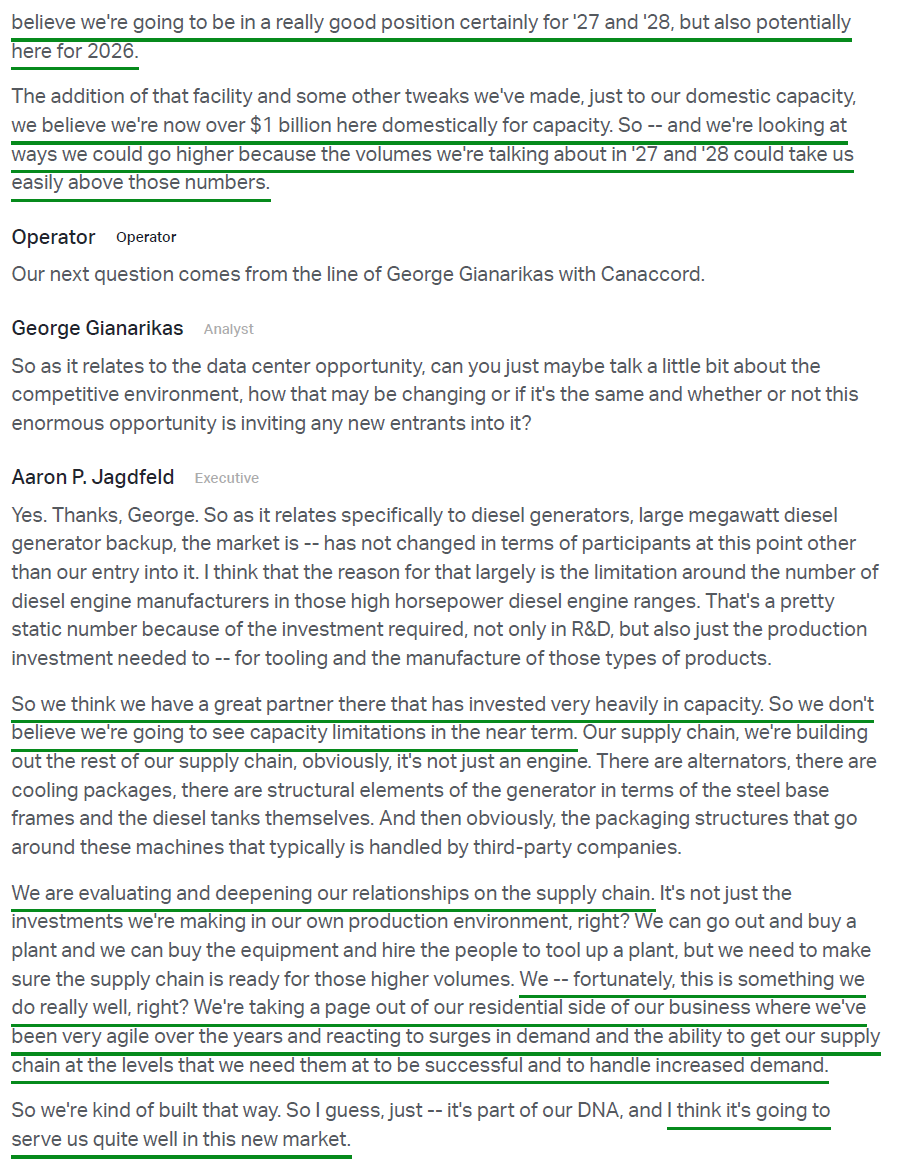

This is all centered on the company’s new large megawatt generators, where backlog has already swelled to $400M+ for these school-bus-sized units priced at $1.5M–$2M each. GNRC is stepping into a market facing a major supply crunch, with the company uniquely positioned to offer lead times shorter than the competition through 2026 and likely well into 2027. While initial success has been driven by co-locators and developers, which make up nearly the entirety of the current backlog, the real upside potential lies in landing a hyperscaler. Generac is currently in the pilot phase with two separate hyperscalers, which management expects to wrap up by the end of Q1 and translate into purchase orders flowing into the backlog beginning in Q2.

Now, here are the most important lines from the entire earnings call:

“To answer the last part of your question about our contemplation of doubling the C&I business over the next 3 to 5 years, if we had to be very honest, that was really landing one hyperscaler… if we landed one hyperscaler, that would get us to a point of doubling. Is there an opportunity to go higher than that? Of course.”

In plain English: GNRC is in active talks with two hyperscalers and is highly confident with both. Landing just one leads to a DOUBLING of the $1.5B C&I business.

While the market gets excited about the data center opportunity, it’s worth stepping back and remembering how this investment started. When we originally underwrote GNRC, it had nothing to do with data centers. The thesis was simple: an industry leader temporarily beaten down by a de-stock/re-stock cycle that the market treated as permanent impairment. That thesis remains fully intact today and has only gotten more attractive.

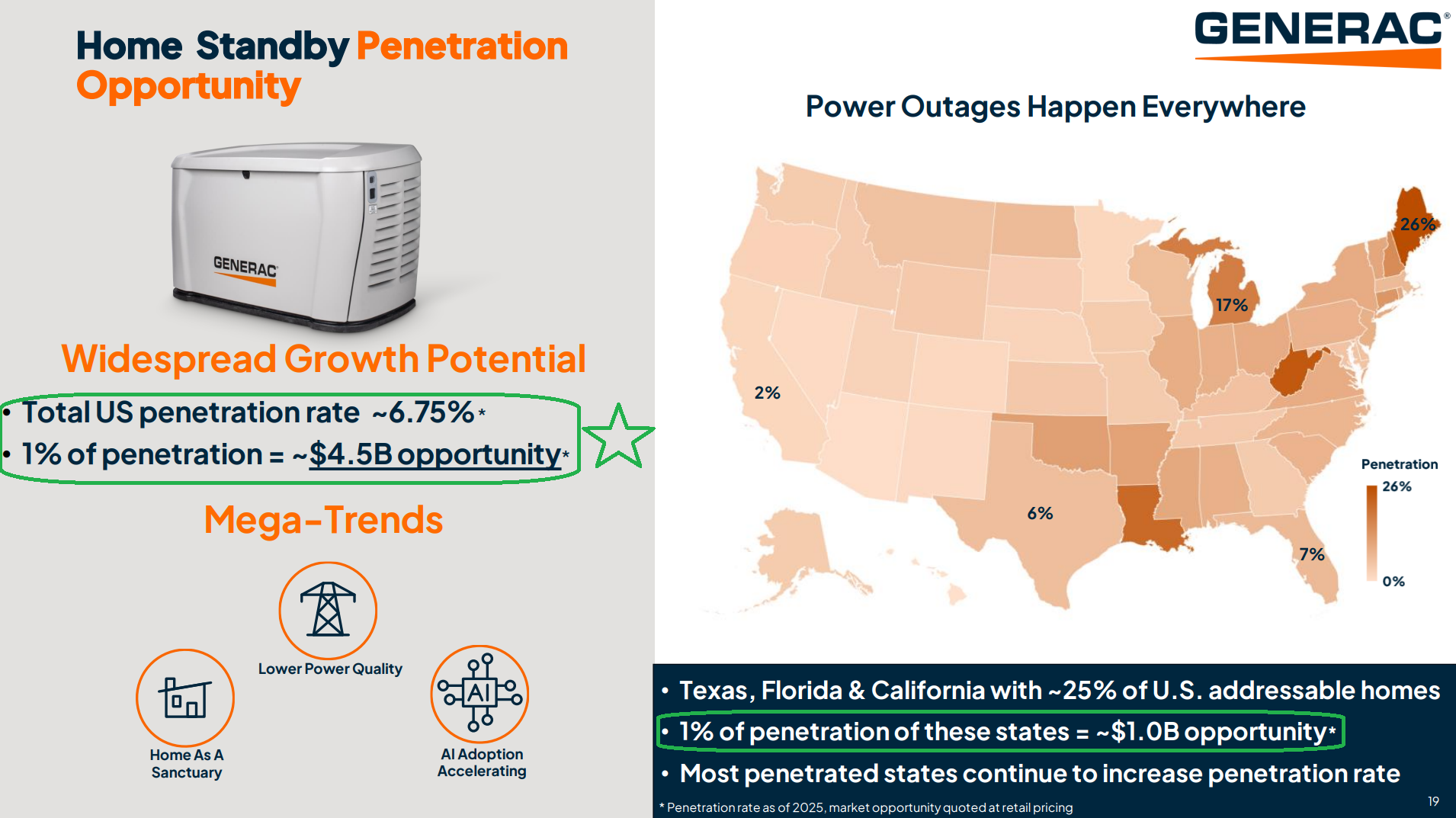

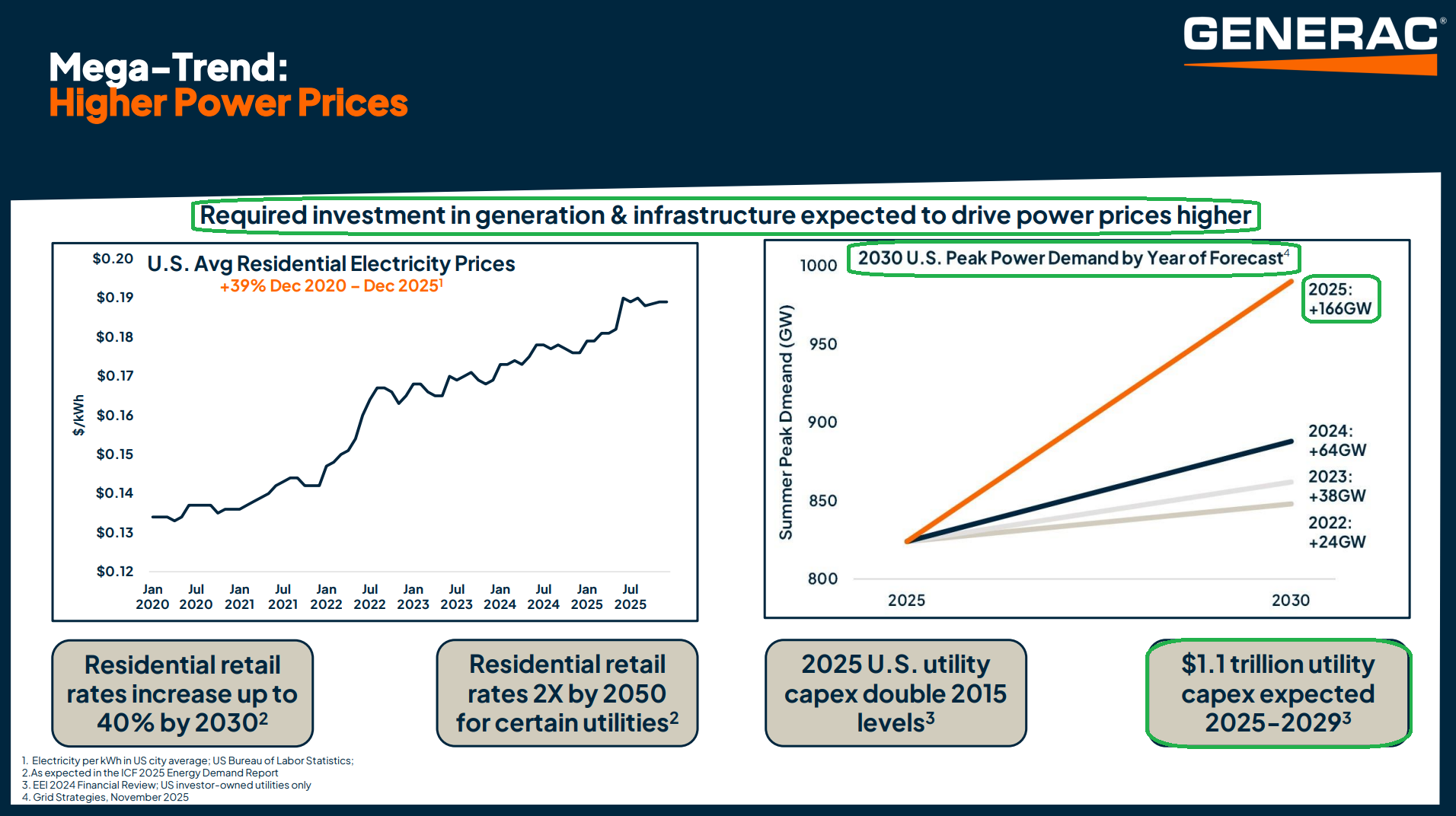

GNRC continues to dominate the high-margin home standby market with 75%+ share and a long runway still ahead, with household penetration still at just 6.75% and every 1% uptick representing a $4.5B opportunity.

The AI data center tailwind was never part of the original investment thesis. We couldn’t have predicted it, but we are more than happy to take the free flier. And that is exactly what it is for us: a free flier.

In many ways, the setup reminds us of our INTC investment. When we originally underwrote INTC, the thesis was based on the legacy CPU and PC business alone being worth $45–$50 per share, offering a double from our cost basis with the domestic foundry bet being whipped cream and cherries on top. The situation with Generac rhymes. The legacy residential and traditional C&I business was undervalued following a once-in-a-generation demand pull-forward and subsequent destocking cycle, and now we find ourselves with the added bonus of a free flier on the data center end market. But unlike the domestic foundry effort at INTC, this free flier comes with even fewer question marks and the writing arguably already on the wall.

It’s only a matter of time before headlines start coming out of hyperscalers signing deals with both GNRC and INTC.

At the end of the day, this investment is a textbook example of our core investment philosophy from the master himself:

When you identify situations like that and stay the course, good things tend to happen.

When you identify situations like that and stay the course, good things tend to happen.

The next major catalyst for GNRC is the March 25th Investor Day, where management is expected to go into detail on the scale of the opportunity ahead and perhaps provide the stage for a big announcement…

Q4 Earnings Breakdown

10 Key Points

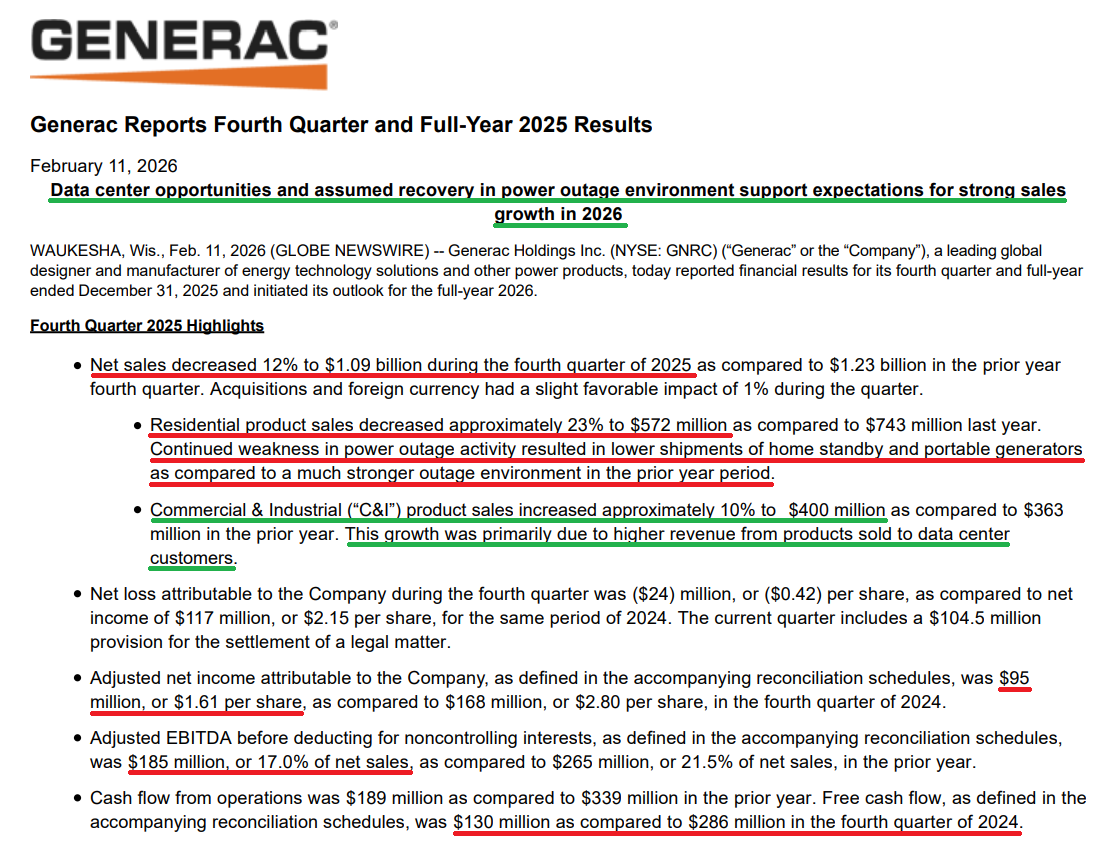

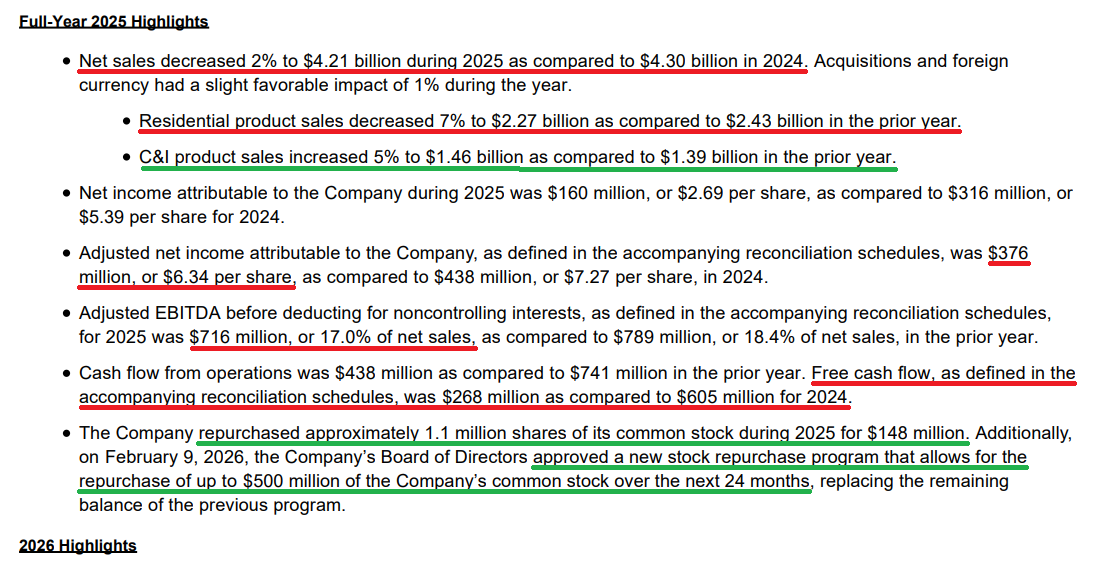

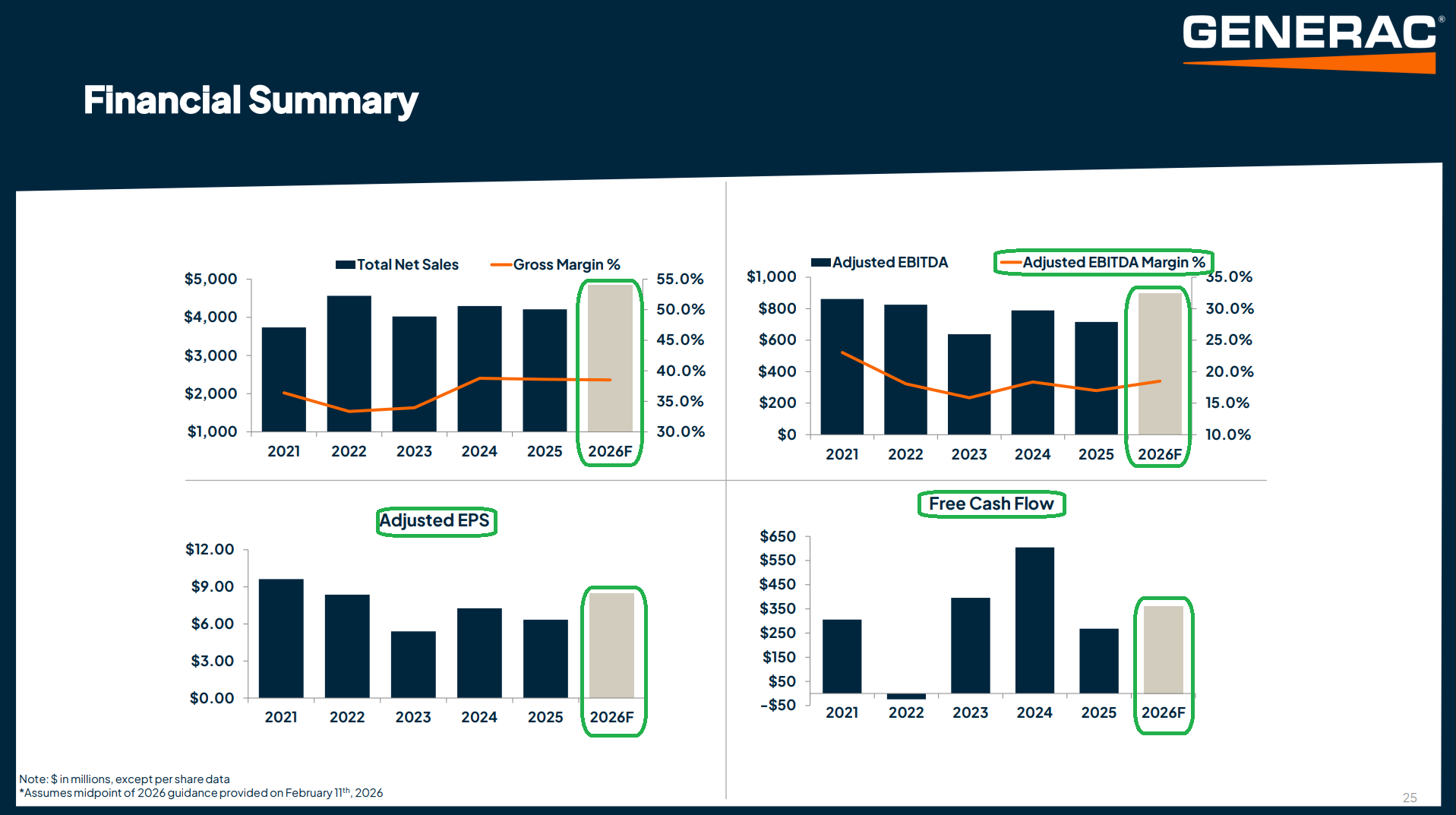

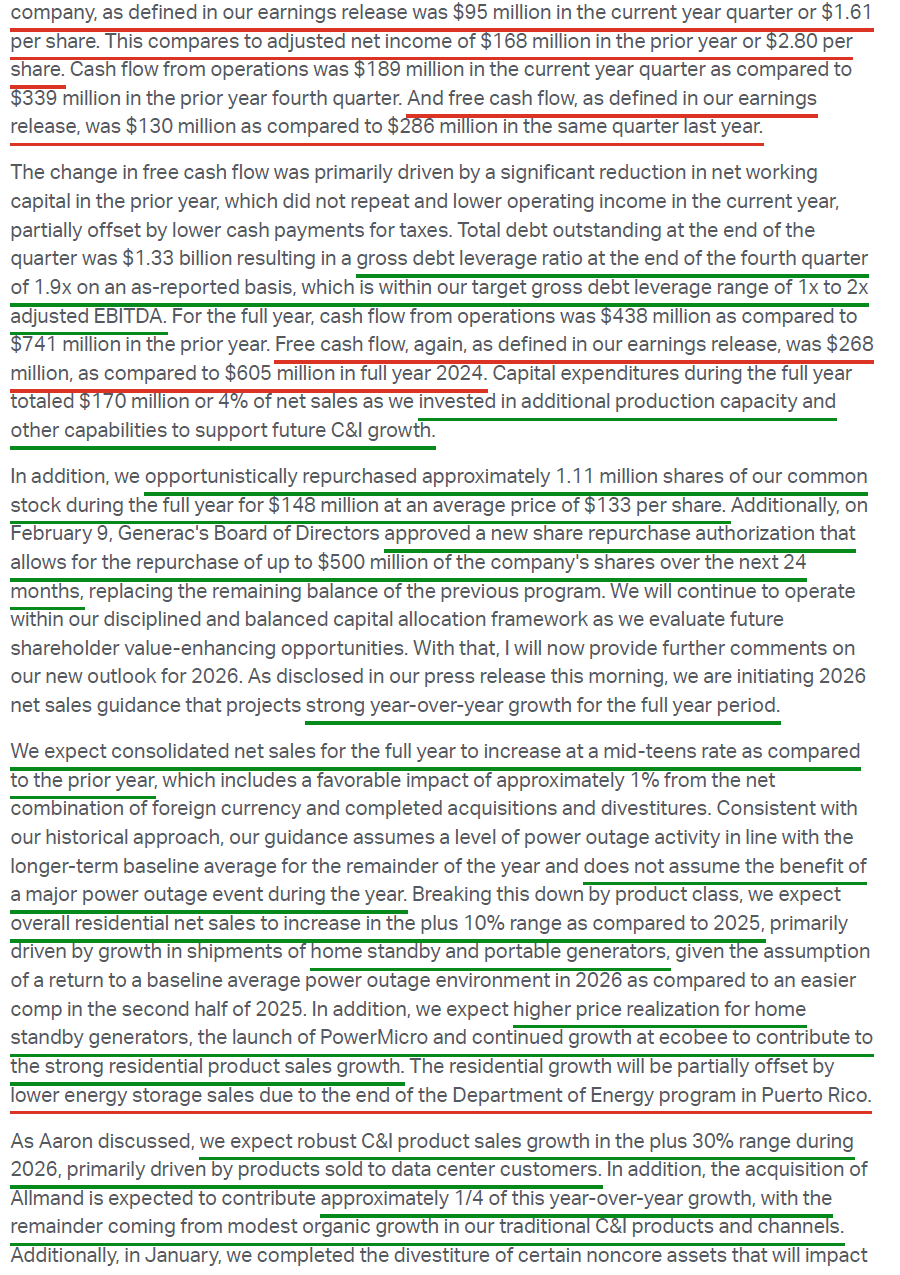

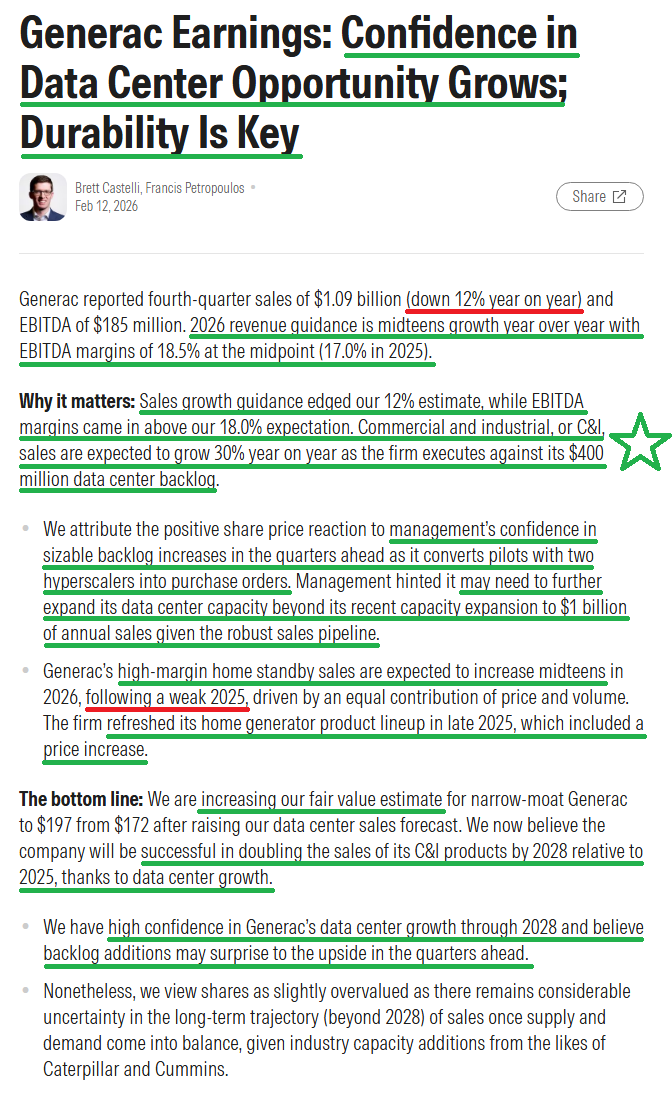

1) Generac posted Q4 revenue of $1.09B (-11.6% Y/Y), missing consensus of $1.16B and bringing FY25 revenue to $4.21B (-2% Y/Y). Adjusted EPS of $1.61 in Q4 missed consensus of $1.77, bringing FY25 adjusted EPS to $6.34 (-12.8% Y/Y).

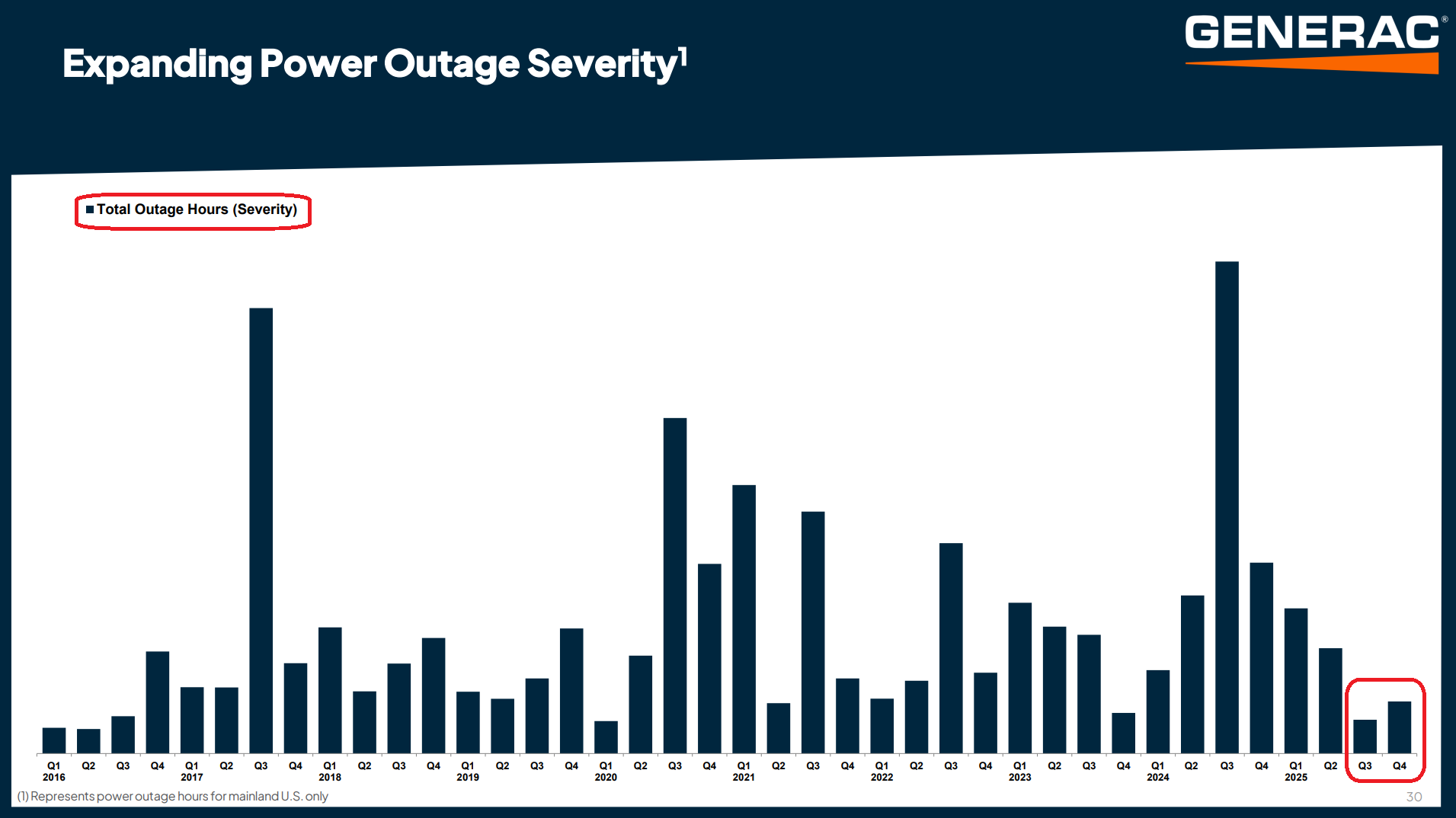

2) The residential segment (54% of total sales) saw Q4 revenue decline 23% Y/Y to $572M, bringing FY25 revenue to $2.27B (-7% Y/Y). Weakness was driven by a 25% decline in home standby shipments and soft portable generator shipments, as the back half of FY25 saw the lowest power outage hours in over a decade alongside tough comps from multiple major storms that made landfall in the prior year period. Management expects the segment to rebound in FY26, eyeing 10% overall growth with home standby increasing at a mid-teens rate as outage activity returns to baseline levels. The year is already off to a strong start, with Winter Storm Fern driving strong portable volumes and doubling home standby consultations in the month.

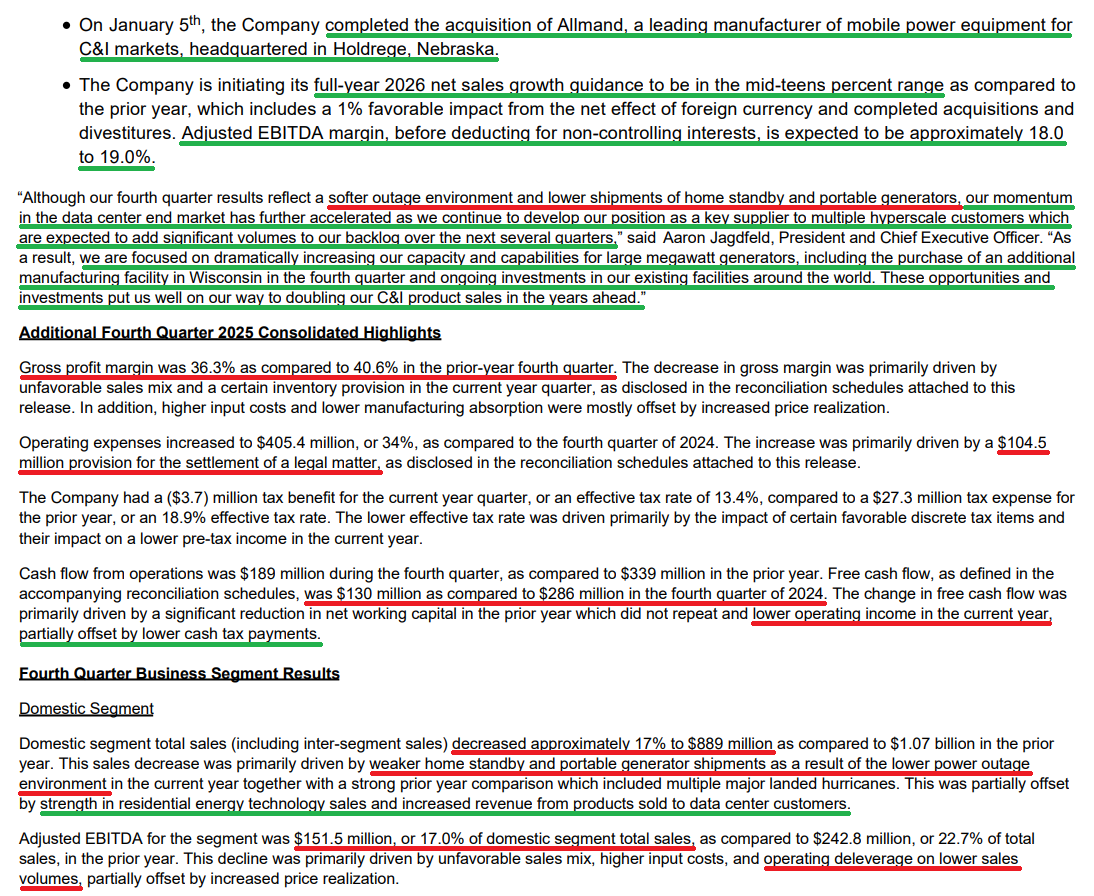

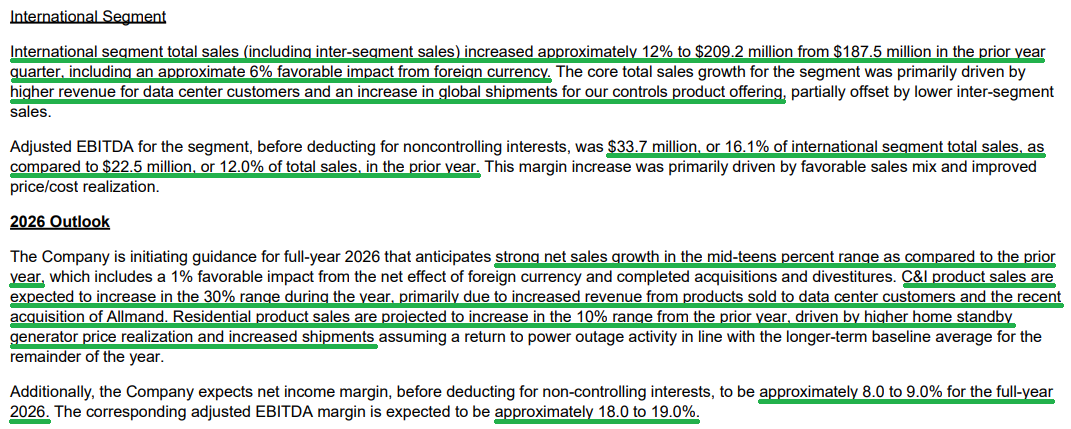

3) Generac’s large megawatt generators targeting the data center end market continue to gain momentum, with the backlog growing to $400M, the vast majority of which is expected to ship in FY26, and domestic capacity on track to surpass $1B in annual sales by year end (vs. ~$500M prior). The current backlog is built almost entirely from orders placed by co-locators and developers and does not yet include any material hyperscaler orders, though GNRC is now in the pilot stage and deep negotiations with two of them. Management is confident these pilot programs will be successfully completed by end of Q1, with purchase orders beginning to flow into the backlog in Q2, and landing just one hyperscaler would create enough volume to double the C&I business over the next three years and easily push GNRC above its current $1B capacity threshold. Management sees the data center end market as a $15B annual opportunity and believes GNRC can realistically become a 10-15% share player. On margins, large megawatt generators are currently running at mid-teens EBITDA and are expected to scale to high-teens by 2027/2028 in line with corporate averages, with further upside as GNRC pursues vertical integration of its supply chain.

4) The C&I segment (35% of total sales) posted Q4 revenue of $400M (+10% Y/Y), bringing FY25 sales to $1.46B (+5% Y/Y), driven by strong data center demand and a recovery in traditional end markets. Shipments to national telecom customers were a bright spot in FY25, increasing 27% Y/Y with another year of solid growth expected in FY26. Shipments to national and independent rental customers also grew in Q4, which management views as the start of a cyclical recovery with further growth expected in FY26. Looking ahead, management expects C&I sales to grow ~30% in FY26, primarily driven by the data center market alongside the recently closed Allmand acquisition, a leading manufacturer of mobile power equipment expected to contribute roughly one quarter of full year growth.

5) Ecobee delivered another strong quarter to close out the year, posting mid-teens revenue growth for FY25 and reaching a new all-time record, alongside significant gross margin expansion and positive EBITDA contribution for the first time. Management expects further sales growth and profitability improvement in FY26, though the solar and storage market is expected to contract 20-25% due to the pullback from the DOE program. As a result, the segment is expected to deliver revenue of $300-$400M in FY26 compared to ~$375M in FY25, with management still confident in reaching breakeven profitability by 2027.

6) Gross margins came in at 36.3% in Q4 (vs. 40.6% in the prior year), weighed down by weakness in the high-margin home standby segment. For the full year, gross margins were 38.3% (vs. 38.8% in FY24). Adjusted EBITDA margins came in at 17.0% in Q4 (vs. 21.5% in the prior year), with FY25 adjusted EBITDA margins also finishing at 17.0% (vs. 18.4% in FY24).

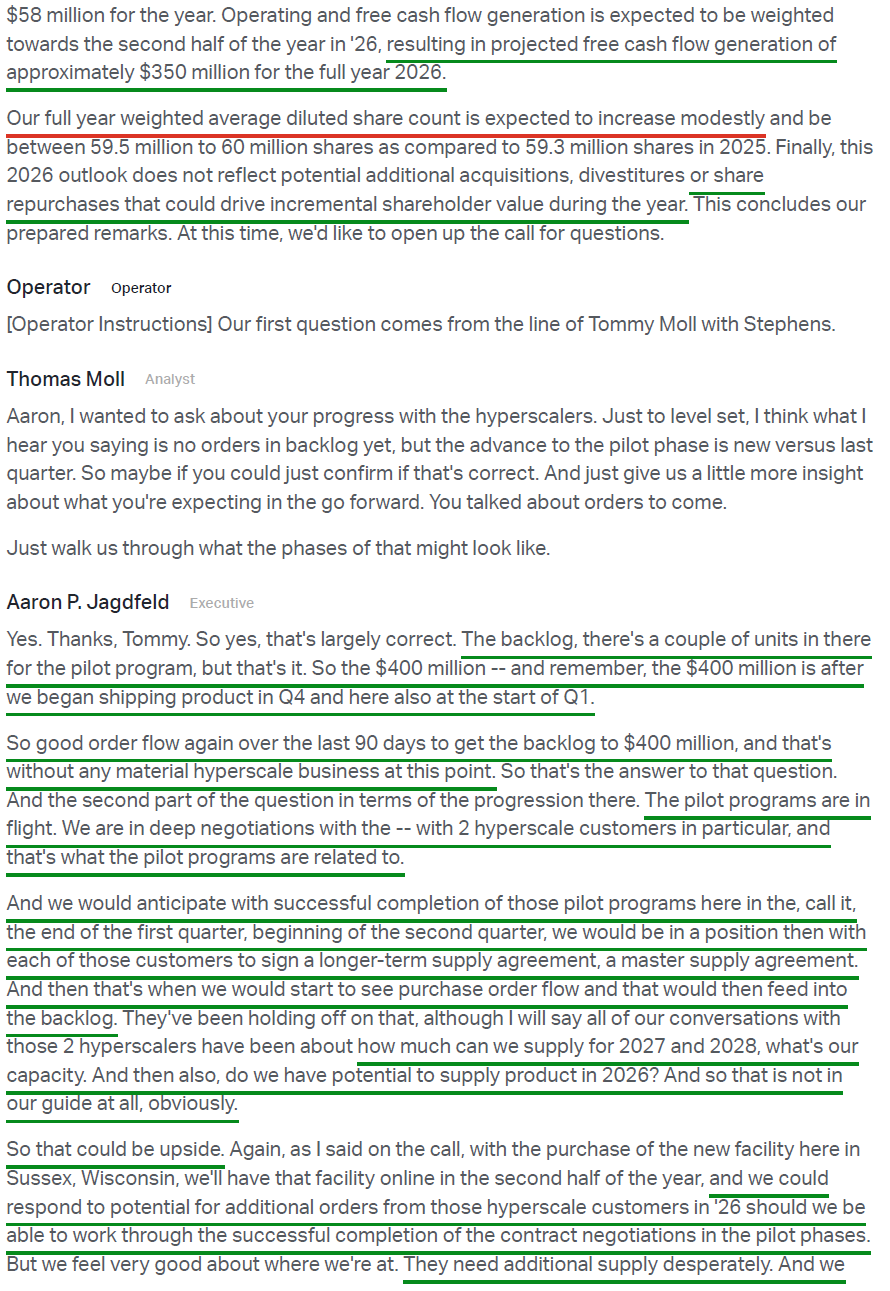

7) Free cash flow came in at $130M in Q4 (vs. $286M in the prior year), bringing FY25 FCF to $268M (vs. $605M in FY24). The step back was driven by a significant net working capital release in the prior year that did not repeat, as well as ramped up capex from the data center capacity buildout, which increased to $170M (4% of sales) vs. $137M (3.2% of sales) in FY24. For FY26, management expects to deliver ~$350M in FCF, implying ~31% Y/Y growth.

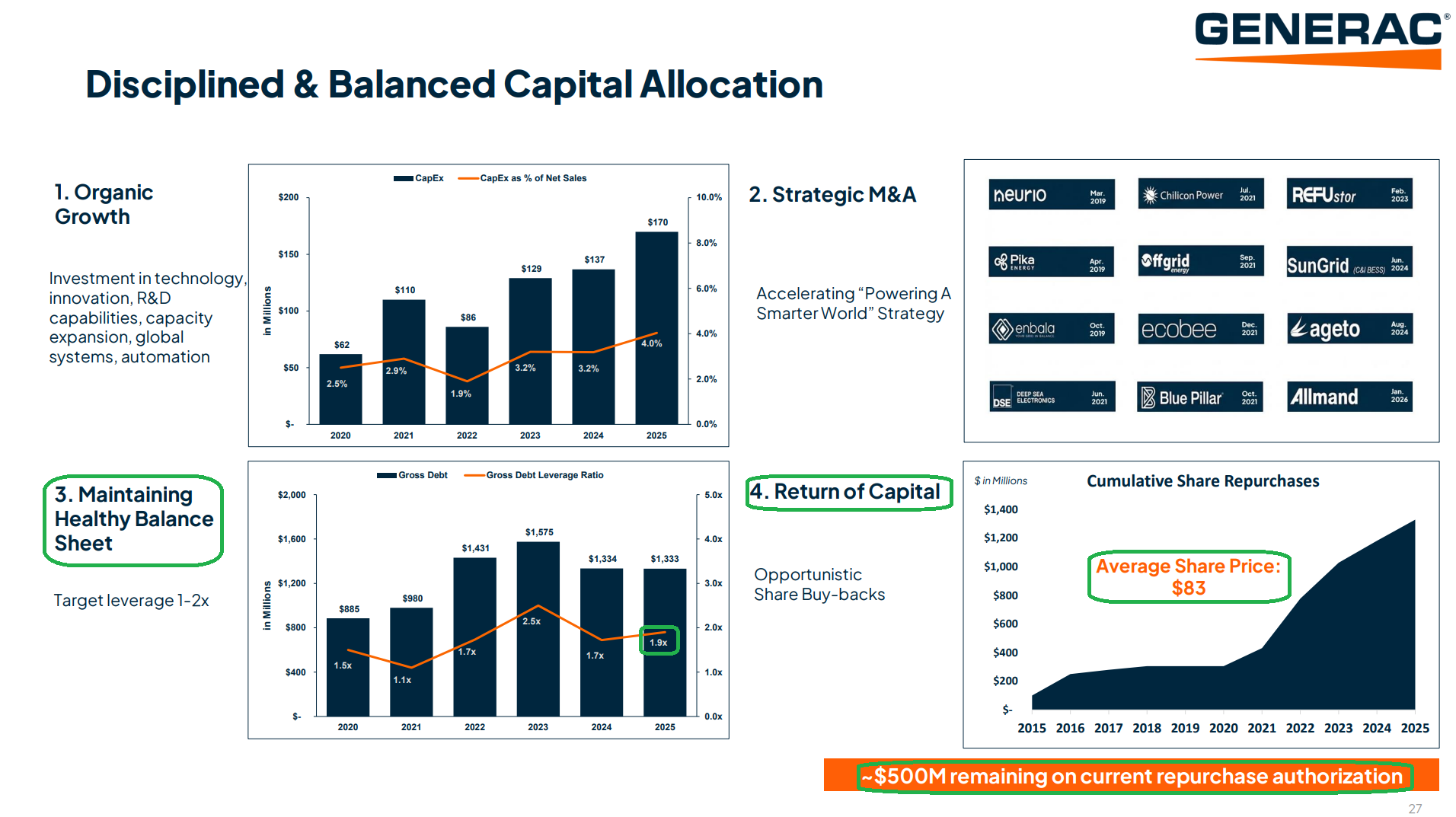

8) Management repurchased 1.1M shares for $148M in FY25 at an average price of $133 per share. The board also approved a new $500M stock repurchase program over the next two years, representing ~4% of total market cap.

9) Generac maintains industry-leading distribution, with the residential dealer network growing modestly in Q4 to over 9,400 dealers, up over 300 from the prior year. Management was also able to assess its new lead distribution system in an elevated demand environment for the first time during Winter Storm Fern, delivering promising early returns and a meaningful improvement in close rates.

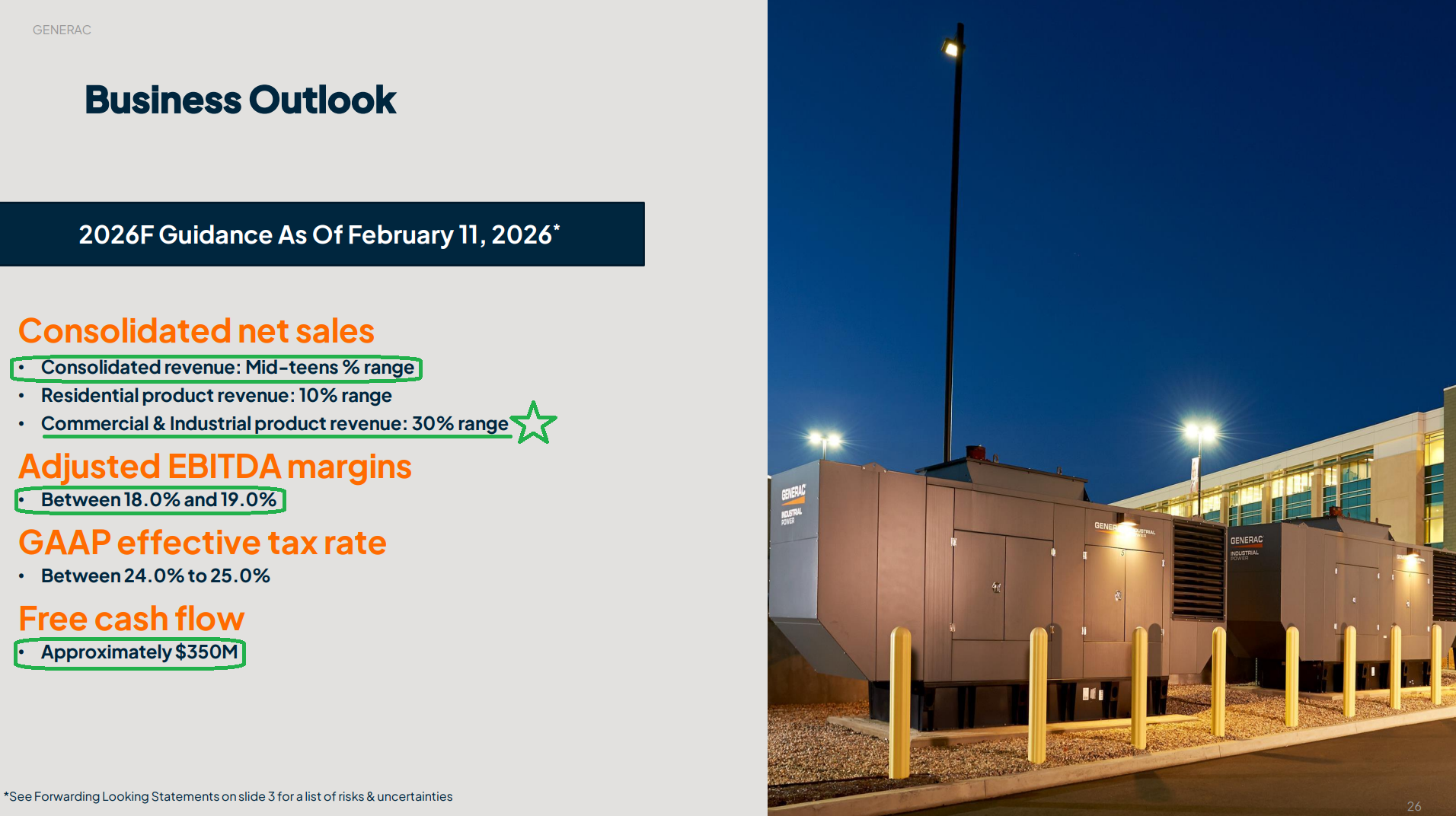

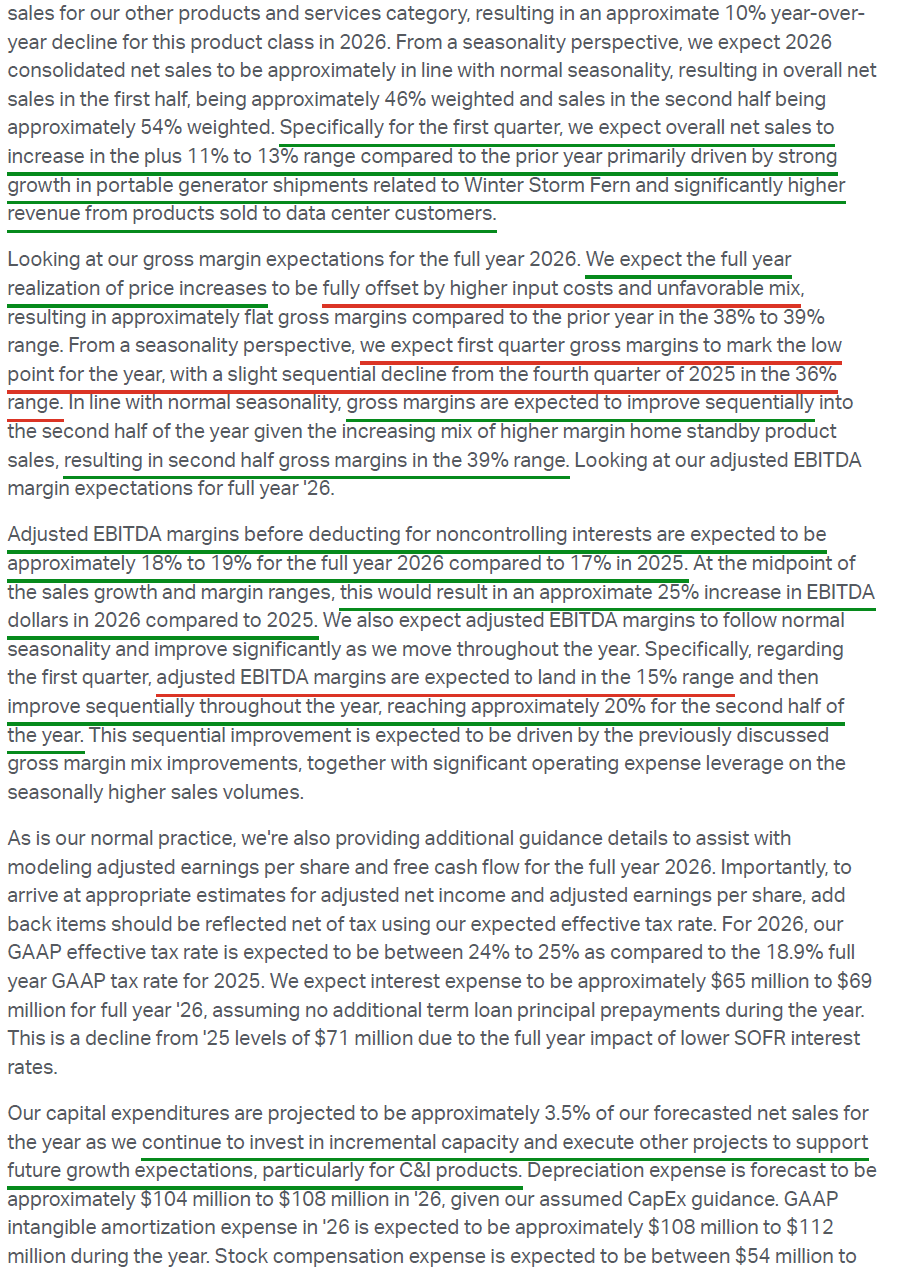

10) Looking ahead to FY26, management expects net sales growth in the mid-teens, with C&I up ~30% and residential product sales up ~10%. Gross margins are expected to remain largely flat Y/Y at 38-39%, with adjusted EBITDA margins expanding to 18-19%, implying ~25% Y/Y growth in EBITDA dollars. Guidance implies FY26 net sales of ~$4.84B and adjusted EBITDA of ~$895M, both coming in ahead of consensus of $4.73B and $863M, respectively.

Earnings Call Highlights

Morningstar Analyst Note

General Market

The CNN “Fear and Greed Index” ticked down to 38 this week from 46 last week. You can learn how this indicator is calculated and how it works here: (Video Explanation)

The NAAIM (National Association of Active Investment Managers Index) (Video Explanation) fell to 74.93% equity exposure this week from last week’s 82.87%.

Our podcast|videocast will be out sometime today. We have a lot of great data to cover this week. Each week, we have a segment called “Ask Me Anything (AMA)” where we answer questions sent in by our audience. If you have a question for this week’s episode, please send it in at the contact form here.

Larger accounts $5-10M+ can access bespoke service anytime here.

Not a solicitation.